I knew this question would come up but for the sake of simplicity, I didn’t write it. In hindsight things are easy. If you pick any of the top performing you looked at today, there is no guarantee that the fund is going to deliver similar performance. Mean reversion is the truth in the markets. What has done well historically has to do worse.

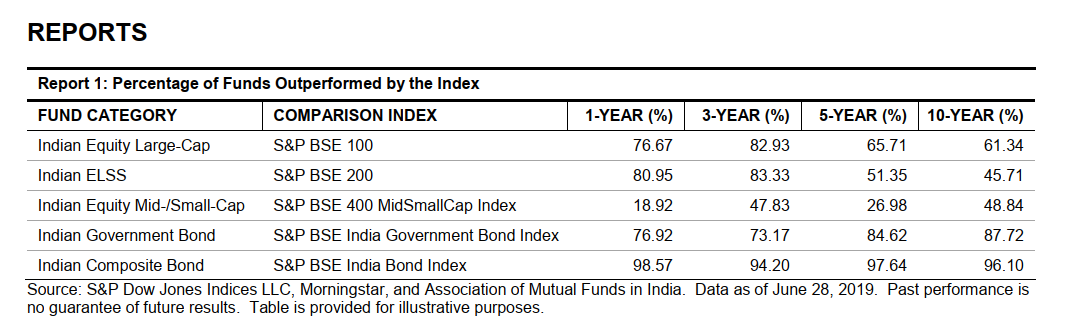

Even historically over 50% of mutual funds across categories have failed to beat the respective benchmark indices.S&P publishes a periodic report called SPIVA which analyses this.

Picking a good performing fund in advance is hard. But in the large-cap space it is pointless to pick a large-cap fund. Large-cap funds charge up to 2%, but you can get Nifty 50 exposure for 0.09%, and NIFTYBEES ETF fro 0.05%. In the mid-cap space, there is a case to be made for picking active funds but the dispersion in performance there is reducing, meaning all funds on average will pretty much do the same. Motilal has lunched the first Mid-cap index fund, which makes indexing easirer.

Small-caps are hard to but but Motilal has a fund for that too. But I don’t even know why people invest in small-caps, they are useless.

Now coming back to the original question, why are funds finding it difficult to beat benchmarks?

-

Strict categorization guidelines. Earlier, funds had the relative freedom to do what they want. Even if a fund was from the large-cap category it used to hold mid-caps to juice returns. This is no longer possible. SEBI has strictly defined the category and stocks to invest. Large-cap fund can only invest in the top 100 stocks. If all the 40 AMCs can only do that, where will the outperformance come from?

-

Mandatory benchmarking to total return indices

What is total Return Index index and how is it calculated? - #4 by portfolioplus911 -

High costs. Indian funds even by global standard charge too much.