Zoltan Pozsar’s latest insights on Adapting to the New World Order covers a wide range of topics. Here’s a summary of his interview with Incrementum AG in collaboration with In Gold We Trust(IGWT).

Why are central banks stockpiling gold and do you think that is going to accelerate?

Yes, I think it’s going to accelerate. The way central banks manage their foreign exchange reserves is going to go through transformative change over the next five to ten years.

One reason is that geopolitics is a big theme again; we are living through a period of “great power” conflict between China, the US and Russia and their various proxies.

The dollar will still be used as a reserve currency in certain parts of the world, but there will be other parts where that’s no longer going to be the case.

One example would be Russia. Russia’s forex reserves have been frozen. That means that their dollars and euros and yen assets became unavailable for use.

They will be looking for other reserve assets as an alternative.I think gold is going to feature very prominently there. As a matter of fact, since the outbreak of hostilities in Ukraine and the freezing of Russia’s forex reserves, foreign central banks’ purchases of gold has accelerated quite a bit.

Why central banks hold Forex reserves?

-

You need to import oil and wheat and whatever you don’t produce at home, and the price of commodities is denominated in US dollars and it’s invoiced in US dollars. There’s no way around it. Essentials that you import are priced in dollars.

-

When the local banking system has dollar liabilities and there’s some crisis, you have to provide some backstop to that; or if your corporations borrow too much offshore in US dollars, and they run into problems, you will have to cover that.

-

There is a new theme where, in addition to gold, foreign central banks are going to start accumulating currencies other than just the dollar because there will be more oil that’s going to be invoiced in renminbi and other currencies. It’s no longer the case that countries can rely only on dollars to import essentials that they need.

In a multipolar world, will there be one single reserve currency, or do we have to get rid of that thought?

I think there will be three dominant currencies: the US Dollar, the Chinese Renminbi, and then the Euro is going to be like a third wheel.

China is reducing the dollar’s weight in its basket, but it’s increasing the euro’s weight. It’s kind of a hard question to answer because Europe is a great prize in this “great game” of the 21st century, which China is going to be playing on the Eurasian landmass and in Africa and the Middle East.

Economic Blocs

-

There are basically the two “economic blocs”. If you think about the macro discourse, we are talking about the aligned countries and nonaligned countries.

-

Everything that you see in terms of supply chains and globalization is going to also happen in the world of money, because supply chains are payment chains in reverse.

-

If you realign supply chains along the lines of political allegiance – who is your friend and who is not – you will also realign the currency in which you will invoice some of these supply chains and trade relations. Eurasia is looking like a renminbi slash gold block. Then what we refer to as the G7 looks like a dollar block. I think Europe is a question mark in there. It’s going to be fought over.

Q: How do you differentiate between a reserve currency and a trade currency? I think for the Renminbi to become a trade currency for trading oil and gas is pretty easy. But to become a reserve currency, wouldn’t they have to open up their capital accounts, deepen their capital markets, and let the Renminbi start to float?

Babies are not born walking and talking and trading interest rates; it’s a 20-year journey.

The US Dollar has gone through all of that. After the Second World War, when we read the history books, it became the reserve currency, but it was still a journey to get there. Post-war reconstruction of Europe and Japan and the Marshall Plan. The US was running current account surpluses, much like China is running current account surpluses today. The US was providing financing to Germany, the UK and Japan to import all the stuff from American companies that they needed to build out their industries.

I am amazed when people say that China and the Renminbi are becoming something big, but they have a current account surplus, so they cannot become a reserve currency. The US Dollar became a reserve currency with a current account surplus. It’s just that things later changed and then they turned to running a deficit.

The young generation of traders and market participants conceptually understand the dollar as a reserve currency, but are unaware that that status was born out of a surplus position.

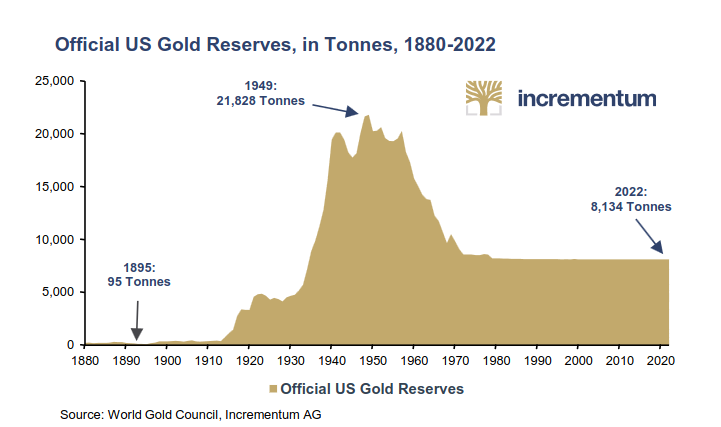

The US and Gold reserves

The US also had more than 20,000 tons of gold, which was pretty important in establishing that trust in the dollar.

