Once we start earning and make some lump sum money, one of the most common recommendations from our parents would be to invest that into Fixed Deposit. Even most of our parents used to keep their savings in FDs. But does it really makes sense now, if one invest in FD for long term investment? Let’s check it out.

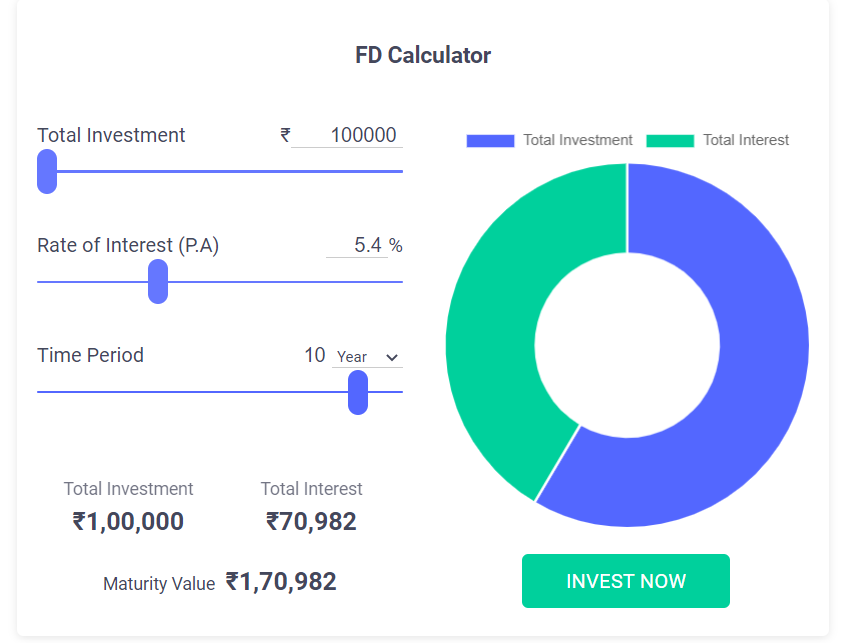

If you Invest 1 lac in FD for ten years with current interest rate of 5.4%, your 1 lac grows to 1.7 lacs in ten years. But if you fall under 30% tax slab, then the returns you get from Fixed Deposit is not tax-free, we need to pay tax for that as well. After tax, your FD interest rate will be just 3.92%, so after ten years your post tax returns would be only Rs. 1.47 lacs only.

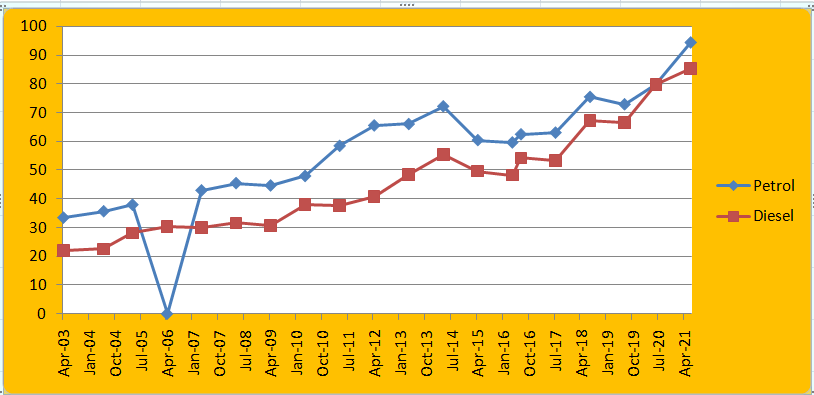

But consider the inflation, remember what was the petrol/diesel price before 10 to 15 years? Currently, we pay around Rs.100 per litre, but in the year 2003 it was just Rs. 33. The fuel price alone increased more than 203% in last 15 years.

