I have read many questions regarding sensibull and people from its team have always iterated that they have tested numbers for many times and all is correct.

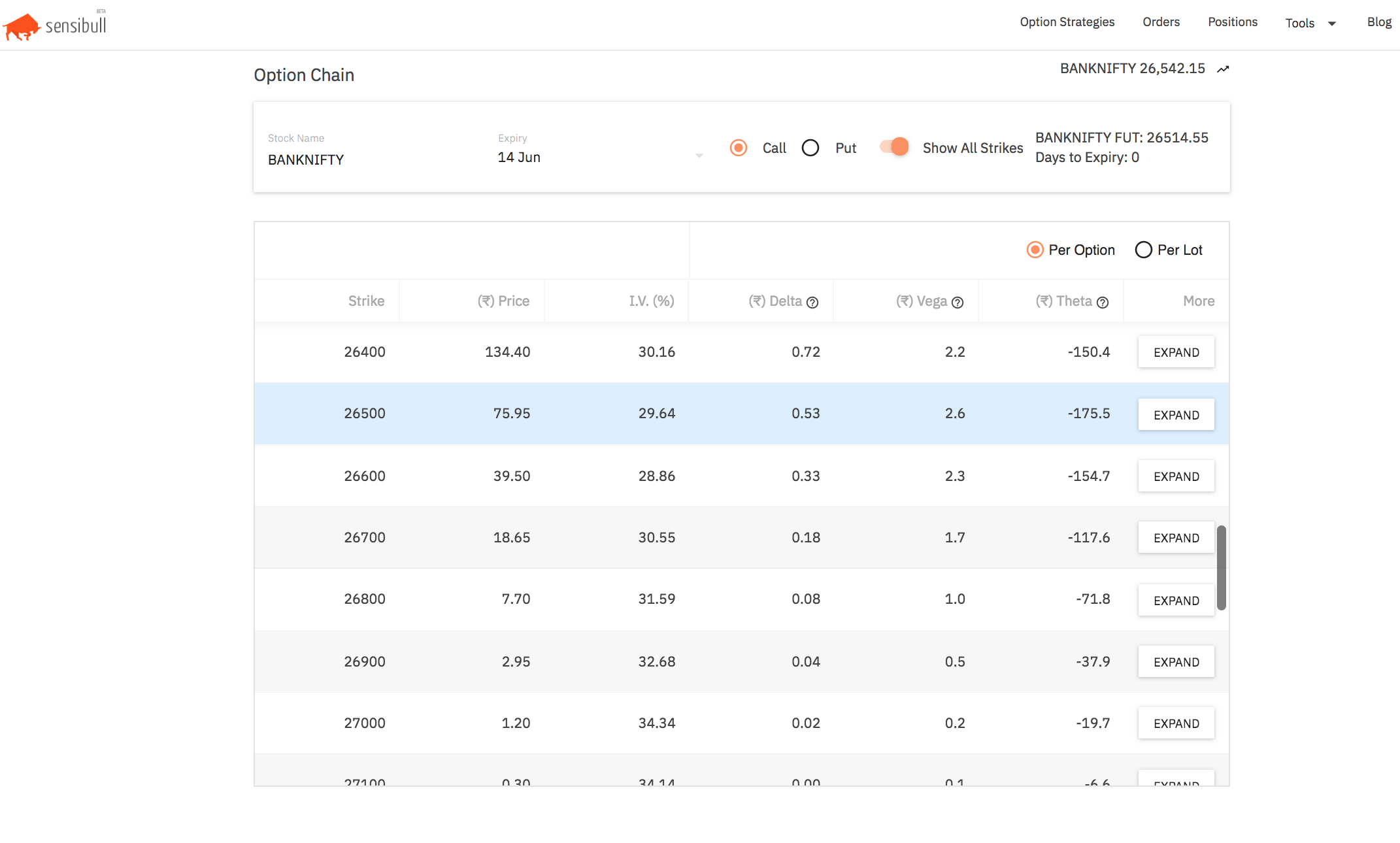

But look at the attached screenshot -

Theta is way much higher than LTP of option. This is not rare event but happens on all expiries and to all instruments, so does this mean there is major gap in greek calculation formulae of sensibull?

