This is a continuation of this post I wrote In the previous post we saw how interest rates have hit record lows. One common narrative that keeps coming is that low interest rates are pushing people to take more risk. This isn’t incorrect but I’ve always wondered about just how this risk is transmitted through the financial markets and how it manifests. So, this post is a bit of an exploration on how low interest rates push various actors in the markets to take on more risk and go out on the risk curve.

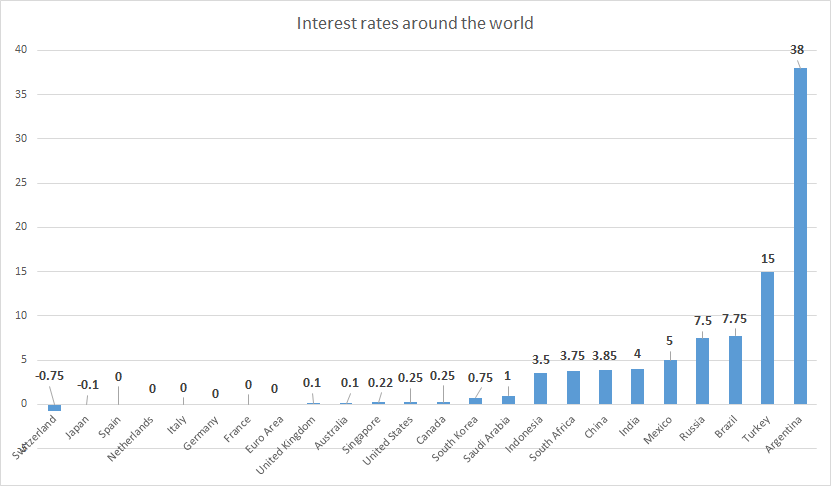

Interest rates around much of the developed world are at record lows

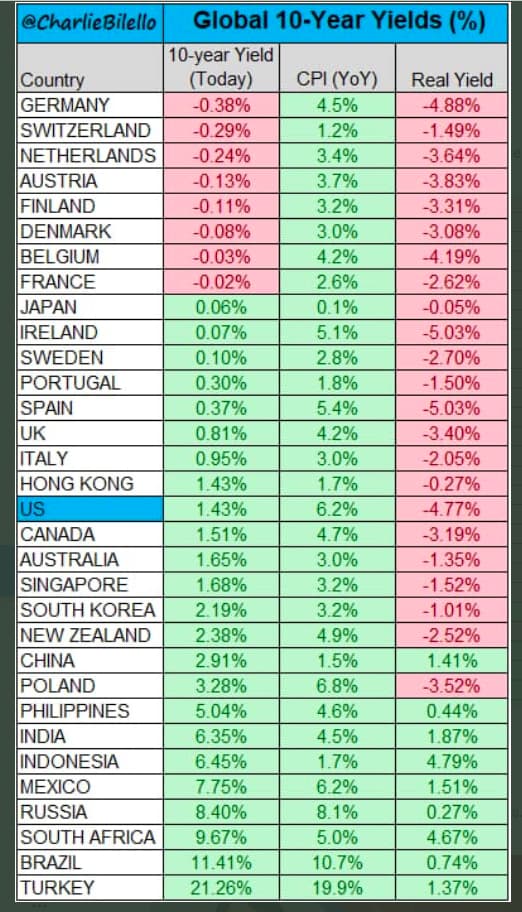

Naturally, Bonds are yielding close to zero:

