The Board of Directors of REC Limited at its meeting held on November 06, 2020, declared an interim dividend of Rs. 6 per share, the ex-dividend date being November 13, 2020.

SEBI has prescribed a framework to the exchanges for adjustment of corporate actions in derivative contracts at the time of the corporate action. The exchange has published everything regarding the adjustments in case of corporate actions here. Accordingly, if a company declares a dividend at and above 5% of the market value of the underlying security, it’ll be deemed as an extra-ordinary dividend and the exchange will take actions in the adjustment of the futures and options contracts in the underlying security.

Since the dividend declared by REC Limited was above 5% of the market value of the security, the exchange has published this circular on the adjustment of F&O contracts in REC Limited on the ex-date which is November 13, 2020.

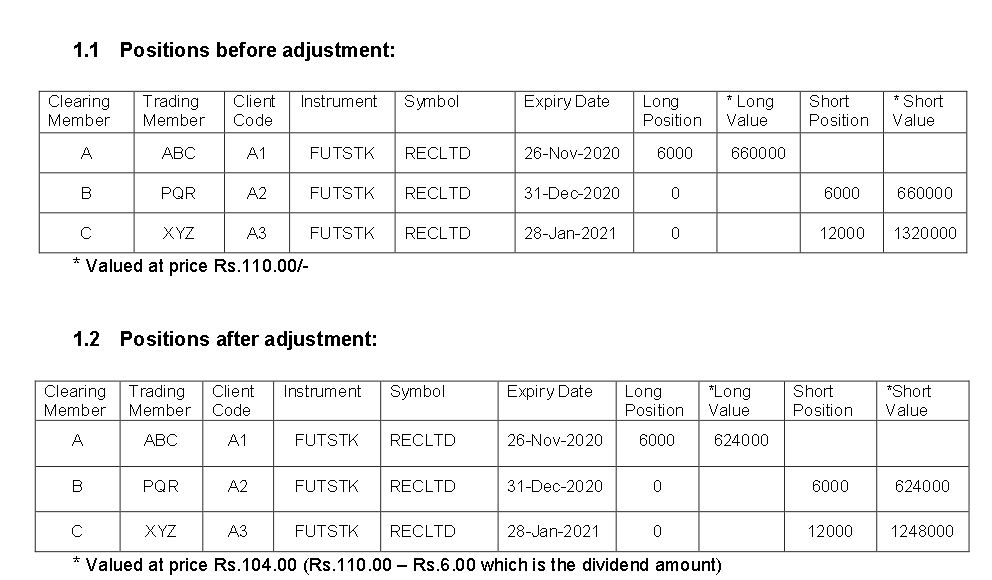

Adjustment for future contracts:

All positions in futures contracts of REC Limited would be marked-to-market on the last cum-dividend date i.e. November 12, 2020, based on the daily settlement price of the respective futures contract. Subsequently, open positions shall be carried forward at the daily settlement price less Rs.6.00 (dividend amount) for the respective futures contract.

From November 13, 2020 (ex-dividend date), daily mark to market settlement of the futures contracts would continue as per normal procedures.

Assume you bought 1 lot of REC Limited futures on November 12th, 2020 at Rs. 108 and the daily settlement price at the market close is Rs. 110, you would have made a mark to market profit of Rs. 2 per share. On November 13th, 2020, the previous day’s position will be carried forward at Rs. 104 (i.e., 110 - 6). If the closing price on November 13th is Rs. 105, you’ll make a mark to market profit of Rs. 1 per share.

Adjustment for options contracts:

The full value of dividend i.e. Rs.6.00 would be deducted from all the cum-dividend strike prices on the ex-dividend date. All positions in existing strike prices shall continue to exist in the corresponding new adjusted strike prices.

For instance, the strike price of Rs. 110 call option will be reduced to Rs. 104 on November 13th, 2020 and the positions in Rs. 110 call option will continue to exist in Rs. 104 call option.

The lot size of the F&O contracts will not change. Also, if you hold equity shares of REC Limited in your demat account as on November 17th, 2020 you will be entitled to receive the dividend.