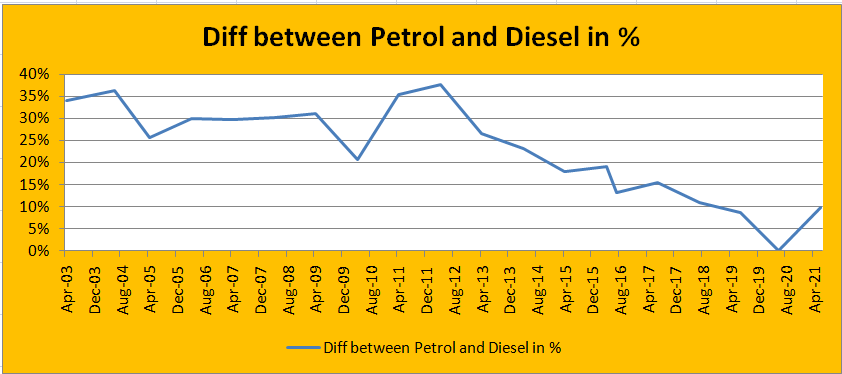

Even the difference between petrol and diesel is also very narrow now. Earlier the difference was around 30% to 35%, but in last 10 years it kept on going down. Now the difference is less than 10%.

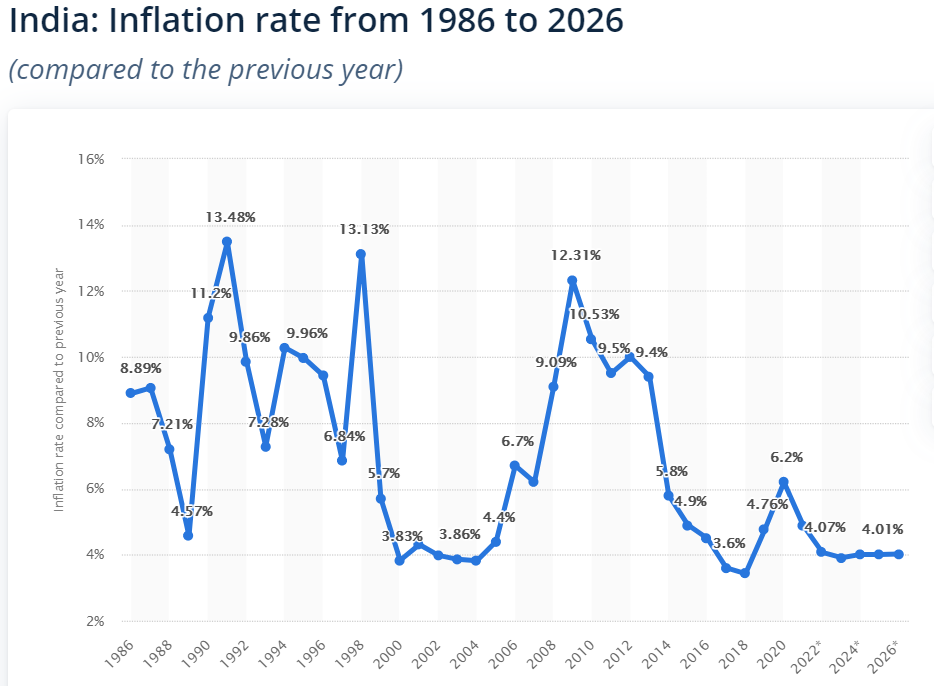

Here’s the last 30+ years of historical inflation rate in India, there are years when inflation was more than 10% as well. But let’s consider our average inflation rate at just 6%.

Let’s do the math.

Fixed Deposit interest rate : 5.4%

After tax: 3.92%

Inflation: 6%

So the real rate of returns we eventually get is -2%. So every one of you who invested in fixed deposit for long term will get negative returns.

Do you know how much amount lying in Fixed Deposits in India? Its more than 140 lac crores. That’s right. Around, 3 lac crores of wealth getting destroyed every year just like that.

It’s better to allocate your money to fixed deposit for short term only, if you need your surplus cash in a year or so, then keeping it in FD ensures some liquidity, and you can redeem it whenever you need urgent cash. But if your expectation is to invest for long term, then investing in FD is a very bad idea. You should ideally invest in index funds that can help you not only beat the inflation, it can also generate decent returns over the long run, even though market risk is there compared to FD, but over the long run, equity always outperforms any other asset class.

For more such information related to Investments, algo trading, mechanical trading systems follow us at our Blog and Youtube.