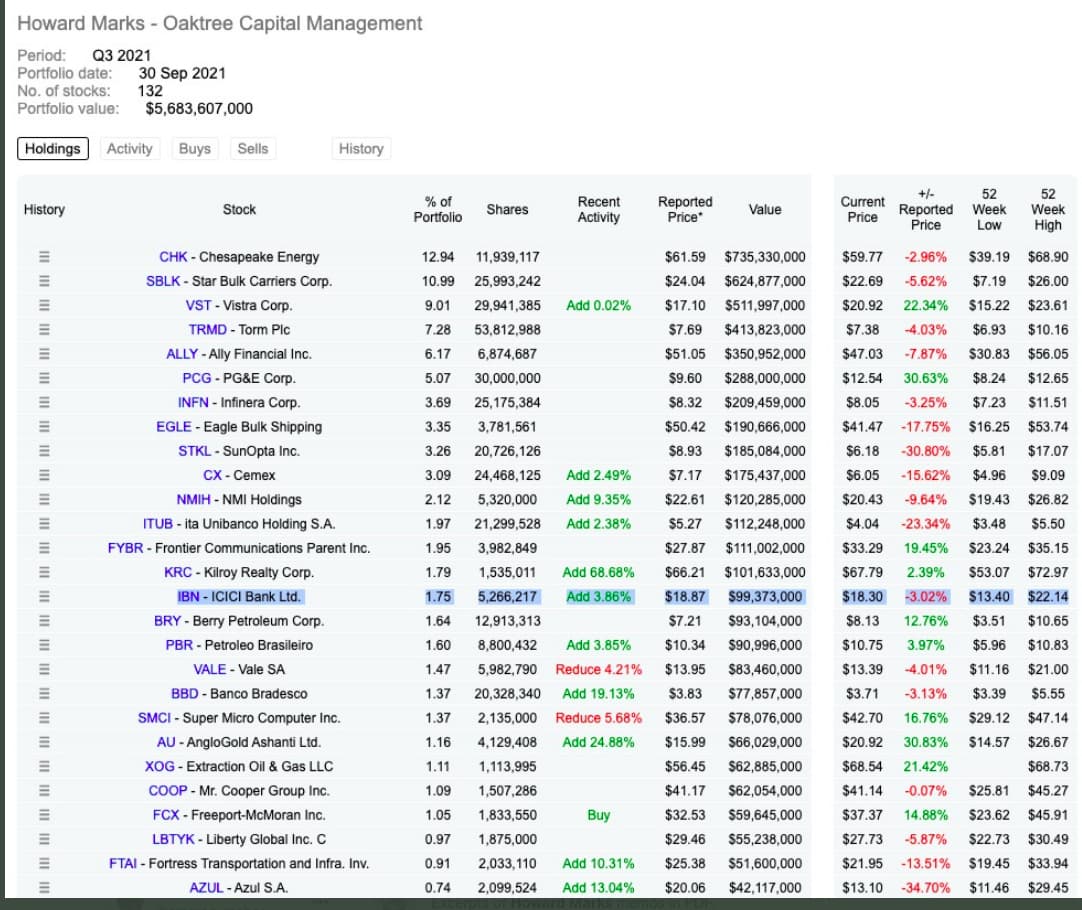

Howard Marks is the co-founder of Oaktree Capital Management, one of the greatest investors around. Unlike Buffett etc., Howard Marks specializes in high yield and distressed debt. Since Oaktree was founded, it’s has delivered about 19%. That’s quite a number given that they primarily only stick to debt, which is why you don’t hear of him often as Buffett, Munger etc, but that’s no less impressive.

He’s most well know for the memos he’s been writing since the 1990s. Funnily, for nearly 10-15years, nobody read them. He used to religiously write then physically mail them to clients. But today, they are wildly popular for the same and simple advice in them. Keeping aside investing, it also shows the importance of sticking to things for a long time. For me personally, the takeaway was: Write for an audience of one. He’s also written several popular books, some based on his memos.

I’ve always loved reading his memos, not because he gives some earth-shattering macro forecast or such. But or the absolutely commonsensical advice that he gives some of it which can seem a bit

anachronistic given the absolutely crazy environment we’re in.