China’s way to make Renminbi mainstream - Swap lines

There’s also a mechanism through which China is going to provide the world the Renminbi that the world doesn’t have but will need in order to import stuff from China, and that’s swap lines. It’s not going to be like a Marshall

Plan, but there are mechanisms through which China is going to pump money into the system.

The second thing is that China reopened the gold window in Shanghai with the Shanghai Gold Exchange. There’s that convertibility of offshore renminbi into gold if someone so wishes; that’s another important feature. Renminbi invoicing of oil has been happening for a number of years now, with all the usual suspects – Russia, Iran, Venezuela – but now it’s going to happen with the Saudis and the GCC (Gulf Cooperation Council) countries at large. We are

starting to see copper deals that are priced in renminbi with Brazil.

The money you have in the Western banking system is only yours if the political process that those banks ultimately report to or exist in allows you have access to this money. When that trust is broken, you start building out your alternative payment and clearing systems

China and the BRICS (Brazil, Russia, India, China and South Africa) countries are basically doing with the Renminbi all these steps that don’t seem to add up to much when you read about them in isolation; but when you look at them in the totality of things, and when you take a 10-year perspective about what they have been building, it adds up to quite something.

China is not blocking capital outflows

The other thing I would say is there’s a capital flight from China. People want to keep their money anywhere but in China. Although certain countries have no option but to keep their money in China, other people want to keep their money elsewhere. I think it’s important to point out that China is not blocking those capital outflows with capital controls

Depending on how you look at these things and the perspective you want to take, things are moving in a direction where a large part of the world is going to use the renminbi to a much larger extent. That’s a path toward becoming a major trade and reserve currency.

The other thing I would say about the reserve currency question is this: people have stashes of dollars because you need them in a crisis. That kind of thinking and that body language if you’re a central bank, came of age in an era

where you didn’t have the dollar swap lines. And because you knew that if you’re short dollars, the next thing you’re going to have to do is go to the IMF and That’s going to be very tough and painful. China has a swap line with everybody. As a result, nobody will have to hoard renminbi to be able to trade with China. Had these swap lines existed in the 1980s, Southeast Asia would have had a different financial crisis than in 1997 – it was a liquidity crisis. These days, we deal with liquidity crises through swap lines.

I don’t think that the journey for the renminbi to a reserve currency is that countries will start accumulating it; it’s going to be managed through swap lines.

I keep on re-reading President Xi’s address to the GCC leaders; there’s a lot to unpack there. He says, “We are going to trade with each other a lot more and we are going to invoice everything in renminbi” and "You will have a surplus, I will have a deficit; or I will have a surplus and you will have a deficit, and then there’s going to be an interstate means of how we are going to recycle and manage the surpluses and deficits”.

Would you agree that we should not be too scared of global conflict or war, as it could also have positive effects like innovation, higher productivity, and so forth?

We need to be careful here, because we don’t want to reimagine history here, going forward. With the Napoleonic Wars and the Crimean Wars and First and Second World War, physical resources, land and industries, that’s the stuff you fought over. It’s hard to imagine that all conflict in the future will be about bits and bytes and data and spreadsheets and balance sheets. There is risk here. I think war is not good, because it’s a very risky game. Now, it usually happens in the domain of trade and technology and money, and then it spills over into uglier Forms.

I don’t think that war is good. Yes, it is going to be a catalyst for change, and this is going to mean a lot more investments. As I articulated in my thesis, we are going to pour a lot of money into rearming, reshoring, friendshoring, and energy transition. But again, all these themes are going to be very commodity-intensive and very labor-intensive.

It’s going to be “my commodity” and “my industry” and “my labor” versus yours. It’s not just a US versus China thing, it’s a US versus Europe thing as well, so it’s going to be very political. None of these things are going to be interest-rate-sensitive. The US Fed can raise interest rates to 10%; we are still going to rearm; we are still going to friendshore; we are still going to pursue energy transition; because these are all national security considerations, and national security doesn’t care about the price of money, i.e. interest rates.

Maybe 5-10 years down the road we are more self-sufficient and such, but I think the next five years are going to be complicated from an exchange-rate, inflation, and interest-rate perspective. My “War” dispatches were not “happy” pieces.

Would you say that the first inflationary wave is over and that we should expect more inflationary waves?

2% inflation and going back to the old world, I don’t think it stands a snowball’s chance in hell. Low inflation is over and we’re not going back. There are a number of reasons for that.

1. Inflation has been a topic for three years now. We started to fight it a year ago, but it’s been a part of our lives for much longer. The CPI is up, I think, 20% since the pandemic and wages are up about 10%. There’s still a deficit in terms of what your money buys versus this statistical artifact that’s the CPI.

