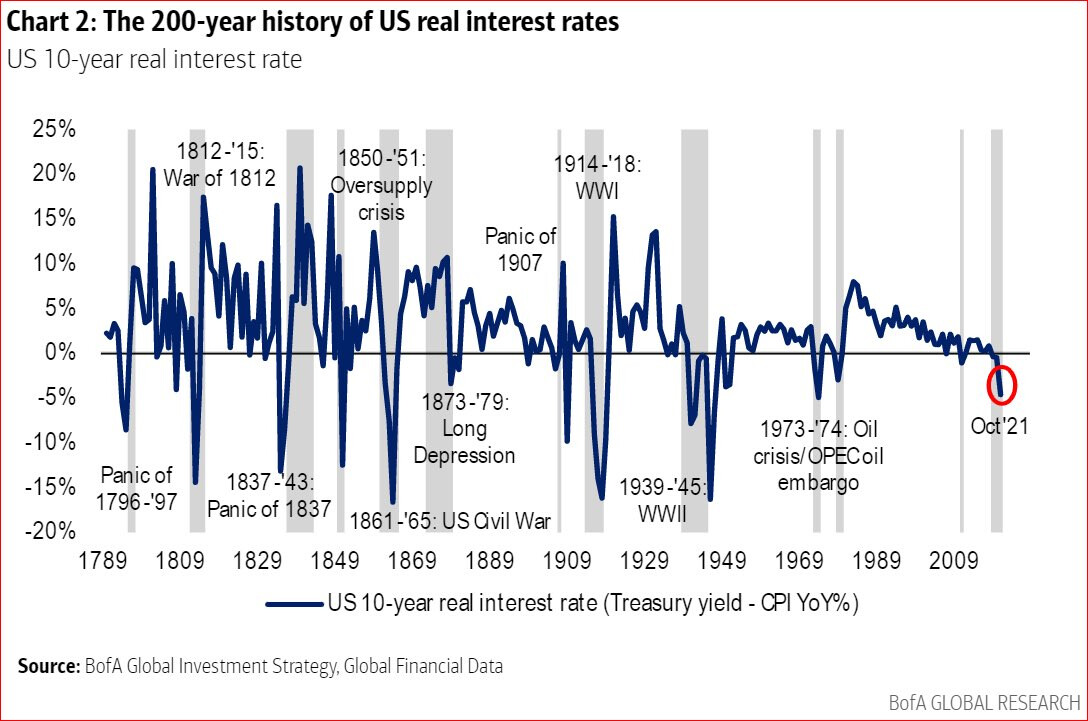

I came across this pretty interesting chart of historical US interest rates. Seemed like a good time to share given all the inflation worries around the world.

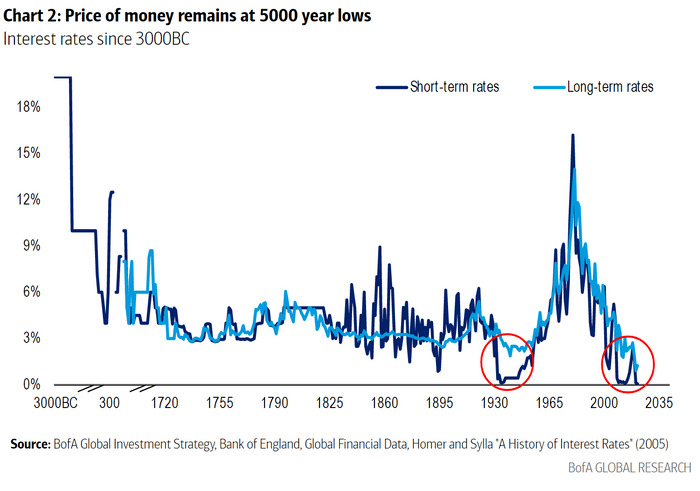

What’s even more dramatic is this chart that shows the interest rates over the last 5000 years, thanks to the work of Richard Sylla