Source: JP Morgan

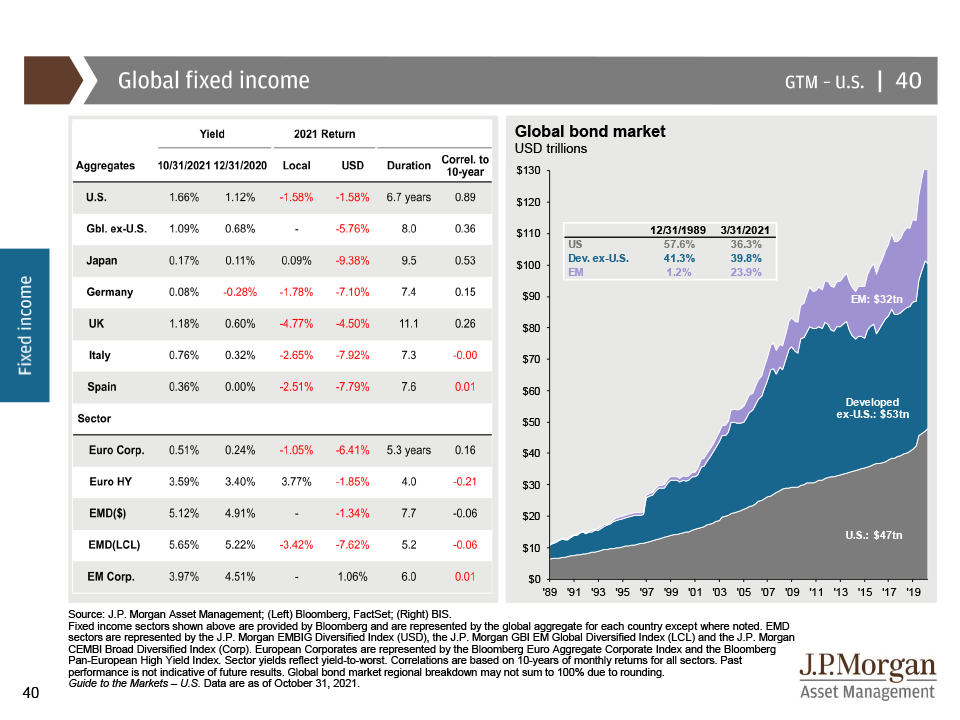

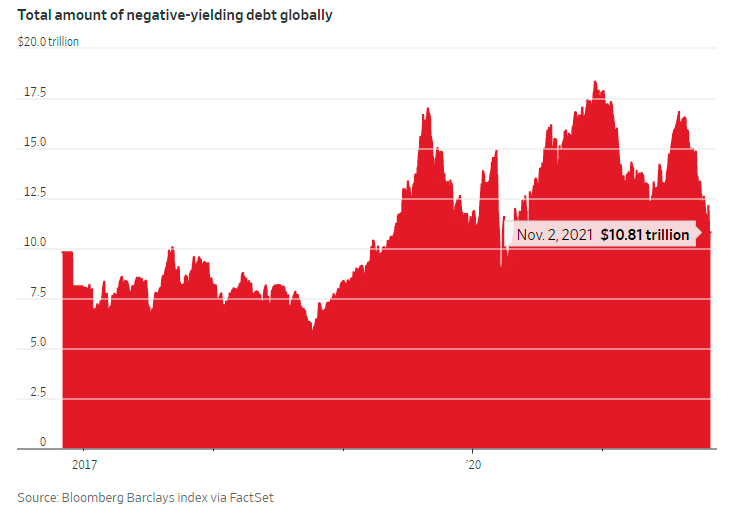

In fact, $10 trillion worth of bonds have negative yields. Meaning, you will get less money than you paid for at maturity-you are losing money to buy a bond. Let that sink in. Some companies have issued bonds at negative yield-basically free money.

Source: WSJ

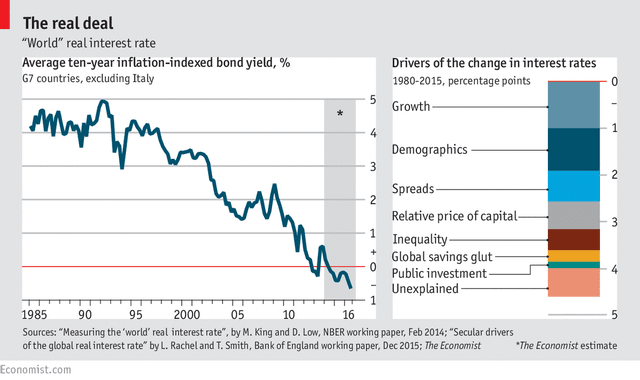

Like I wrote in the previous post, it’s hard to pin down one exact reason for the low-interest rates. At the broadest level, interest rates are an indicator of economic health. But then again, there are also structural reasons like demographics, low inflation, savings glut, and globalization, among other factors for low rates.

