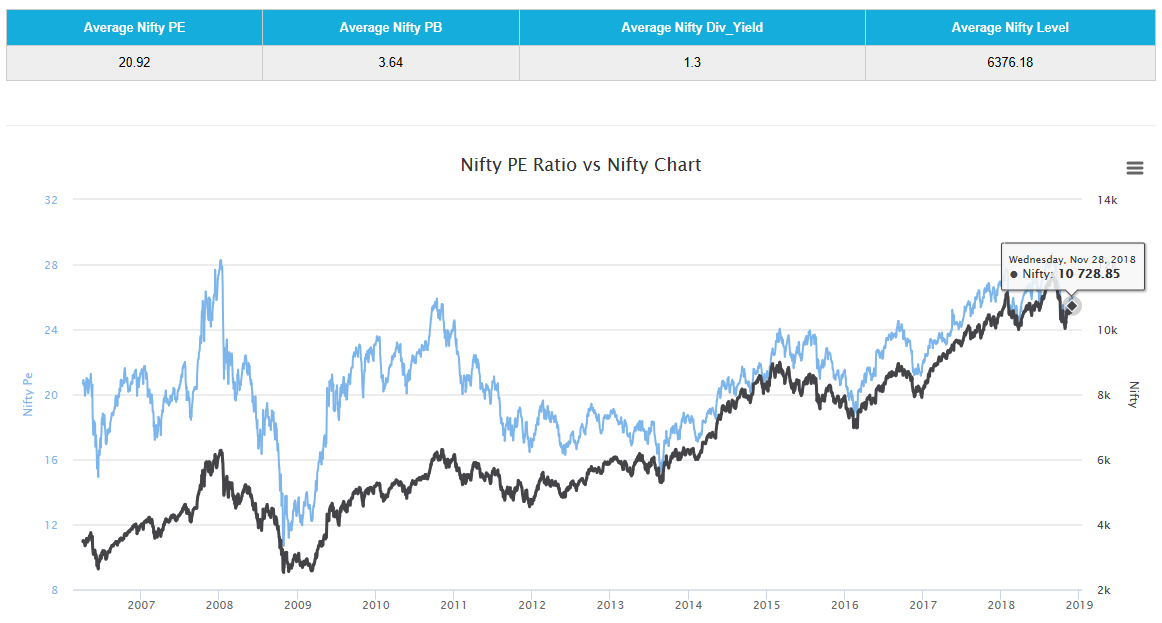

If you an average investor about his return expectation for the next say 10 year, you’d most often than not hear numbers ranging from 12-18%. Is it reasonable? I don’t have a crystal ball but we do know that that Indian markets are defiantly not cheap. The Nifty PE is at about 25. But this can be a bit misleading because the data in this chart is based on NSE site and it reports only the standalone PE and not the consolidated one. The consolidated number is around 20 and this also not cheap by any measure.

What do we know, since inception (1996) the Nifty 50 has given an annualized return of 10.7%, Nifty Midcap 100 has annualized 19.7% and Nifty Smallcap 100 has annualized 12.9%. Are the returns likely to be in the same ballpark going ahead? My bet would be no, given that the Nifty 50 is pricy while the Mid and Smallcap a little less so given the recent corrections.

Now, assuming that we were to enter a low return environment, which I am not predicting by the way. What should you do to maximize your returns with the same risk? Here’s a rather though provoking study by ReSolve Asset Management, a Canadian asset manager.

Here are some highlights:

Looking back over the past decade, investors can be forgiven for thinking investing is an easy game. After all, you just had to buy the S&P 500 near the bottom of a bear market and ride the rebound to earn double-digit returns. But this hindsight bias engenders a dangerous illusion.

In fact, most investors were too terrified to buy stocks in 2008 and 2009 as it seemed like the financial world was collapsing. And there have been many other terrifying hurdles over the past ten years that kept many investors on the sidelines.

Moreover, the strong performance of the S&P 500 obscures an important reality: U.S. stocks have been the only game in town. While U.S.-oriented investors were living large on the performance of FAANG s, international stocks and most currencies left non-US investors with low single-digit returns.

The fact is, investing is hard. Even worse, the next decade is likely to be harder than most. This will require advisors to diversify into alternative strategies so that client portfolios don’t fall behind on their goals.

Those who heed the lessons of past market cycles and the well-established principle of true diversification may have an unprecedented opportunity. Those who choose comfort and traditional portfolio construction methods may not be so lucky.

We know that a bond’s current yield is the best estimate of its total return . Currently, the iShares Core U.S. Aggregate Bond ETF (AGG) is yielding 3.3% and global bond indices are at even lower yields.