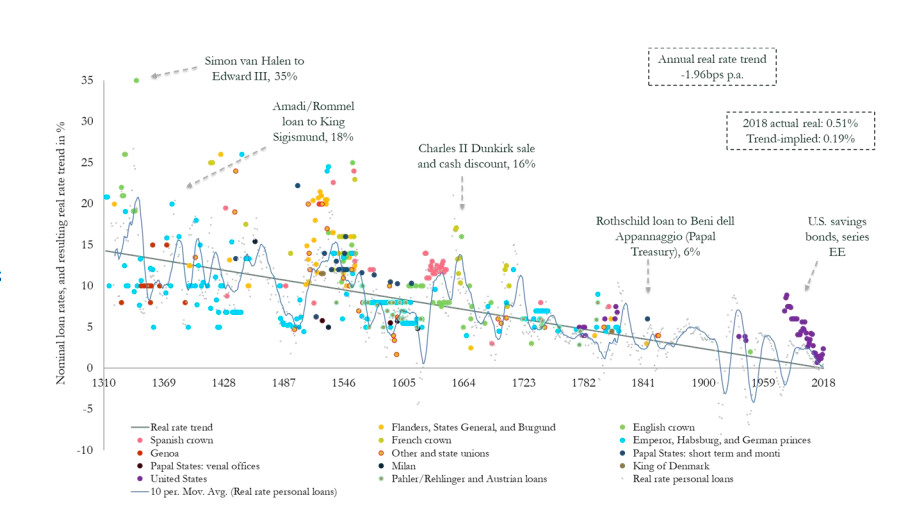

Not just Sylla, even Paul Schmelzing at Harvard has catalogued the same. Interest rates have been heading to the levels we see today over centuries:

As Harvard’s Paul Schmelzing wrote in a January paper, a longer-term look might be warranted. After cataloguing returns on safe assets for the previous 707 years, Schmelzing found, somewhat astonishingly, that “global real rates have shown a persistent downward trend over the past five centuries, declining within a corridor of between -0.9 and -1.75 basis points per annum.” Since the Black Death, in short, real interest rates or their equivalents have been plunging inexorably toward zero—a “suprasecular” stagnation. The causes of this slide, Schmelzing admits, must remain unclear, given the fragility of the archival dataset. - Berkley

