Fully aware that this is a old post. The reason one should invest if they wish to in FD and not call it ridiculous is because whats happening in the world banking sectors.

Few banks collapsed in usa, the federal reserve came to the rescue of depositors. Similarly with credit suisse, i read ubs is taking over the bank for 1 billion.

Central bank has assured the depositors of their money. I am sure the equity shareholders have lost everything.

When events like this happen, fd ensures at least your capital is safe most of the time unlike investing in the markets

Only a person who goes thru the pain of losing capital will understand this and not call investing in fd is ridiculous.

Only 5 lakh is insured in the bank, better keep in mutiple banks or move to gsec or money market funds or some bit in gold( in case hyperinflation hit). Why would i risk my sleep over

Banks which are just gaming the system they just have there own interest not the depositors. P2P lending and RBI ease of buying money market makes bank less relevant to retailers in this disruptive world

Yes. It is, but for the general public, FD has been the comman women/man go to investment vehicle. Can you buy Gsec without demat account. I thought you can buy gsec only through a broker

I believe you are a trader in the market, when you can take such high risk in the market, why do you think , bank deposits will give you sleep less nights. Yes bank was a classic case. No depositors lost money. Irrespective of the insured amount, due to systemic issues, RBI will not allow bigger banks to fail. Even in USA, all of them except for the crypto bank (not too sure) was bailed out and depositors got the money.

All I am saying is when a person can take large risk where the capital can be wiped out in one single trade, how come, they do not like bank deposits which is one of the relatively safe investment.

Buying Mutual funds is not very difficult. Once income becomes taxable, FD becomes very inefficient vs debt Mutual funds. This is the basic idea of the thread, don’t understand whats hard to understand.

That’s a very bad way to think about trading. Anyone who trades like this wont be trading for long. Trading can give much - much - better returns vs risk than even Nifty, once you have an edge.

And yes i would rather invest in something like overnight funds ( has gilt as collateral) or gilt itself for my capital vs FD/Bank where only max 5L is insured.

No idea if there is no precedent, i would think at least cooperative banks must have failed taking deposits with them but no matter - things happen that never happened before, Crude oil futures went negative even. Gilts are safer and there is no advantage from FD so why should we use it ?

Anyway risk would be low and if not taxable, FD from good bank probably is alright too. Just does not seem useful to me.

The cost of losing out on the returns is much more than cost of a demat account.

These days we know how easy it is to get a demat account.

Even then if you don’t want a demat account, you can go for gilt funds. But then you will have to bear expense ratio of the fund. Even then it will easily out perform FD.

I know you are a strong believer and endorser of FD and my intention is not to chance your opinion on this.

Agree. So does that make it an efficient asset class? From little that I know, you are a financial literate. I believe your income is above the basic tax limit. Do your own calculations with both risk and return and you will know how much of difference it will actually make.

In my opinion, FD are only for the ones whose income is below basic tax limit and do not understand anything about finance.

Interesting question. Depends on how you define safety and what you are trying to save.

While Gsec has no default risk it carries tremendous interest rate risk, especially for long dated securities. Especially in time like these when interest rate are moving up, Gsec can easily give a capital loss.

For people who have spent time in market and understand interest risk movement, this is very easy to comprehend.

But for newbie investors or those who does not understand debt market, this can be challenging situation.

@Jason_Castelino there is a risk in Gsec - liquidity risk. You cannot always exit when you want to, unless its a daily traded item like 754GS2036

FD can be broken very easily at a low impact cost. Also if the re-investment of interest option is selected for a 10 year period then the taxation is same as a Gsec

Only growth debt funds will have a tax advantage if you are not planning to withdraw

And most importantly - all these are pledgeable and can be used for margin. Gsec has 10% haircut, debt funds also 10% haircut

FD has 0% haircut.