There’s a saying: “Inflation expectations are well anchored when nobody talks about inflation”. Now, it’s increasingly hard to talk to any investors without talking about inflation. So, inflation expectations are not well anchored anymore.

2. Wall Street and investors are very young. :

This is an industry unlike physics, where we all stand on the shoulders of earlier giants and where knowledge is cumulative. Finance is cyclical; you make your money in the industry and then you retire and grill tomatoes. Then everybody else has to relearn everything you knew and again retire that knowledge as they go along. If you’re young, let’s say 35-45 years old, you haven’t really seen anything but lower interest rates and low inflation. In terms of how you think about inflation, it’s a new skill you have to acquire, because it’s not a variable you had to think about in the past.

What that means in practical terms is that there’s this tendency to think about inflation as if it was another basis on a Bloomberg screen that blew out, and it’s going to mean-revert. What do I mean by that? At your age and my age, our formative experiences in financial markets are the Asian Financial Crisis, 2008, some spread blowouts since 2015, the Covid pandemic; all of these things were crises of bases where FX spreads were broken, and then AAA Collateralized debt obligations (CDOs) and AAA Treasuries turned out to not be the same thing. There was a basis between those two, and the cash/Treasury futures basis broke down in March of 2020, when the pandemic hit and we didn’t really have a risk-free curve for a couple of days until the Fed stepped in.

These are all easy things, because all you need to do to fix these dislocations is, you throw balance sheet at the problem, which in English means someone has to provide an emergency loan or you have to do Quantitative easing QE and pump money in the system; and then, once the money is there, the basis dislocations disappear.

Just as the UK had this mini budget problem, we have the problem with SVB. All we had to do is say, “Here, we give you money, we guarantee deposits, problem solved”. So, these are easy problems With inflation there is a clear difference.

On Paul Volcker and how there were different back then and now

I think we are in love with this idea that Paul Volcker is a national hero because he raised rates to 20% and “that’s all it takes to get inflation down”. Well, not really. Paul Volcker is a legendary policymaker, but he was lucky due to the following 2 reasons:

- The OPEC price shocks that precipitated the inflation problems happened in the early 1970s. When prices go up, people start drilling more; and supply increased in that decade after the OPEC price shocks.

This was the period when the North Sea oil fields were developed, and Norway started to pump in the North Sea and Canada drilled more and Texas drilled more and we were just swimming in oil. Then Paul Volcker arrived in the early 1980s, raised interest rates and caused a deep recession, and the demand for oil and oil prices collapsed. So that’s fantastic. More oil, less demand. That’s how you get inflation down.

- The second thing was the labor force back in Volcker’s time. There were more people working because of the boomer generation, and female labor force participation was going up, so there was a lot of labor coming in. Also, the politics around wages was changing, because in 1981 President Reagan famously fired air traffic controllers because they dared to go on strike. So, it’s easy to get inflation down when energy and labor are going down for fundamental reasons. There’s more supply, and politics is supportive.

Today’s time - Elevated geopolitics and Tighter labour market

Today, oil prices are elevated and we haven’t invested in oil and gas for a decade. Geopolitics is just getting worse. For Volcker it had gotten worse the decade before, and he was dealing with a very stable geopolitical environment by the time he was fighting inflation.

Now, the oil market and all other commodities are tight and geopolitics is getting nastier – look at the OPEC production cuts. OPEC+ wants to target USD 100 per barrel; we are below that. Probably they are going to cut

more to get up to where they want to be in terms of target. The SPR has never been lower in history.

Labor? Very different from Volcker’s backdrop. The baby boomers are retiring, and millennials just don’t hustle as much as boomers did. The older millennials, the young generation today, all go to college; but they don’t have to work on the margin to put themselves through college, because student loans are flowing from the faucet, and their parents are richer, so the parents are going to put them through school. When you look at the boomer generation, their parents weren’t wealthy and their student loans were not as easy to come by, so they had to do odd jobs at restaurants and God knows where in order to make some money on the margin, to put themselves through college.

That was part of labor supply for lower-end restaurant and hospitality jobs. Those things are missing today. We have a stagnant labor force participation rate that’s actually falling on the margin; and we have a severe labor shortage, which only immigration can fix. But that’s not an easy solution and it’s also quite political. We

have a skills gap where most of the jobs don’t require a college degree, but everybody that’s entering the labor force is overeducated for some of these jobs. That keeps the labor market from clearing.

I would say that people tend to overthink inflation and get technical about core inflation and this and that. There are two things to keep in mind. The labor market is ridiculously tight. I don’t think unemployment is going to go up much during this hiking cycle. Because, if you’re an employer and you’re lucky enough to have the staff you need, you’re not going to get rid of them, because you will have a hard time hiring them back. If unemployment doesn’t really go up, the wage dynamics are going to remain robust in a very tight labor market; and that matters for

services inflation, which is determined by the price of labor.