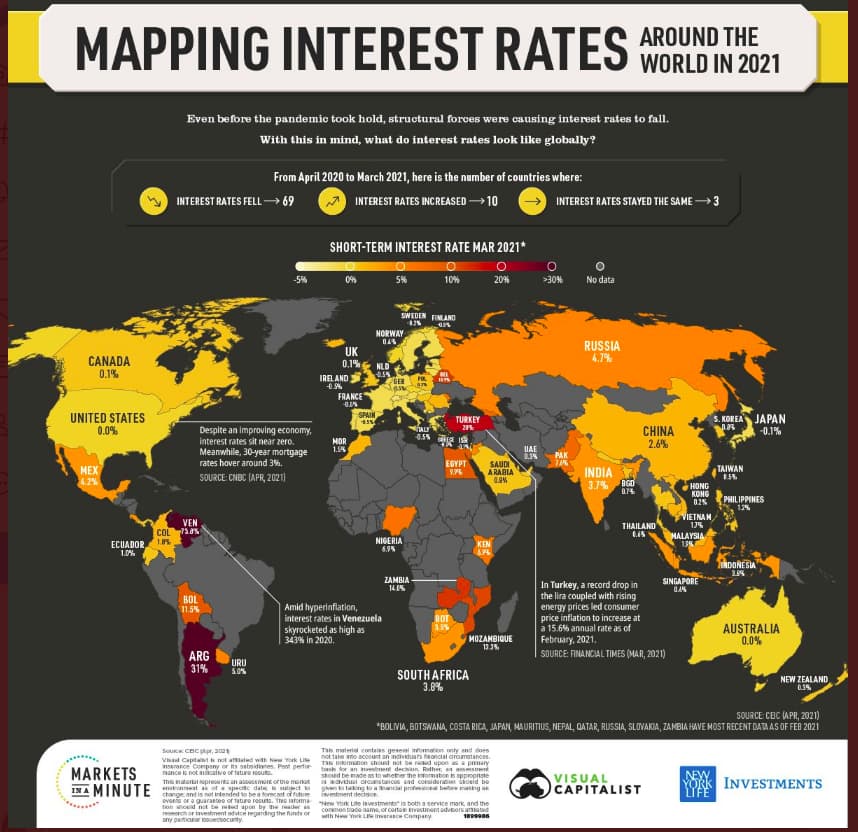

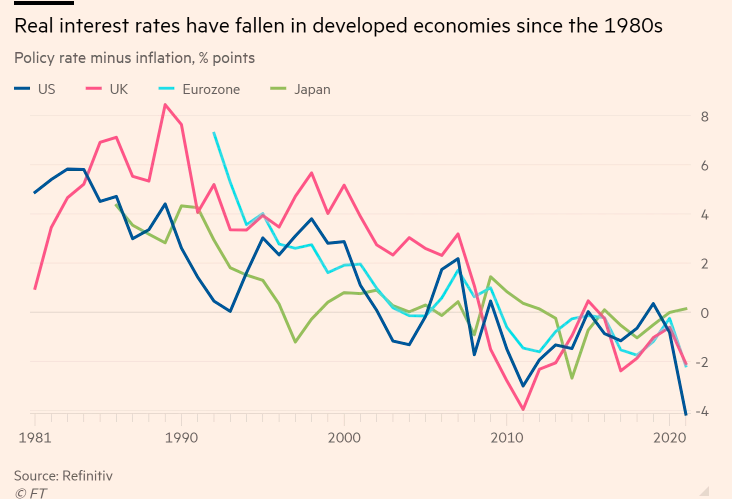

Interest rates across the developed world

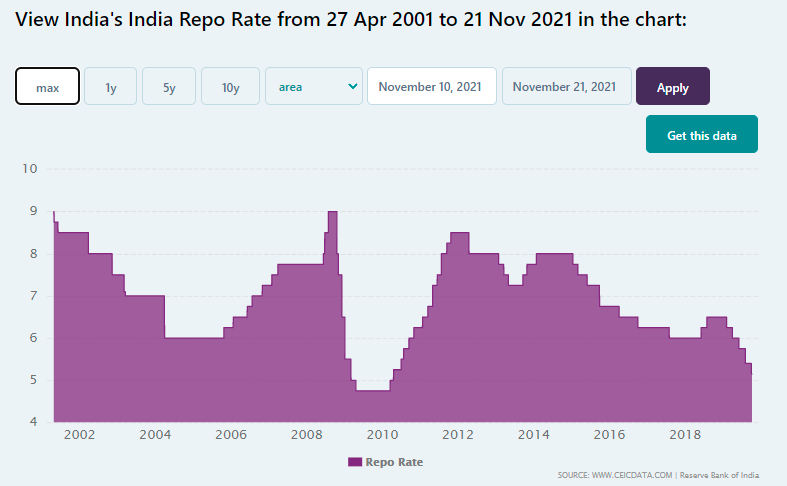

Here’s how Indian interest rates have moved. We don’t have a lot of history but there have been 3-4 cycles to get a sense.

A few thoughts

In the developed markets Interest rates have been falling for over 40 years. That’s a stunning bull market for bonds. Falling interest rates are good for bonds the price of the bonds goes up. As you can see from the chart above, the real rates (nominal interest rate-inflation) across developed countries is at almost zero or negative. That’s still hard for me to digest.

Why are the rates low?

I’m scared to even ask this question given how contentious it is. Like with all things economics, nobody bloody agrees on anything and there are 1000 theoris. But at the broadest level, interest rates show the health of the economy. As William Bernstein writes in The Birth of Plenty:

Interest rates, according to economic historian Richard Sylla, accurately reflect a society’s health. In effect, a plot of interest rates over time is a nation’s “fever curve.” In uncertain times rates rise because there is less sense of public security and trust. Over the broad sweep of history, all of the major ancient civilizations demonstrated a “U-shaped” pattern of interest rates. There were high rates early in their history, followed by slowly falling rates as the civilizations matured and stabilized. This led to low rates at the height of their development, and, finally, as the civilizations decayed, there was a return of rising rates. For example, the apex of the Roman Empire in the first and second centuries A.D. saw interest rates as low as 4%. The above sequence holds only on the average and over the long term, with plenty of shorter-term fluctuations. Even during the height of the Pax Romana in the first and second centuries, rates briefly spiked as high as 12% during times of crisis.