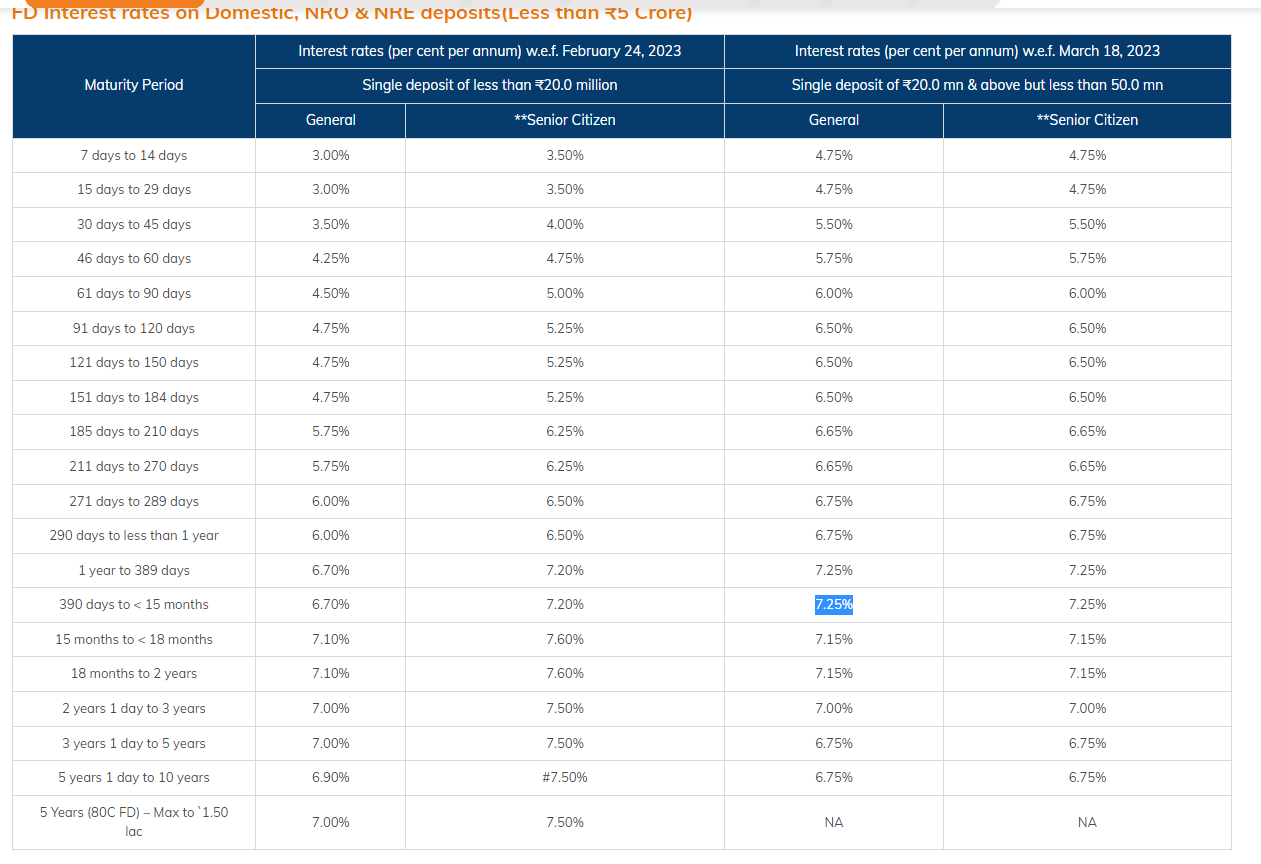

Currently none of the liquid gsec is giving more than 7.25% interest rate. So @neha1101 if i were to make a choice to deposit 20 lakhs right now - i would take the FD route.

I was referring to default risk when I was talking about safety.

I understand this very well. Even after considering this, it will easily outperform FD.

Further over a long term, I don’t think interest rate risk will be negative. We will only have interest rates coming down. In 20 years from now we may even have interest rate as low as 1 percent.

To the extend you want funds for emergency you can may be consider gilt funds. But if you holding to maturity then there is neither liquidity risk nor interest rate risk.

Not considering this because we are taking about common people.

Anyways. I respect all your views and you have pointed out relevant points. May be I was seeing it more from investment point of view.

So I stand corrected. For emergency fund, FD makes little sense. I would still prefer money market funds. Lol

Same. I actually have gilt funds only to the extent of 10 percent. But I mentioned about gilt only because I had to cover the default risk better than bank FD.

Who said it is difficult to understand what the topic is all about. I was putting across my point of view about FDs.

It is difficult for people who are common folks. I tried to explain this to my in-laws and they said they do not understand this. I am not saying who is right or wrong. All I am saying is FD is a very popular vehicle for Indian public.