Someone recently sent this PDF by this persona called Anil summarizing some of his memos and this is quite literally a goldmine. It’s a 80-page doc and you can read it over a few days, but I’m just highlighting a few things that struck a chord with me:

The right price

In short, we feel “everything is triple-A at the right price”. We have many reasons for following this approach, including the fact that relatively few people compete with us to do so. But we feel buying any asset for less than it’s worth virtually assures success. Identifying top quality assets does not; the risk of overpaying for that quality still remains.

The cycle will always turn

If you’re going to succeed at all in timing cycles, the only possible way is to act as a contrarian: catch some opportunities at the bottom, let your optimism abate as prices rise, and hold relatively few exposed positions when the top is reached. To find bargains at the bottom, you don’t have to think that things will get better forever; you just have to remember that every cycle will turn up eventually, and that prices are lowest when it looks like it won’t. But it’s just as important to avoid holding at (and past) the top, and the key is not to succumb to the popular delusion that "trees will grow to the sky”

As you know, we don’t consider ourselves good macro-forecasters (or even people who believe in forecasting). So we certainly are in no position to say when the recession or market pullback will start, how bad it will be…or even that there definitely will be one. But we think we’re unlikely to be proved wrong if we say cyclicality is not at an end but rather is endemic to all markets, and that every up leg will be followed by a down leg.

So we conclude that most of the time, the future will look a lot like the past, with both up cycles and down cycles. There is a right time to argue that things will be better, and that’s when the market is on its backside and everyone else is selling things at giveaway prices. It’s dangerous when the market’s at record levels to reach for a positive rationalization that has never held true in the past. But it’s been done before, and it’ll be done again.

Buy things people don’t want to buy

Because of the fluctuation of both fundamental developments and investor behavior, assets are sometimes offered for sale at bargain prices and at other times at prices that are too high. A technique that works most dependably is putting money into things that are out of favor. Although investors often seem not to grasp it, it shouldn’t be hard to understand: only unpopular assets can be truly cheap. And those that are in favor are likely to be dear.

Lord Keynes wrote “speculators accept risks of which they are aware; investors accept risks

of which they are unaware.” As Keynes’s definition makes clear, investing in the stocks of

great companies that “everyone” likes at prices fully reflective of greatness is enormously

risky. We’d rather buy assets that people think little of; the surprises are much more likely

to be favorable, and thus to produce gains. No, great companies are not synonymous with

great investments . . . or even safe ones.

Past performance

In contrast, highways – like markets – are dynamic environments. What the other participants do on a given day goes a long way toward determining what will and will not work for us. When people flock to the fast lane, they slow it down. And with the lane they left suddenly less crowded, it speeds up. This is how the “efficient market” in travel acts to equalize the speed of the various lanes, and thus to render ineffective most attempts at lane-picking.

Efficient securities markets work the same way to eliminate excess returns. Everyone knows what has worked well to date. Just as they know which lane has been moving fastest, they know which securities have been performing best. Most people also understand there is no guarantee that past performance will continue. What is a little less widely understood, however, is that past returns influence investor behavior, which in turn alters future performance.

Contrarian investing

The truth is, the herd is wrong about risk at least as often as it is about return. A broad consensus that something’s too hot to handle is almost always wrong. Usually it’s the opposite that’s true. I’m firmly convinced that investment risk resides most where it is least perceived, and vice versa: When everyone believes something is risky, their unwillingness to buy usually reduces its price to the point where it’s not risky at all. Broadly negative opinion can make it the least risky thing, since all optimism has been driven out of its price.

As I wrote in “Dare to Be Great,” non-conformists don’t get to enjoy the warmth that comes with being at the center of the herd. But it should be clear that when you’re one of many buying something, it’s unlikely to be a special opportunity. It’s only when few others will buy that you can get a bargain.

Going where few dare to

Our approach emphasizes the low-risk exploitation of inefficient markets, as opposed to aggressive investment in efficient ones. We restrict ourselves to markets where it is possible to know more than other investors. We put avoiding losses ahead of the pursuit of profits. And we do not seek to employ leverage. Inefficient markets must by definition entail 15 illiquidity and occasional volatility, but we feel unleveraged and expert investment in them offers investors with staying power the best route to high returns without commensurately high risk.