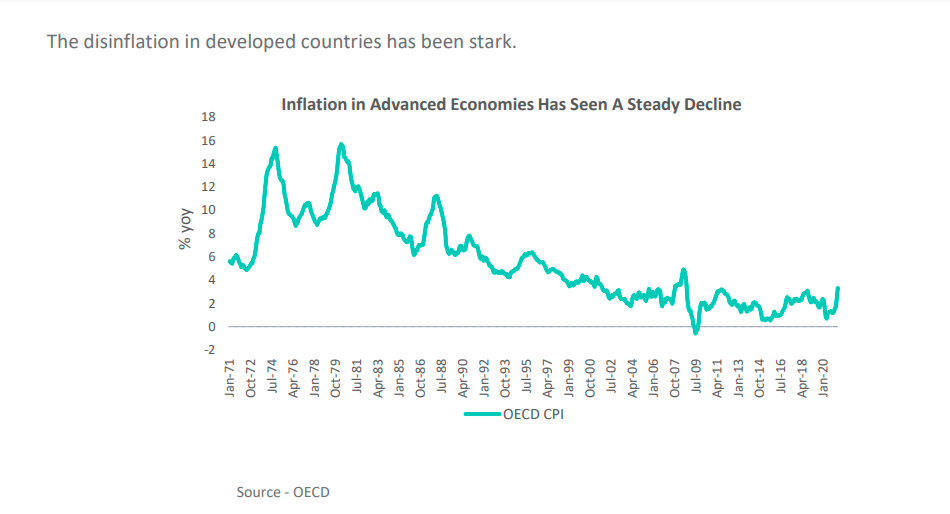

The other major reason is that inflation has been stubbornly low across much of the developed world if you subtract the recent spike in inflation.

Source: DSP

Why?

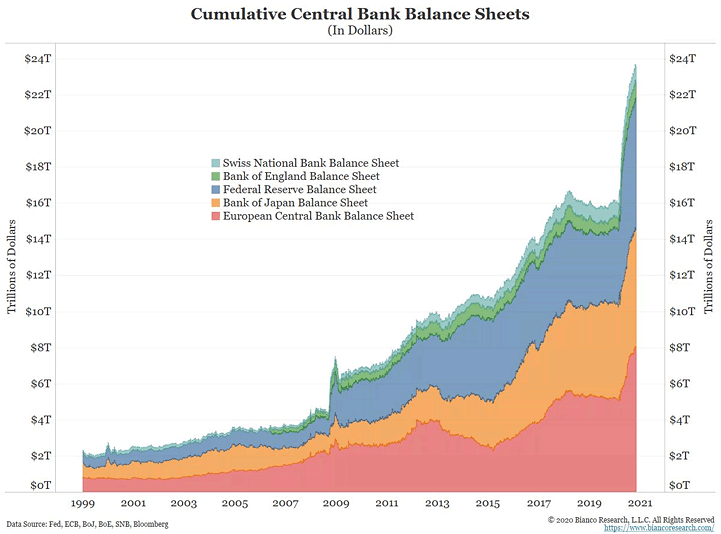

Again, this a contentious issue. But the triple threats of demographics, globalization, and technology explain a good chunk of the drop in inflation. Then there’s the big reason which people cite-aggressive intervention by central banks.