Then, on the other side, what you need to look at are the prices of food and energy, both of which are stochastic, and they are caught up in geopolitics. So, if you want to take a guess: Food and energy prices, do they have more upside or downside?Probably more upside, because things are tight, things are geopolitical, mine versus yours. And that’s necessities

If the price of necessities is going up,and the labor market is tight, there’s going to be a lot of feedthrough from higher headline inflation to higher wage inflation; and core goods, whatever that is, doesn’t really matter as much. This is the price of flatscreen TVs and the price of used vehicles. Frankly, if you’re the Federal Reserve, you’re not going to care about used vehicle prices and the price of flatscreen TVs and D-RAM chips and all that stuff, because it’s not the type of thing that is going to determine what people are asking for in terms of wages.

I like to say that people go on strike not because the price of flatscreen TVs goes up, but because the prices of food, fuel and shelter go up and you can’t make a Living.

Rate cuts by end of the year seems wishful thinking

We don’t really have much progress to show for all these interest rate hikes. Housing is slowing and demand for cars is slowing, but unemployment is still very low.

When you look at the earnings of consumer staple companies like Nestlé or Coca Cola, or P&G, you don’t really see the economy falling off a cliff. People are eating at price increases, and it’s not like they are spending less. It’s going to be a persistent problem, and it’s just wishful thinking when the market thinks that we are going to be cutting interest rates by the end of the year.

I think it’s important to think about inflation in cyclical terms near-term, as in what happens to it because of the hiking cycle. What I just told you there is, inflation is probably going to be stickier than you think. Definitely for the next one or two years. Tight labor markets, high wage inflation, core inflation, all well above target, around 4-5%

The second thing is these industrial policy things that we talked about. Rearming and re-shoring and energy transition; this is going to be like an investment renaissance that’s coming. We can already read about the Inflation Reduction Act with billions in investment so far in its first year, and There’s a lot of stuff coming. Recessions are usually not associated with an investment boom. The longer inflation persists, and if the Federal Reserve doesn’t manage to drive us into a recession where unemployment goes up meaningfully, I think we’re going to run out of time, because all these investment themes are gathering momentum. And once they gather momentum, as I said, it’s going to require a lot of labor and a lot of commodities. That’s just going to add to the inflation problem and it’s going to make the Fed’s job more complicated.

How do you invest for this environment; what assets do you expect to do well?

I think this means all sorts of bad things for a 60/40 portfolio, the standard portfolio construction. At the very least, you need to do something like:

20/20/20/40. Meaning 20% cash, 20% commodities, 20% bonds and 40% stocks.

Cash and commodities make sense to me for the following reasons:

-

Cash used to be like a dirty asset, because it didn’t yield anything. But cash now yields a substantial amount. We shouldn’t be punting on the back end of the curve at about the 10-year yield, because if the market is wrong about recession and rate cuts and inflation,the US 10-year Treasury yield is going higher, not lower from here. When the yield curve is inverted, cash is actually a very nice asset; it gives you a very decent yield, the highest yield along the curve; and it gives you option value, which means that if you find some great assets to buy, you can.

-

Commodities are under-invested and are fundamentally tight; geopolitics is messing up commodities and resource nationalism is on the rise. Even if the supply is there, it’s going to come with special terms attached, and that’s going to mean higher prices, not lower.

On Bitcoin

The dollar and the renminbi and gold and money and commodities. I think they are all going to get caught up.

I’m aware that everything that I have been writing about and saying in terms of the changing monetary order and commodities and energy and money and gold, is smack in line with the Bitcoin thesis.

- There are two things that I always hear in my head. One thing is what Paul McCulley taught me, which is that money is either a purely public or a public private partnership; but a purely private form of money that is not sanctioned by any state is an interesting concept. Let’s put it that way. Certainly, I think it incorporates a lot of the themes we have talked about: You can’t print it, it’s kind of outside money, no state controls it. All of these are positives, but I would say that I’m searching for that state link to it. I think that’s what remains a question mark for me.

I also find it comical that central banks in the West are trying to do Central bank digital currencies (CBDCs) because that’s how they want to take the wind out of Bitcoin’s sails or something. I guess they don’t get it that the people that buy bitcoin don’t buy it because it’s digital, they buy it because it’s outside of state control and it cannot be printed.

- Because of its limited supply, it’s a better store of value. That’s what I would say about Bitcoin, that it’s kind of a purely private form of money, and I don’t know which state we are going to attach it to, and if you don’t attach it to a state, it’s kind of a unique point in history. Because money’s usually a state-backed thing.