Sixes vs singles

It’s easy to say you should prepare for bad days. But how What’s the worst case, and must you be equipped to meet it every day? Like everything else in investing, this isn’t a matter of black and white. The amount of you’ll bear is a function of the extent to which you choose to pursue return. The amount safety you build into your portfolio should be based on how much potential return willing to forgo. There’s no right answer, just trade-offs. That’s why I went on from the as follows: “Because ensuring the ability to [survive] under adverse circumstances is incompatible with maximizing returns in the good times, investors must choose between the two.”

Avoiding mistakes

As you’ve heard ad nauseum, we chose to base Oaktree’s approach to money management on a simple motto: “if we avoid the losers, the winners will take care of themselves.” Thus we’ve endeavored to build portfolios that would give us acceptable performance if our expectations weren’t fully realized, combined with the possibility of surprises on the upside if they were. We’ve strived to match market returns in good times and do markedly better in bad times – something that may sound simple but isn’t. We chose to work in inefficient markets only, with portfolios that stick closely to their charter

We’d love to deliver great results every year, but that’s simply not possible. Instead, in short, it’s our goal to eliminate disasters, so that every year is either good or great. If a money management firm can do nothing other than produce returns that are at least decent every year, it’s sure to have an excellent long-term record. I truly can say my colleagues have done so, and that we’ve made money for our collective clientele every year since Oaktree opened its doors

Survive first, maximize returns later

If you know what lies ahead, you’ll feel free to invest aggressively, to concentrate positions in the assets you think will do best, and to actively time the market, moving in and out of asset classes as your opinion of their prospects waxes and wanes. If you feel the future isn’t knowable, on the other hand, you’ll invest defensively, acting to avoid losses rather than maximize gains, diversifying more thoroughly, and eschewing efforts at adroit timing. Of course, I feel strongly that the latter course is the right one. I don’t think many people know more than the consensus about the future of economies and markets. I don’t think markets will ever cease to surprise, or thus that they can be timed. And I think avoiding losses is much more important than pursuing major gains if one is to achieve the absolute prerequisite for investment success: survival.

Peaks of ecstasy vs troughs of despair

If I were asked to name just one way to figure out whether something’s a bargain or not, it would be through assessing how much optimism is incorporated in its price.

No matter how good the fundamental outlook is for something, when investors apply too much optimism in pricing it, it won‟t be a bargain. That was the story of the Internet bubble; the Internet was expected to change the world, and it did, but when the optimism surrounding it proved to have been excessive, stock prices were decimated. Conversely, no matter how bad the outlook is for an asset, when little or no optimism is Incorporated in its price, it can easily be a bargain capable of providing outsized returns with limited risk.

Even with a bad “story,” the price of an asset is unlikely to decline (other than perhaps in the very short term) unless the story deteriorates further or the optimism abates. And if there‟s no optimism built into its price, certainly the latter can‟t happen. It was primarily this line of reasoning that allowed me to feel positive in the teeth of the financial crisis in late 2008. The outlook was as bad as it could get – total meltdown – and prices clearly incorporated zero optimism. How, then, could buying be a mistake (providing the world didn‟t end)?

On macros

Investing means dealing with the future – anticipating future developments and buying assets that will do well if those developments occur. Thus it would be nice to be able to see 21 into the future of economies and markets, and most investors act as if they can.

Thousands of economists and strategists are willing to tell us what lies ahead. That’s all well and good, but the record indicates that their insights are rarely superior, and it’s never clear why they’re willing to give away gratis their potentially valuable forecasts.

We believe consistently excellent performance can only be achieved through superior knowledge of companies and their securities, not through attempts at predicting what is in store for the economy, interest rates or the securities markets. Therefore, our investment process is entirely bottom-up, based upon proprietary, company-specific research. We use overall portfolio structuring as a defensive tool to help us avoid dangerous concentration, rather than as an aggressive weapon expected to enable us to hold more of the things that do best.