Source: Economist

Now to the important question: Do low-interest rates lead to investors taking excessive risk-taking or hunting for yield?

I’d like to start with one of my favourite quotes:

> “More money has been lost reaching for yield than at the point of a gun.” – Raymond DeVoe Jr

Intuitively, the logic goes something like this. People always want high returns. When interest rates are low, people don’t quickly adjust their return expectations downward. Instead, they look for other alternatives that offer a higher yield. If someone was getting a 7% return on FD when interest rates are at 6-7%, it would take time for him to adjust their expectations if interest rates fell to 3% and FD rates fell to 4-5%. This Let’se behavioural explanation.

So in order to continue earning the 7%, those investors might take on additional risk-hunt for yield. This could mean taking credit risk by investing in lower-rated bonds or credit funds. It could also mean making some equity allocations to juice up the returns.

This is the intuitive explanation, and it’s not wrong. But I wanted to write this to give you a better sense of how risk-taking flows through the financial systems.

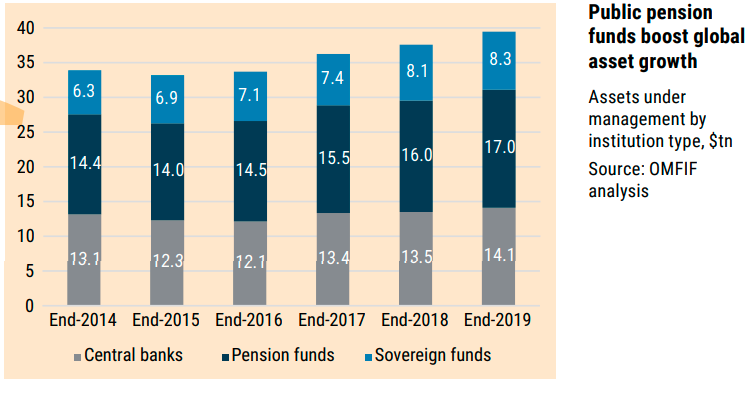

Let’s start with the biggest pools of money like pensions, insurance companies and other wealth funds. Combined, they manage trillions of dollars

Source: OMFIF

TheseHere’sies tend to have fixed returns targets and long-dated liabilities. The liabilities of a pension fund are when the pensioners who invested into the fund retire. you’dension fund has to start paying out money then. So pensions need to hit certain return targets to ensure that their funding ratios are meant otherwise, they will be in a shortfall.

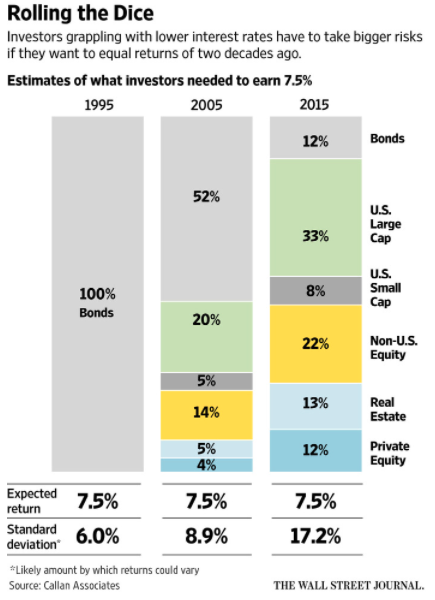

So how does this translate to excessive risk-taking? Here’s a stunning graphic from WSJ that shows the asset mix you’d have needed to hit a 7.5% return target. In the 90s, 100% of bonds would hdoesn’tten the job done. Today, pension funds need to take 3 times the risk measured by the standard deviation (SD) to achieve the same returns targets. Bonds went from 100% to 12%, while equities went from 0% to 63%.