No single approach has been able to explain persuasively how inflation evolves. From a variety of potential determinants, the literature has broadly highlighted economic, institutional, technological, and political factors, which we group into eight economic theories: (1) natural resources, (2) demography, (3) globalisation and technology, (4) money, credit, and slack, (5) monetary policy strategies, (6) political and institutional setup, (7) public finances, (8) past inflation. - VoxEU

One other theory that increasingly comes up is the developed countries by offshoring manufacturing also exported their inflation to emerging economies like China, India, Vietnam, etc

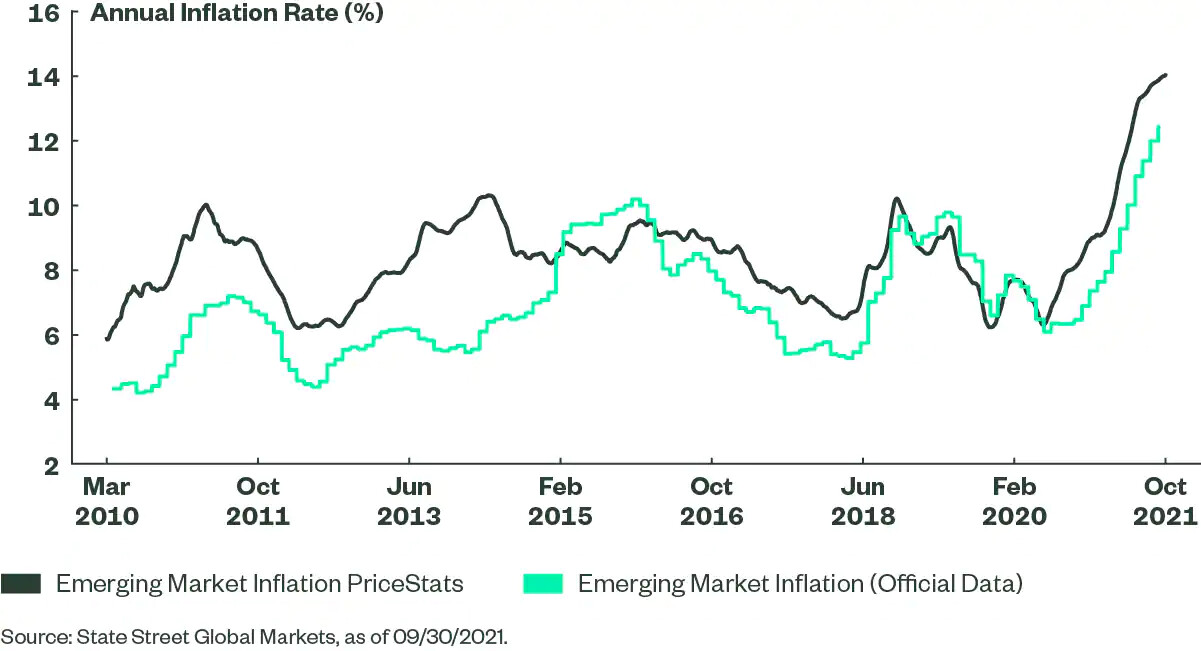

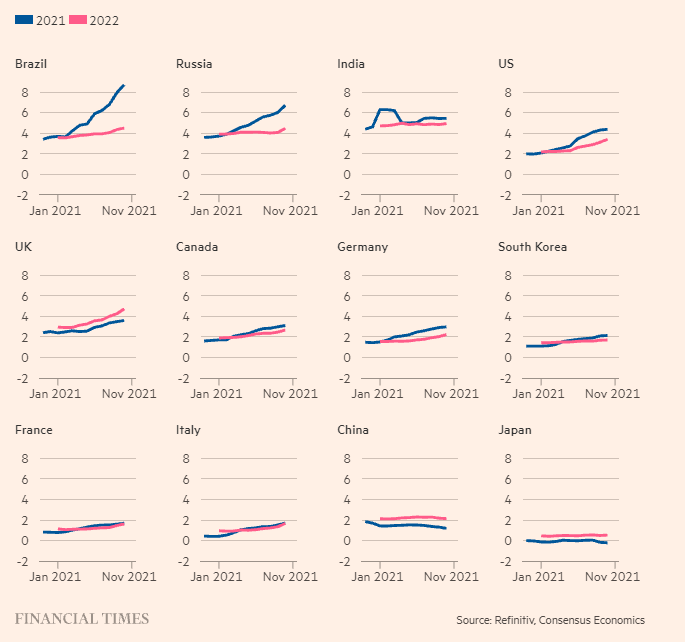

The recent inflation spike

Much of the word had a problem of low inflation since 2008. But inflation has shot up significantly in 2022