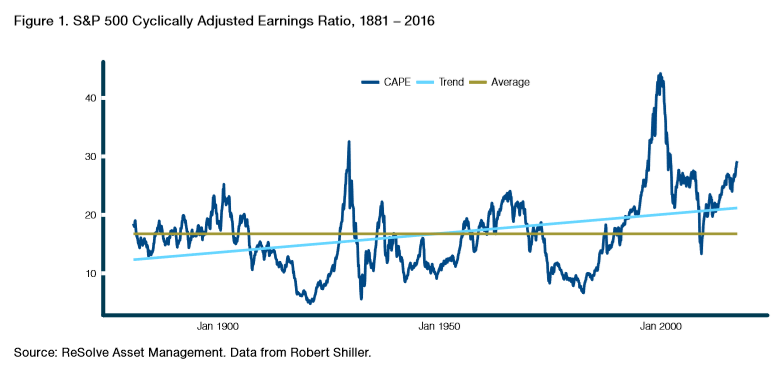

On the equity side of things, stocks should be expected to produce below average returns when they are priced above their average long-term valuations.

Currently, and even after accounting for an upward drift in valuation multiples over time , U.S. stocks remain well above their average, long-term valuations.

Together, these two factors signal a major headwind for traditional portfolios over the next ten to fifteen years.

In fact, after adjusting for inflation and fees, we estimate that investors will be hard-pressed to earn more than 2.5% per year on traditional portfolios of domestically focused stocks and bonds over the next decade.

A solid first step might be for investors to consider emphasizing global asset classes and less common markets like inflation protected bonds, and potentially commodities.

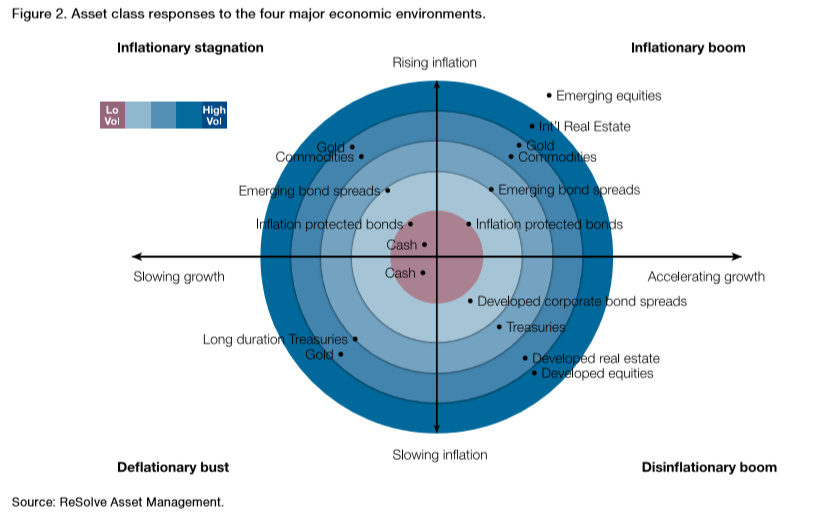

Diversification across these global asset classes is important because they are expected to respond in a very predictable manner to changes in growth and inflation. As you can see from the chart below U.S. stocks and bonds only thrive in ONE of the four potential economic regimes.

U.S. stocks and bonds respond most favourably to the ‘Disinflationary Boom’ period located in the bottom right corner. This is in stark contrast to the asset classes that do well in the exact opposite “Inflationary Stagnation” regime where TIPS, gold and commodities thrive while US equities and bonds tend to do very poorly.

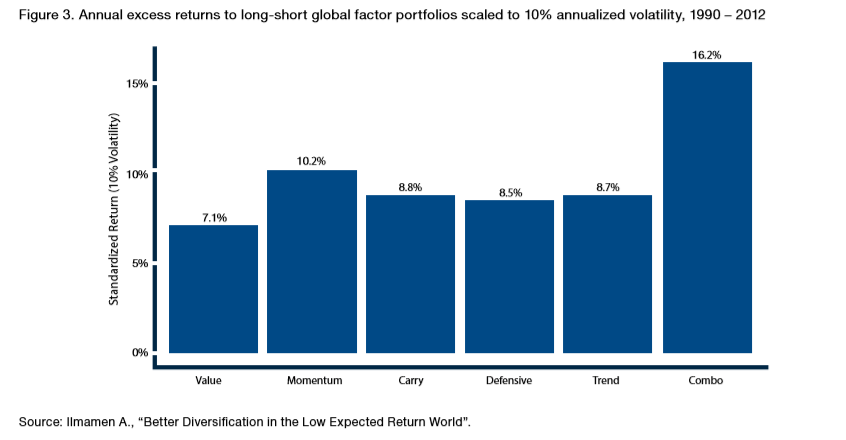

If investors misbehave in relatively predictable ways – by herding, over/underreacting to new information, anchoring, etc. - then there is an opportunity for other investors to earn excess profits by investing in a manner that arbitrages this behaviour.

Most alternative investment strategies tend to harvest one or more of these forms of misbehaviour. We’ve highlighted a few such approaches in Figure 3. As you can see, the excess profits earned from these alternative approaches can be quite lucrative. Better yet, they are uncorrelated with one another, and can serve as extraordinary diversifiers for traditional asset classes.

Setting realistic expectations, diversifying as much as possible, and taking advantage of unique alternative strategies – can help investors navigate a future that may be radically different from the recent past.