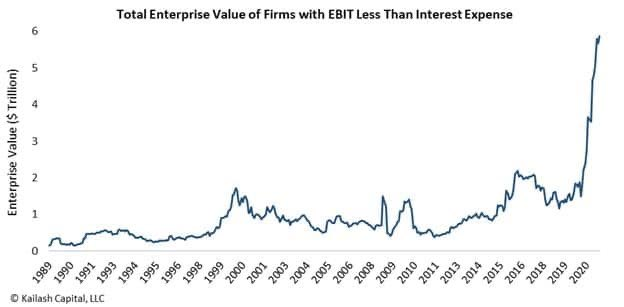

That’s how low-interest rates push certain actions to reach for yield pushing them into equities. In some they’llit doesn’t just stop at equities. These entities have consistently gone out on the risk curve into high yield credit, risk sovereign debt of lower rated countries, esoteric structured credit products, mortgage backed securities (hell0 2008) and a wide spectrum of high yielding credit products.

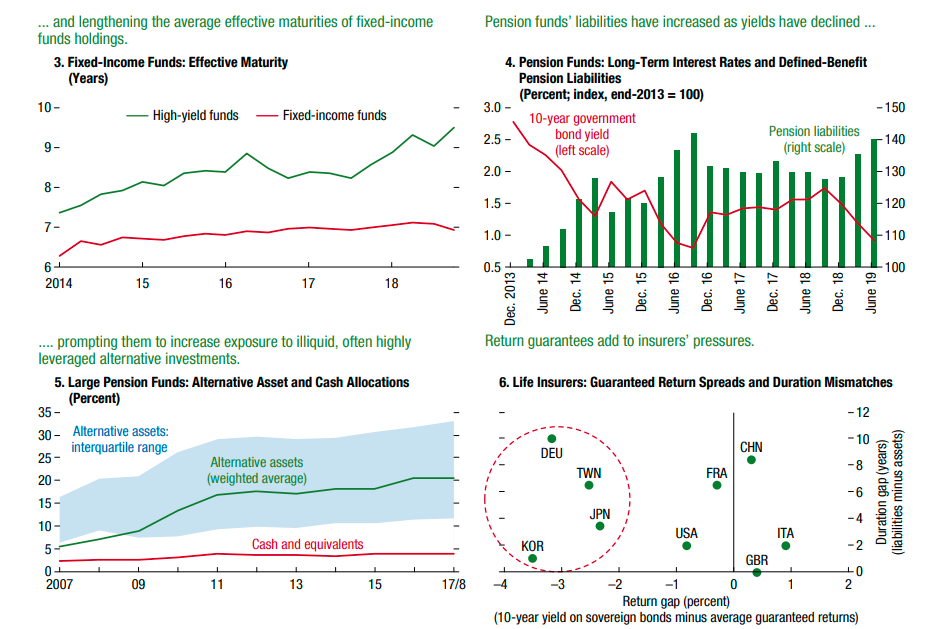

Perhaps the most dramatic change In the last decade has been the dramatic increase in allocations to alternative strtaegies such as venture capital (VC), private equity (PE), real estate, infrastructure, hedge funds and so on. The allocations have increased from the 5% range to more as the pension funding deficits have increased to trillions.

The result has been a sudden rush into alternatives to bridge the returns shortfall. 5-10% allocations might seem like tiny numbers, but given these size of pensions, those are 100s of billions of flows. This one reason for the dramatic increase in VC and PE funding across the world.

Source: IMF

The other development because of low rates has been the growing popularity of “call-overwriting” strategies among certain pensions and large pools of money.