Trading considering those numbers will make dangerous trades and it seems numbers are way off the real thing.

That option expires today. The Theta you you see as 175.5 is a one day Theta. But now there is a fraction of a day left in trading as of now. So the price of the option, which is 75.95 which is almost all theta is Theta for the fraction of a day.

Interestingly if you see yesterday’s closing price of 26500 June PE, you can see that it closed around 180, which is almost all of the Theta value you are seeing on Option Chain, which adds up.

But what you are suggesting here makes sense from a UX perspective. Instead of showing the one day Theta, we should move towards leftover Theta for the day. It is much more meaningful than the Theoretical one day value. This one day Theta does not exist on expiry day, and adds no practical value.

If theta is shown for full day where as actual expiry is just fraction of time away, same can be said for delta, gamma, rho etc greeks.

Calculating Theta for complete last day and showing only fraction of it as per remaining time wont correct the things. You need to put correct time to expiry (till 3:30pm) which will give correct theta automatically and also other greeks will come out correct, but now it seems time to expiry is somewhere near day end and not 3:30pm so other greeks must also be behaving as per day end expiry.

How are you checking sensibulll greeks against? Is there any valid source which is trustworthy to match greeks?

This fractional Theta issue exists only on the expiry day. Also, this convention of 1 day Theta is followed pretty much across the world. In most (if not all) option calculators, if you calculate Theta with fractional days you will see that Theta turns out to be greater than the option value. It is just about the way Theta is defined. Passage of one day. Definitions don’t help much though. Also, I am not sure how many people trade intra-day on expiry day with Theta decay as the objective.

Coming to others Greeks - They are not affected by this thing. Even if I were to assume for one second that there is some fractional day issue, which does not exist, let us play it out. On the expiry day most Greeks are of hardly any consequence. They are small, and change rapidly with Gamma profile, and does not lead to any meaningful insight. For example, with 20 minutes to go or an hour to go, what does delta of 0.2 mean anyway. It is a complete spot game. Even at a scale when I am gamma scalping, I would rather not look at delta as a meaningful measure of doing anything on the expiry day. So it becomes one of those math numbers of hardly any significance. Thus, Greeks are not of use on expiry day to make trading decisions for most retail investors.

As for your last question, you can find enough sources on Greeks. If you are complete DIY person you can write an excel macro with BS formula yourself. There are excels/ macros/ web resources from almost all exchanges and well known establishments. If you want this in code, there are open source resources like NPM libraries in the intenet.