To explain, when a person trades, I am assuming he is willing to take a greater risk. When he can take such risk, why does he think that FDs which are relatively low risk as a investment gives sleep less nights.

It is never advisable to put in money in co operative bank. Even though I will fight tooth and nail for FDs, I will never advise anyone to put money in cooperative bank.

I agree, but a person who puts money in FD wants his capital protected. Returns are a factor but not the core factor. Taxation might reduce the return, but tax can be managed, if a person is NRI - the FD returns are non taxed. You can distribute money among family members, if you are a resident and still avail the full interest benefits.

it depends on each individual and her/his risk taking ability. For my in laws, FD is the most efficient asset class as they do not pay any tax on the returns. Only when it comes to FD, people talk about returns, they go so conservative, that they are worried that the bank will fail when in fact depositors money is protected to a greater extent. At the same time, they are willing to put money in mutual funds and shares or trade, you need to expect capital loss as well.

I think you have very wrong understanding about trading business, and here your comparison is baseless. Business failure is different thing( Trading is business) and Bank is just a custodian of my money not a business. If custodian can’t keep it safe than why i would keep my money with it even every bank say only 5 lakh has insurance .

Ask PMC bank customers , any thing greater than 5 lakh they have lost .And there are ample banks who lost cutometers money

To the best of my knowledge the custodians over the years have always safeguarded the money and none have lost money. With regard to PMC bank, it is a cooperative bank and I have expressed my view that coop bank is not a place where I will keep money.

Again with regard to PMC bank, each of the depositors got 5 lacks each and for others the arrangment is as follows:-

As per the government approved scheme of merger of PMC Bank with Unity Small Finance Bank, all eligible depositors will get Rs 5 lakh under the DICGC scheme as the first round of payment. After that, there will be staggered payments over a period of 10 years. During this period, the depositors will get amounts ranging from Rs 50,000 to Rs 5.5 lakh from the first to fifth years, and the remaining at the end of 10 years

Everyone knows that the bank is a custodian and hence to safeguard the simple, depositors who put money in banks Central Bankers come in and ensure that the depositors money is safeguarded. The same happened with Yes bank where a clutch of competitor banks came in to safeguard the bank. The same is happeneing with Credit suisse which is taken over by UBS. I heard with regard to american banks all have gone to Warren Buffet… This is just news and I read this somewhere. To summarise, if it is a reasonably big bank, there is no issue of money being lost.

people have views, its tough to change their core beliefs

my parents had 90% of their savings in society, state govt. treasuries. i took me almost an year to convince them to shift to Gsec although they were getting (8.5%, gsec gives them 7.3%). When this happened the max FD returns were 5.2%

Bank runs can happen in India, i am a silent majority that thinks it will happen before 2024. Mostly because of the un secured loans given by banks during covid.

Also financing is a big business in our country, much above the agriculture and textile sector. Most of the financing done informally has interest rates so high that it will supersede the principal in 10 to 12 years.

I thought gilt funds were better. Gilt index funds have expense around 0.2%, but taxation is all in CG so post 3 years it should be better vs interest from gilts which is taxed at slabs. Plus reduced complexity. If income not taxed, then yeah direct gilt should be better.

yeah, perhaps that’s why its taxed unfavorably. Also its not very difficult to understand if someone takes an effort and atleast someone in family should. But anyway, we cant control that…

Assumption is incorrect. Traders can control their risk and get reward in proportion to risk taken. So taking more risk is a choice. While most may well be taking too much risk, but its not a given

I will never expose all of my capital to this kind of risk.

FDs are low risk perhaps but also unsecured beyond 5L. There is a reason why unsecured loans pay more interest vs secured ones. Add to that taxation impact and FD becomes really pointless beyond your immediate cash needs.

At the least, someone investing in FDs should diversify it across good banks.

cool, but things happen. Unsecured debt is unsecured. FD is only protected till 5L. Cannot have dangerous belief that it will always be bailed out. But yes, chance of anything happening to large banks is low but not impossible either.

This is my only issue with FDs. If taxes are managed then it’s fine. In fact that’s why I mentioned for somebody who’s income is above basic limit it’s not efficient. Then all the indexation benefit and all becomes irrelevant.

Yes correct. When I first spoke about gsec I was actually referring to gilt funds. Later I somehow got lost with my replies when somebody spoke about its liquidity.

Anyways. Thanks for correcting.

| FRONTLINE")