Kindly guide me in finding a good bank saving account for monthly income and expenses. I have a separate savings account for investments And all demat accounts are linked to it.

Use of this savings account:

Getting Salary

Keeping money for expenses of around 2 months (Maybe around 1Lakh)

No I am an electronics engineering. I have nothing to do with banks.

Just to prove that I am not from Indusind bank, I request everyone to do good research before opening a bank account. And be careful of small banks like IndusInd Bank as they may have many negative points listed below:

Few branches

Few atms

Low quality of service

Slow resolution of problems

They may get closed anyday

For maximum safety and convenience open a bank account with big banks like hdfc, icici and axis.

Even if any problem happens with them, govt and media will make them provide the solution quickly.

In case any problem happens in a small bank like indusind bank, there might be no one to listen to your problem.

As stated above personally I have my investments through hdfc and axis banks.

I am looking for a small bank for daily transactions so that I can earn good interest rate on the money kept for monthly expenses.

And even in the post you quoted, I am asking about how can Indusind bank give benefits? There must be a downside.

And the condition conclusion was that we have to keep huge amount of money in bank account. And that is just pointless as it will be losing its value to inflation.

Therefore, in that thread I help to prove that all the good points shown by indusind bank comes at a great cost so better to avoid such hifi bank accounts.

I dont have, but one of my friend have… and i know that you can easily run day to day activities, but i cannot assure you in high end transaction like neft, rtgs, etc.

Thank you @TIMEFRAME

I checked both of these…

Post office saving account: Interest rate is really good (4%), but the ATM withdrawal limit is low 10k, 25k

Canara Bank: Interest rate is low…

I feel it’s more difficult to get the work done in government banks than in private banks…

Although private banks can also make you suffer, but it will be less than govt banks.

Most banks who offer higher rates on savings account i.e Listed Small finance bank pay on a tiered basis based on the balance held. as you expect the amount to be deposited is around 1 Lack, most banks pay 3 to 3.5%.

If balance is in the range of 5 to 10 lakh then it is worth while searching for a bank who offers the highest tiered rates. I am sure your existing bank must be giving 3 to 3.5%

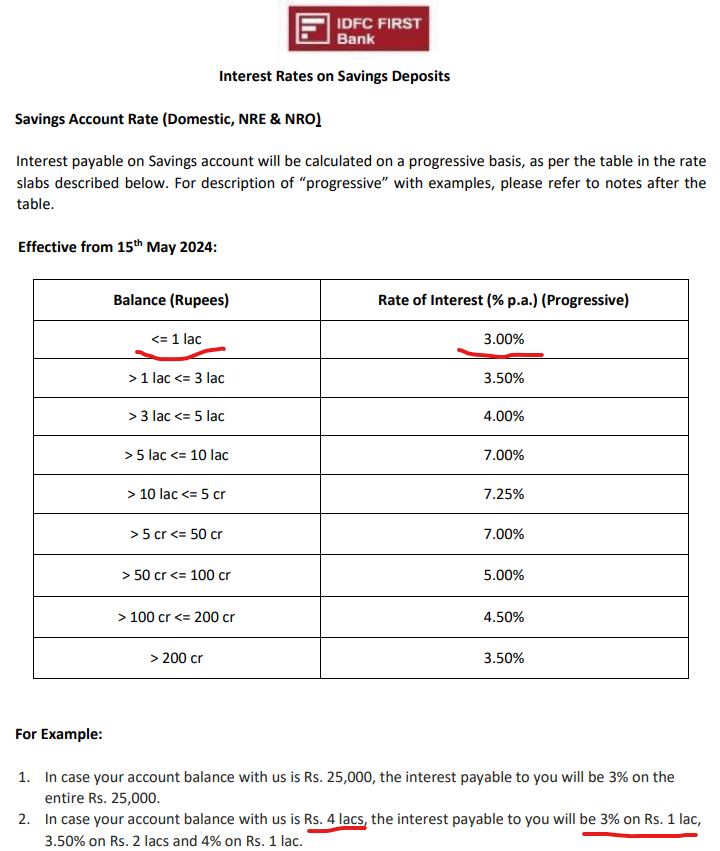

However, IDFC pays high interest on the amount above 5 lakhs. (check image below)

And since I only want to keep around 1Lakh, I will get 3% interest only. Which is same as any other bank.

I wasn’t aware of this change. Earlier they used to pay 6 percent irrespective of the balance. I never bothered to calculate after that. Thanks for pointing it out to me.

That was many moons ago. They were the first bank to offer 7%, For the last several years, they are on tiered basis and most of the banks are on this basis including SBI, the only difference is their tier is less than 10 Cr at 2.70.

Axis and Icici less than 50 L - 3%.

DCB is the lowest at 1.75% upto 1L and highest being RBL at 3.75 upto 1L

Then there is a bank called Unity small finance bank - 6% upto 1 Lack. (Please do recheck about this)

Utkarsh small finance bank gives 4% upto 1L

No, my friend. Institutions like banks, AMCs, and insurance companies can’t get closed any day they want or get into trouble. There are strict regulations for them. For example, AMCs have to put some other companies as guarantors and insurance firms to keep enough liquidity to fund the claims with IRDAI and other entities. Also, a bank comes with DICGC which is a kind of insurance that guarantees the safety of up to 5 lakh rupees of funds even if the bank fails (no matter how big or small except for cooperative banks). The government would never allow a bank to fail, they would bail it out. Look at Yes Bank for example. And by the way, IndusInd bank is not a small bank, it has a market cap of 1.14 lakh crore and is a part of Nifty 50.

PS: Not promoting Indusind bank, just clarifying the myth.

)

)