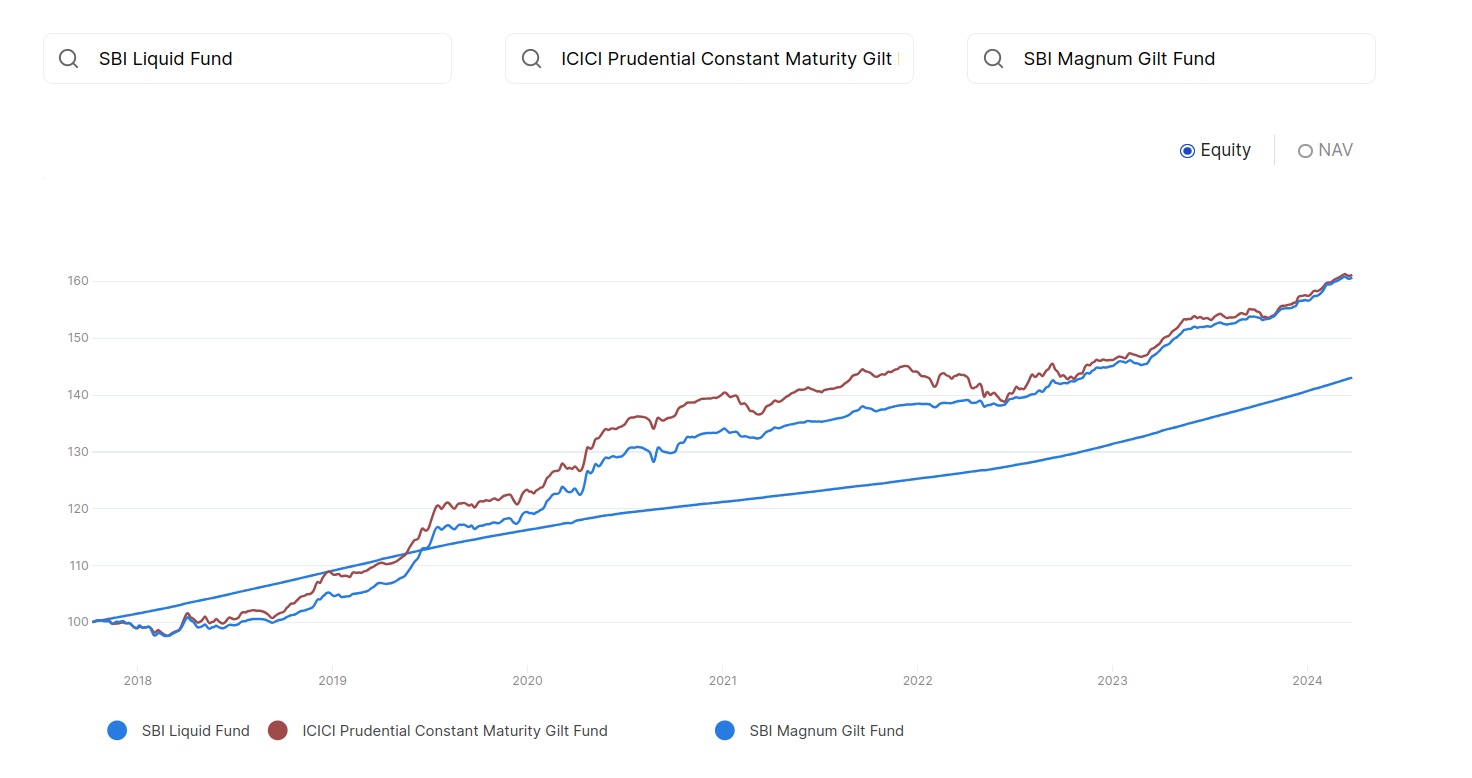

Currently I have invested in Liquid Mutual Funds (Growth) and I’m considering switching to GILT funds for higher returns (>9%).

Does it make sense to buy GILT funds now by selling liquid mutual funds?

Currently I have invested in Liquid Mutual Funds (Growth) and I’m considering switching to GILT funds for higher returns (>9%).

Does it make sense to buy GILT funds now by selling liquid mutual funds?

Comparing liquid funds with Gilt funds is not right. Liquid funds are short term debt funds and their returns will be more or less FD+. Gilt funds, on the other hand, are long duration debt funds with a higher duration or interest rate risk. Meaning, they are more sensitive to interest rate changes and are more volatile compared to liquid funds. When interest rates go up, they fall more than liquid funds, and when rates fall, they gain more than debt funds.

So, your decision should be based on that. Also, 9%+ isn’t guaranteed ![]() It depends on interest rates.

It depends on interest rates.

TLDR:

If I hold the GILT funds for long duration say 10 years, I can nullify the interest rate risk, right?

