The NFO of Edelweiss Bharat Bond ETF open on July 14th and closes on July 17th. Bharat Bond is a debt ETF that will only hold bonds issued by public sector undertaking (PSUs). This ETF is that it is a defined maturity ETF, similar to a Fixed Maturity Plan. Before I explain more about Bharat Bond ETF (PSU debt ETF), you can check out this post if you want to learn more about how an ETF works.

How does a defined maturity ETF work?

A normal open-ended ETF doesn’t have a maturity date. For example, if you buy Liquidbees or a GIlt ETF, it will trade for as long as the ETF is listed. But the Bharat Bond ETF will have maturity dates. Edelweiss has initially launched 2 series of ETFs - 2023 ETF and 2030 ETF expiring in those respective years. This time the AMC is launching ETFs with maturities of 2025 and 2031. This is to allow you to get the benefits of indexation.

The AMC will keep launching new series. Each series will have an index and the ETF will just track that index.

What is the Bharat Bond ETF?

Bharat bond ETF is a debt exchange-traded fund (ETF) that will only hold bonds issued by PSU companies and other Government entities

What will the ETF hold?

The ETF will only hold bonds with AAA credit rating issued by the Government of India owned companies such as REC, PFC, NHAI, etc.

Will the ETF hold the same bonds till the maturity?

Not necessarily. The ETF will rebalance quarterly and if there are any changes to the index, the constituents will change. The ETF can only hold AAA-rated bonds, assuming that for example, REC is downgraded to AA, in that case, the index and the holding of the ETF will change.

How safe is the ETF?

Two of the biggest risks in bonds are default risk and interest rate risk. Default risk is nothing but the risk of a company not paying back its debt. Since the ETF will only hold bonds issued by PSUs, there is no default risk. PSU bonds carry an “implicit sovereign guarantee.” Meaning, the Govt doesn’t explicitly say that it guarantees the debt but it is understood that if something goes wrong the Govt will step in.

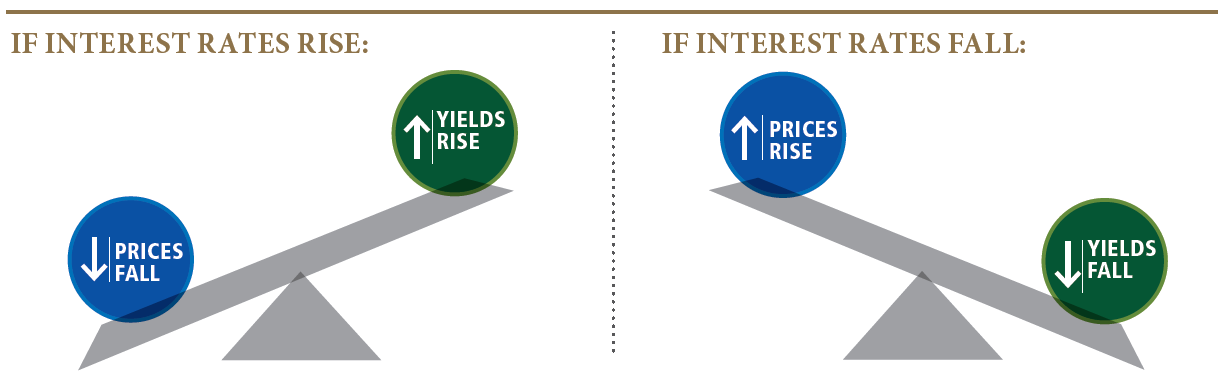

Interest risk remains. But if aren’t aware of what interest rate means

Pimco

This image should help you understand. We had also done a series of webinars on the basics of fixed income, you can check them out:

As interest rates rise and fall, the yields of the underlying bonds will rise and fall and by extension the price of the ETF. However, if you are holding the ETF until maturity, the risk will be negated.

How will the interest payments be paid?

The coupons in the ETF will be reinvested. And once the ETF matures, the entire proceeds will be paid out to you.

What will be the expense ratio of the ETF?

0.0005% for ETF and 0.05% for the fund of fund.

Can I sell the ETF before maturity?

Yes, you can, just like any other ETF on either NSE or BSE. But a general word of caution, there might some liquidity risk in ETFs given that ETFs aren’t really all that popular in India. By liquidity risk I mean, the difference between bids and offers. You can avoid this by placing limit orders.

What returns can I expect?

The Bharat Bond website shows the indicative yields of the ETFs. For the new ETFs being issued the yields are

2025: 5.46%

2031: 6.54%

What will be the taxation on this ETF?

If sold within 3 years, it will be considered as short term and STCG as per your income slab will be applicable. If sold after 3 years it will be considered as long term and LTCG of 20% with indexation is applicable.

When is the issue opening and how can I buy Bharat Bond ETF?

The NFO opens on July 14th and closes on July 17th. You can invest in Bharat Bond ETF here.

Constituents of the ETF.

Bharat Bond ETF 2025

| Issuer | Credit Rating | No. of ISINs | Outsatnding | Weight |

|---|---|---|---|---|

| POWER FINANCE CORP.LTD | AAA | 17 | 27409.2 | 15% |

| REC LIMITED | AAA | 10 | 19254 | 15% |

| POWER GRID CORP.OF INDIA LTD. | AAA | 16 | 10055.36 | 15% |

| NATIONAL HOUSING BANK | AAA | 2 | 3670 | 10% |

| INDIAN OIL CORP.LTD. | AAA | 1 | 2995 | 9% |

| NATIONAL BANK FOR AGRICULTURE & RURAL DEVELOPMENT | AAA | 1 | 2800 | 8% |

| HINDUSTAN PETROLEUM CORP.LTD. | AAA | 2 | 2500 | 7% |

| EXPORT-IMPORT BANK OF INDIA | AAA | 5 | 1765 | 5% |

| EXPORT-IMPORT BANK OF INDIA | AAA | 4 | 1707 | 5% |

| NTPC LTD | AAA | 14 | 1267 | 4% |

| NHPC LTD. | AAA | 10 | 2092.8 | 6% |

| NUCLEAR POWER CORP.OF INDIA LTD. | AAA | 1 | 400 | 1% |

| 83 | 75915.36 | 100% |

Bharat Bond ETF 2031

| Issuer | Credit Rating | No. of ISINs | Outsatnding | Weight |

|---|---|---|---|---|

| POWER FINANCE CORP.LTD | AAA | 6 | 13783 | 15% |

| REC LIMITED | AAA | 2 | 5309 | 15% |

| POWER GRID CORP.OF INDIA LTD. | AAA | 5 | 1893 | 15% |

| NATIONAL HIGHWAYS AUTHORITY OF INDIA | AAA | 1 | 1824 | 15% |

| NUCLEAR POWER CORP.OF INDIA LTD. | AAA | 3 | 1600 | 15% |

| INDIAN RAILWAY FINANCE CORP.LTD. | AAA | 1 | 1410 | 13% |

| HOUSING & URBAN DEVELOPMENT CORP. Ltd | AAA | 1 | 1040 | 10% |

| NHPC LTD. | AAA | 2 | 272.91 | 2% |

| 21 | 27131.91 | 100% |

The ETF maturing in the year 2025 will track the Nifty BHARAT Bond 2031 Index. You can check out the index constituents here for 2025 and 2031

Here’s a conversation with Dhawal Dalal, CIO of Fixed Income, Edelweiss Mutual Fund. In this conversation, we talk about the Bharat Bond ETF, Indian debt markets, the role of debt in a portfolio and a whole lot more.