Covered call overwriting strategies systematically sell short-dated call options on portfolio holdings. The seller of a call option earns the option premium which can add an income stream to their portfolio.

These strategies are being increasingly used to generate some extra income. Counterintutively, as more pensions rush into such strategies, the premiums that can be harvested tend to drop, which again pushes the further go out on the risk curve.

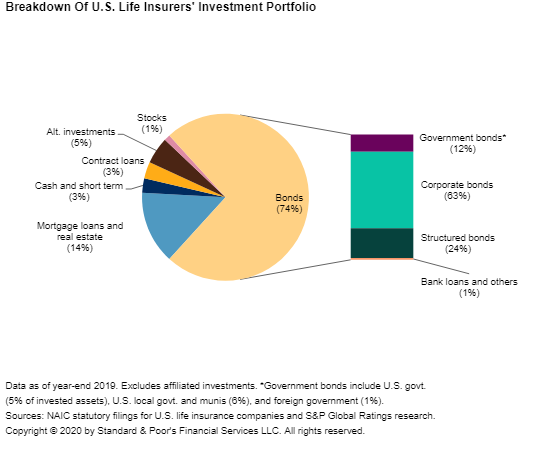

Insurance companies take money, promising to pay out when something happens. They also sell a lot of annuities and other products that tend to have fixed return payouts. Naturally, they’ll need instruments with steady and predictable returns to match the liabilities and bonds are perfect for this. It varies, but for illustrative purposes, this is how the portfolio of US insurers looks like

Source: S&P

In India, LIC manages over Rs 30 lakh crores, of which over 65% is in government bonds (G-Secs). Now at a simplistic level, if insurers sell X policies and products with returns guarantees etc, in a 7% interest environment, and if interest rates fall, they are in trouble. So they have to make up the return shortfall,

Just like we saw with pensions above, when rates drop, they have to make up the returns deficit. So, even they go out on the risk curve. This manifests in the form of higher allocation to high yield credit, increased allocations to emerging market govt and private debt, structured credit products, derivatives products like call/put writing programs and so on.

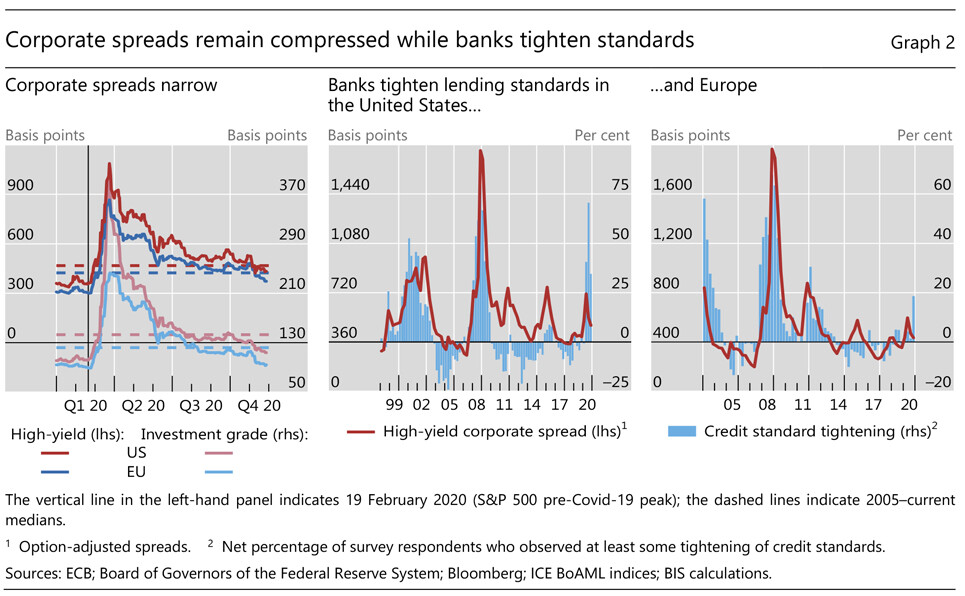

All these activities have reflexive feedback. So for example, if insurance companies increase allocation to risky high credit, the more the money flows, the sharper the compression in credit spreads. A spread is the difference in yield between a govt bond and other types of corporate debt. And we are seeing this happen across much of the developed world