Some people argue that this is transitory. They argue that the inflationary spike is because of:

- All the fiscal spending my governemtns in response to the corona virus. And as governments taper of the spending inflation will fall back into previous ranges

- The recent spike in inflation is also due to all the supply chain issues across the world. These supply chain bottlenecs have translated into shortages of raw materials and higher shipping which has led to an inflationary spike

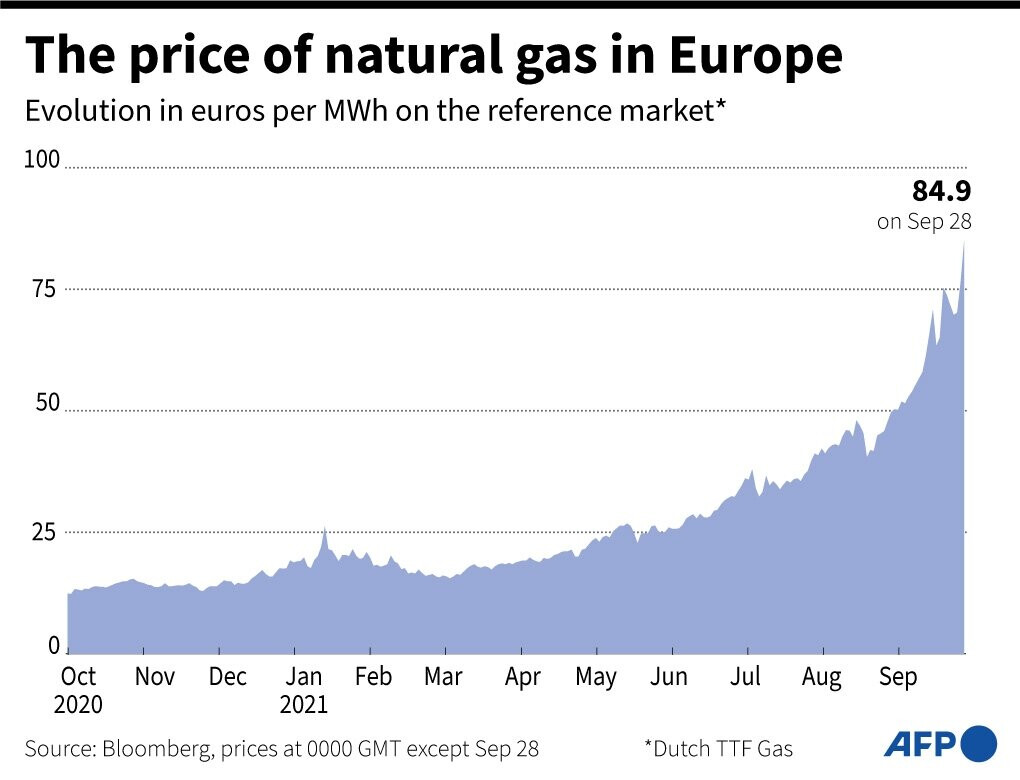

- A large part of the inflationary spike is driven by energy prices due to spike in crude prices and that inflation will reduce as crude prices moderate.

On the other hand you have the people who think that this inflationary spike is permanent because of:

- All the money printing by central banks for decades. All this money will find it’s way into the system and lead to higher asset prices as well as consumer prices

- There are long term structural changes such as the rise of ESG. This is leading to reduced capital for oil & gas companies, which mean lower oil exploration investments. Simultaneously, green energy sources like Wind and Solar aren’t reliable enough to offset coal, oil & natural gas. This is why natural gas prices recently shot up like crazy.

I personally think the reality will be somewhere between those extremes. But you have to remember, when RBI say inflation, it is talking about the rate of change. Meaning, let’s say inflation goes up to 10% and Unilever increases the price of Fair & Lovely by 5%. Let’s say inflation falls back to 5%, Unilever won’t reduce the price of Fair & Lovely by 5%. So the inflation for RBI might be temporary but permanent for consuments. There’s always nuance.