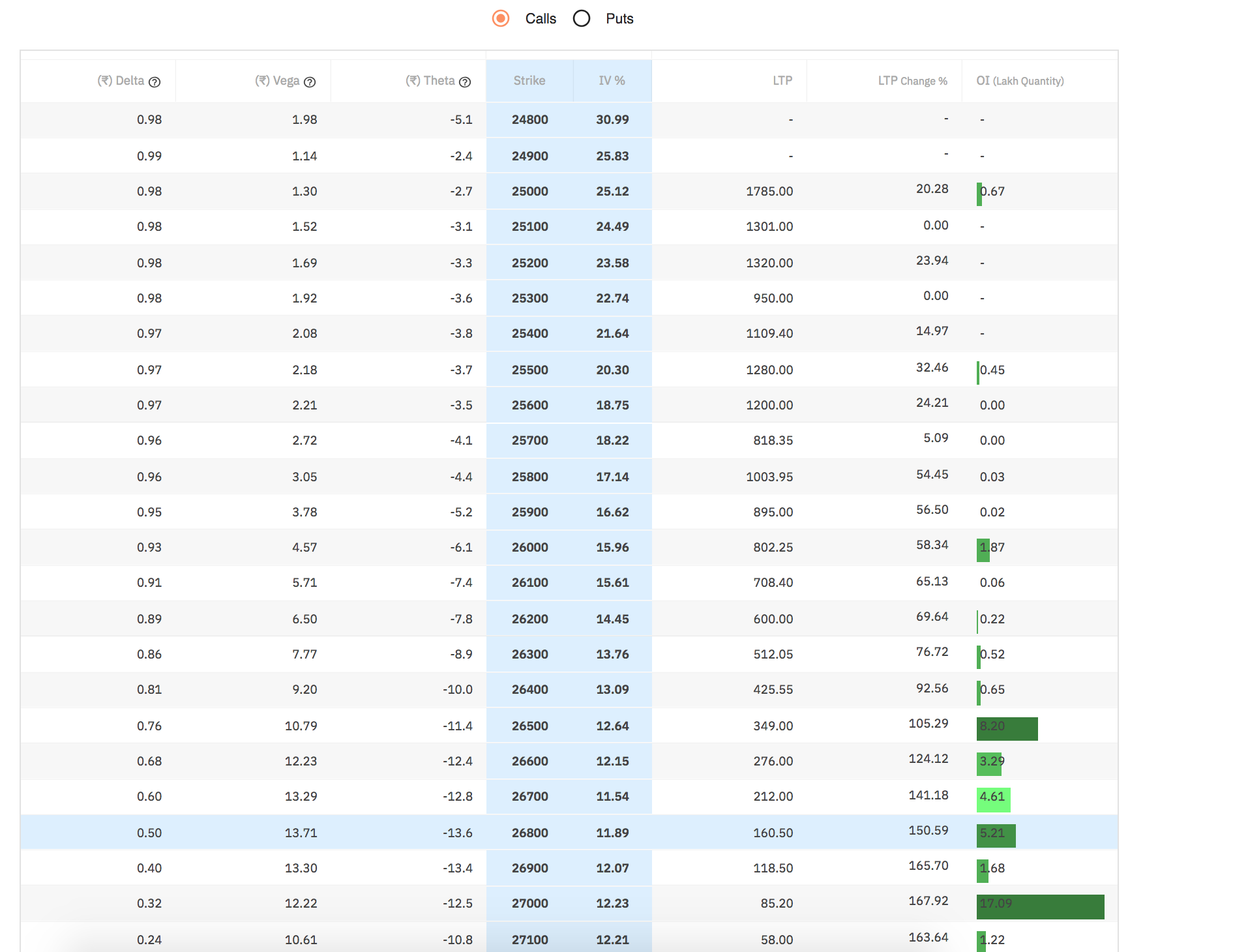

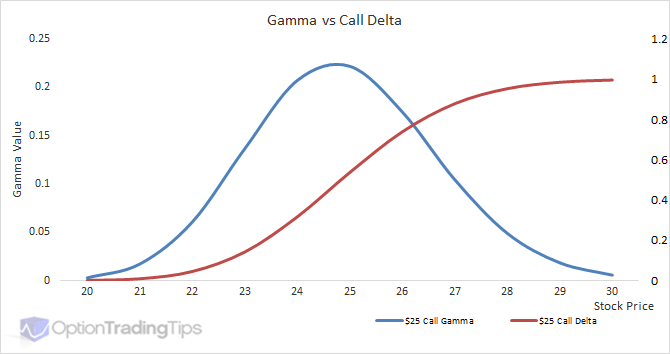

ATM delta is 0.50, 100 ITM strike delta is 0.60 (+0.10), 200 ITM strike has delta of 0.68(+0.08 than previous) and so on for all ITM strikes. This is not possible right? Delta should keep on increasing as we go ITM because of increasing gamma. but this greek calculator is showing reducing gamma as we go to ITM or OTM from ATM which is certainly not the way options behave.

Also from 26200 to 26100 its just 0.02 increase in delta for 100 points increase?

New model of putting future price seems really faulty, even it showed theta more than LTP on last Wednesday morning(not the expiry).

Delta is sure shot off and wrong in new option chain. How do you justify these calculations?

@SSR

Not really. It will be 0.9, 0.99, .0999, and so on and so forth as time reduces or spot goes more in your favor or vol decreases. It will never be equal to 1. But for all practical purposes you can use Delta of deep ITM = 1. (Very much in the money close to expiry with normal to low vols)

Sorry, that statement “Worst Performance” does not make sense. It is vacuous, and not founded on anything concrete.

To put things in perspective, we have answered all the questions here correctly, and given mathematical proof that our numbers are indeed right. Then why would you make such a statement? This is a public forum, and we all should have the courtesy and responsibility to make sure anything which we say has the right reasons.