A divergence in the assessments of corporate vulnerabilities may be emerging. Credit spreads in advanced economies saw some volatility but ultimately compressed further, approaching pre-pandemic lows. On the other hand, banks tightened lending standards throughout the review period. Investors’ search for yield and the specifics of policy support appeared to underpin these contrasting developments. - BIS

More feedback loops

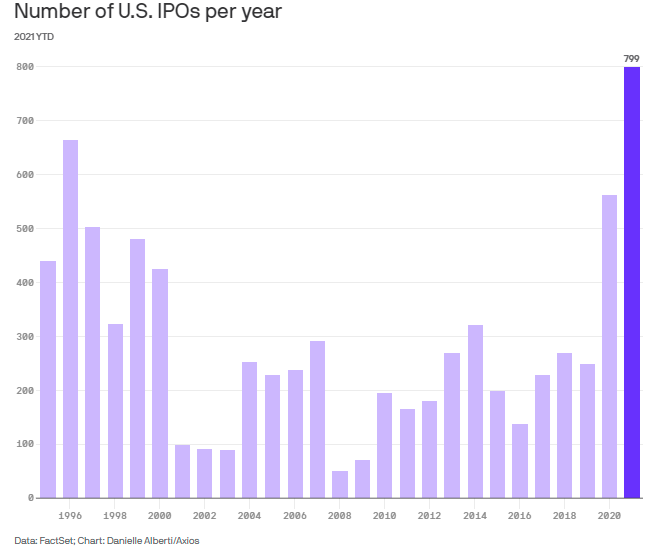

The otherside of the story is that, the number of IPOs and SPAC deals have hit a record high across US and India. VC investors are finally seeing liquidity from all the investments they made. Which means all this money now has to be put to work again-in other worse find yield.