For example, I buy SBI Magnum GILT fund now at current NAV of 63 for 1 lakh rupees. Am I not locking in the current 10 year yield of 7%? I understand there will be NAV fluctuations in the short term, but after 10 years, isn’t it guaranteed to generate 7% CAGR? At this rate after 10 years, the NAV will be close to 124. Is this not guaranteed?

No it is not guaranteed.

You holding it for 10 years is of no real significance, because fund manager can keep on buying and selling its holding intermittently, and if fund amanager’s call goes wrong, returns can change .

While there is very high chance that 10+ years of holding will give you return close to 7, it is not guaranteed.

GILT funds invest in government securities with no credit risk but are sensitive to interest rate changes, making them more volatile. They are ideal for long-term investors seeking safety.

Liquid mutual funds invest in short-term debt instruments, offering higher liquidity and lower volatility, making them suitable for short-term goals.

Choose GILT funds for safety and potential higher long-term returns, and liquid funds for stability and immediate liquidity.

I think one can buy Gilt funds when interest rates are high and sell when the interest rates have bottomed out and there is a buzz in the market of high inflation causing the interest rates to rise. We have been in a high interest cycle for approx. last 2 years due to inflation and in case it remains stable, there are chances that we might undergo interest rate reduction cycle.

I am not an expert, and a hypothesis based on the prices of bond having inverse relation to the interest rate. Experts may comment on this.

I may be wrong about this, but in general if I can directly invest in the bonds or G-SEC, then the coupon interest rate paid by the government, will become my annual return or yield (Eg 7%) as the initial investment will be redeemed on maturity, assuming it is held till maturity or the duration of the bond.

So my returns are fixed and guaranteed, only if i don’t sell when the interest rates rise and hold till maturity.

But when it comes to investing through Gilt mutual funds, i think they invest in many G-secs having different maturity and varying coupon rates, thereby averaging out the yield, creating uncertainty over any guaranteed returns, and not to forget that they carry some expense ratio too.

And when more ppl invest in this fund, they fund is bound to buy these bonds at the prevailing prices which can be at a premium due to the increased demand, and this can impact the yield it generates. (i could be absolutely wrong here)

In conclusion, i believe the only way to guarantee the yield is to invest directly in the bonds and hold em till maturity.

DOUBT:

I have the following doubt, and would love others thoughts on it

Agreed, the bond’s price and it’s yield have an inverse relationship, but this theory holds good only if someone is buying the bonds at a premium, when the interest rate falls, as their yield would be eaten away by the premium paid to acquire it.

My doubt is, for someone who is already holding the bond, which is paying a fixed high coupon rate, doesn’t the fall in the interest rate, provide an opportunity to increase the yield by selling it at a premium.

As in this situation, the yield actually increases when the bond price increases for the holder, is it not ? Or am I making a conceptual mistake here ?

@SG_13 When interest comes down, bond prices shoots up, and if you are already owning a bond, you can sale at premium too. But that means you are trying to time the market. There is no guarantee that interest rate will be increased and bond prices will become lower. It’s all about risk just like stocks.

Note: Yield decreases whenever bond price rices because of fixed coupon rate

Oh, you mean to say that once i sell my bonds at a premium during a period where the interest rates have fallen, i wont be able to find another bond to invest in with that money, as all the bonds will be trading at a premium.

For someone who is happy with the fixed rate coupon that the bond pays, they might not want to sell just because they can sell at a premium, but if someone was looking to cash out, the best period would be during the interest rate fall.

I mean, theoretically, interest rates are low when the inflation is low, I would be okay with not investing back in the bonds during a low inflation and low interest rate period, as i can look for other investment options with that money, as the economy grows faster during the low inflation period.

Anyways, i could be completely wrong.

Just trying to learn and express my thoughts.

Switching from Liquid Mutual Funds to GILT Funds in pursuit of higher returns could make sense, but it involves a thorough understanding of both the market conditions and investment horiazon.

If you are looking to invest for a shorter horiazon, like less than a year then keeping investments in Liquid funds make sence. For long term, the GILT funds make sence because they has the higher yields than Liquid Funds in the lont term horiazon.

Insightful

How liquid is Gilt fund?

even if I want to invest for the short term, why gilt is not a better choice? due to interest rate cut/increase by Govt?

Can you explain a little bit more about premiums due to increased demand? I want to buy sbi magnum Gilt fund…is it at a premium right now? Ideally, one security should be bond price interest due …above it is premium …

i already buy one month back this fund - for next 3 years its will give good return , because of intrest rate cut - in SBI magnum - fund manger rotate the asset depend upon the intrest rate - so nothing need to worry for next 3 years

yes…I am also expecting a rate cut…but I want to park it for avg. 6 months. And, I am curious how much premium is this trading? and how does this get tax Slab or capital gain?

6 month its not enough to be get in gilt fund = because only one cut can be expected - wait for atleast one year for good return

Do we get interest in our account from Gilt Fund or it’s adjusted in NAV?