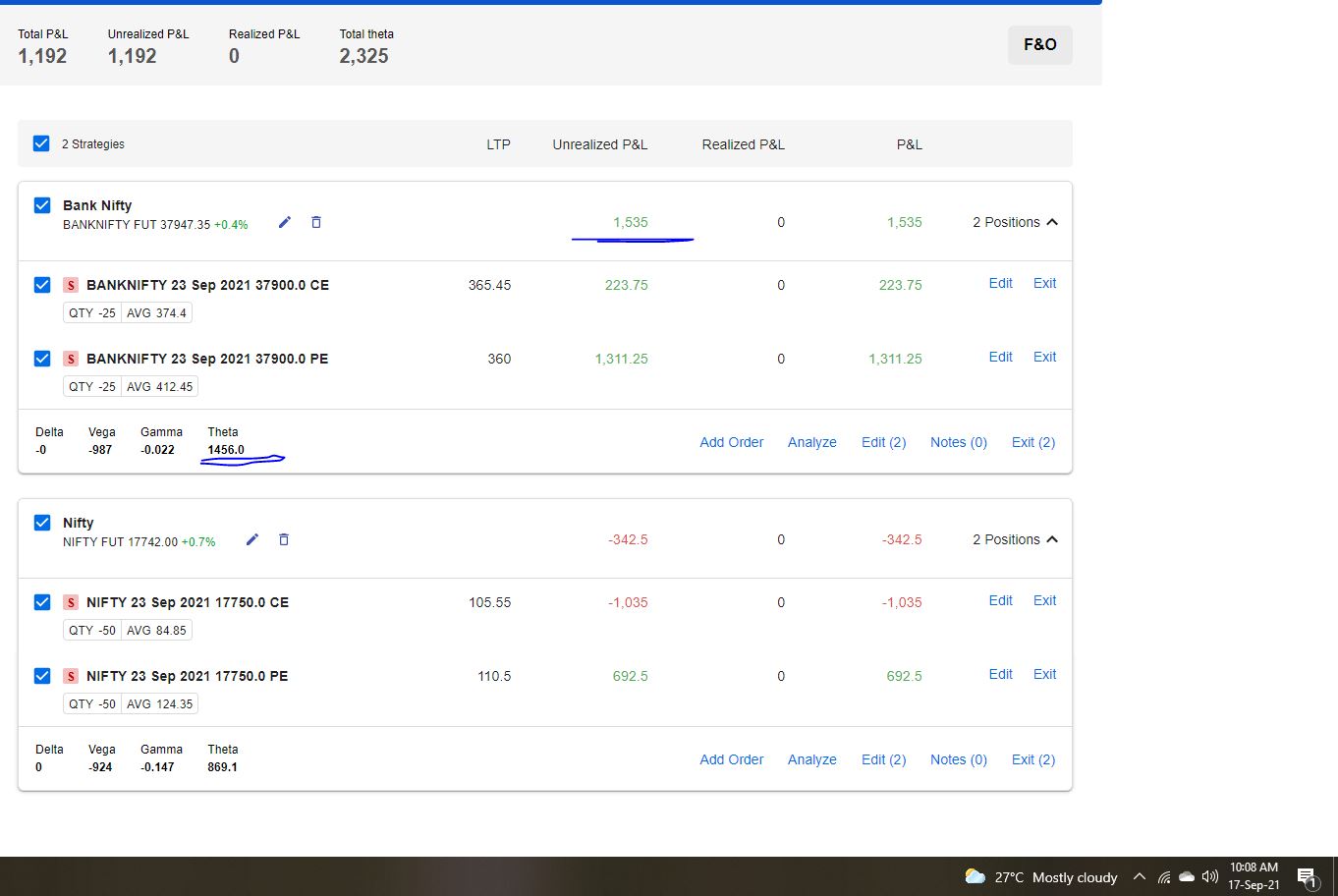

This is a virtual trade I took on your platform. Notice that your total theta for the bank nifty straddle shows 1456 but within only half hour of taking the trade (took it around 9,20 AM same morning) I’ve already earned more premium than your given value, and that too when the vix was rising so I didn’t earn any premium from volatility, it was all theta. At the end of the day (you can confirm this by looking at the chart) this straddle gave me 4100 which is waaaayyyy higher than your given number 1456. How do you justify this? oh wait…you can’t. I asked your customer service rep several times to address this discrepancy but that person never replied.