Source: FT

Source: Axios

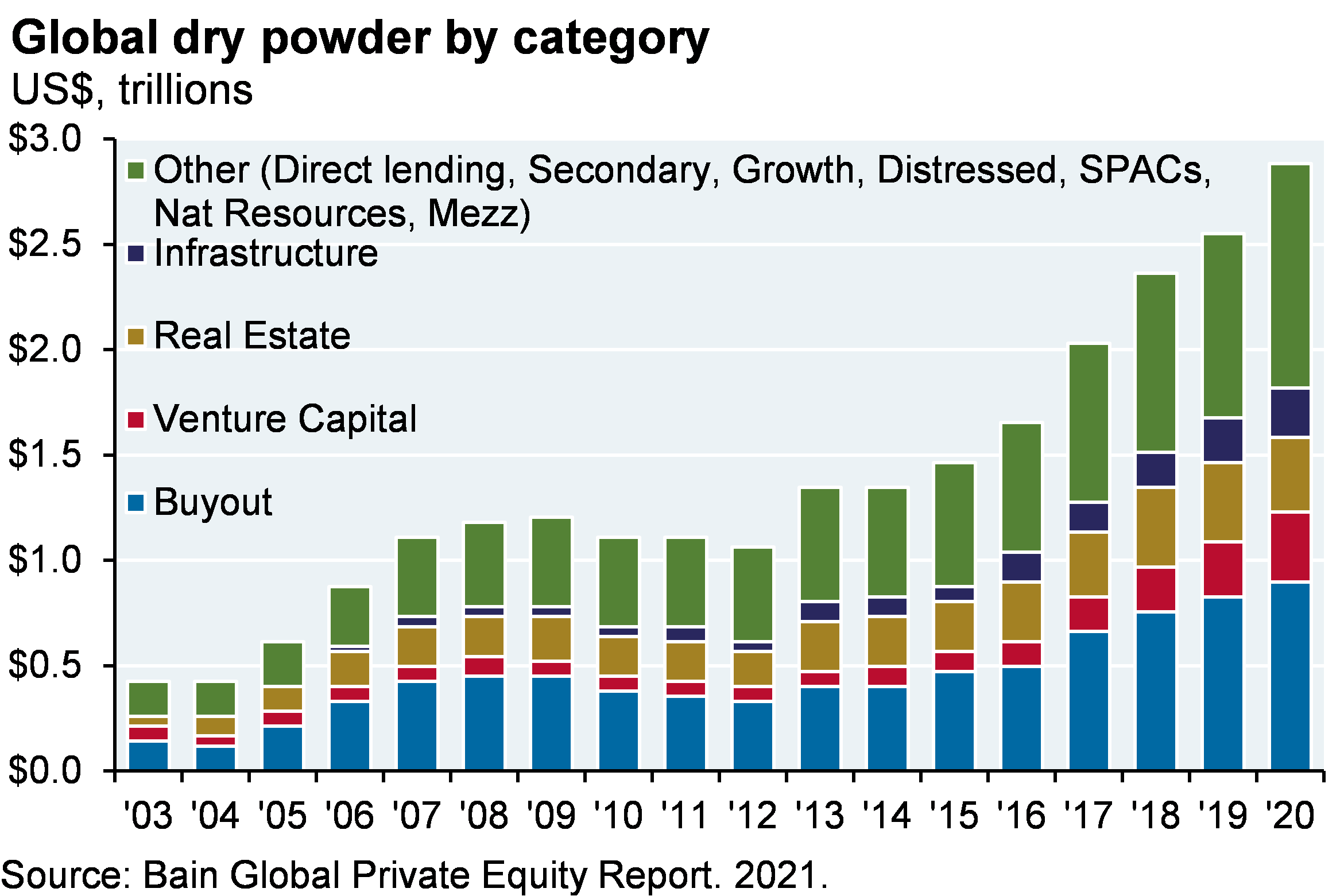

And the amount of idle capital waiting to be deployed is at a record high across the world.

Source: JP Morgan

So when people say this is a liquidity fuelled rally, this is one side of it.

Individuals

Chen Lian and Yueran Ma had a really interesting paper on the behavioral side of a low interest rate environment. Here’s an interesting snippet:

Indeed, many savers appear to have a deeply ingrained notion that saving is the preservation of wealth, and wealth should grow at a “decent” rate. Savers also have a tendency

to be influenced by the salience of investment returns, and perceive and evaluate returns

proportionally. Such mindset could lead to saver behavior that is at odds with predictions

of canonical models. As we show, savers may reach for yield and demonstrate a stronger

propensity of risky taking in their financial investments in a low interest environment. Saving targets savers (such as retirees) aim to achieve may also prompt them to cut back on

consumption in order to achieve their savings target (Powell, 2017; Gross, 2015).

There was another study by Yueran Ma, Wilte Zijlstr and they found that risk taking increasing substantially as rates drop

We find robust evidence that people in the low interest rate condition invest significantly more in the risky asset. This finding holds among several thousand participants from Amazon’s Mechanical Turk platform (representative of the general US population) as well as 400 Harvard Business School MBA students.1 The results also hold consistently across different settings (hypothetical questions and incentivised experiments). The average investment share in the risky asset increases by about 8 percentage points in all these cases, as shown in Figure 1.

We’re seeing this playout among individuals in multiple ways. Equity allocations have hit highs. A segment of retail investors increasingly moving toward risky products like credit funds, structured debt products etc. I’d argue that the rise of crypto, DeFi is also to an extent a symptom of low interest rates. For example, the yield on the US 10 year bond is 1.6%. But some crypto products that are considered relatively safe offer 2-3 times the yield.