1.As has already been discussed on multiple occasions by @nithin, every broker is now a discount broker and it all boils down to who has the best product.There was apprehension of a threat to zerodha even when Paytm money got into stocks but that has not happened. My experience with Zerodha has been really good and the reason I stick to Zerodha is the quality of management and their resolve of doing the right thing.

-

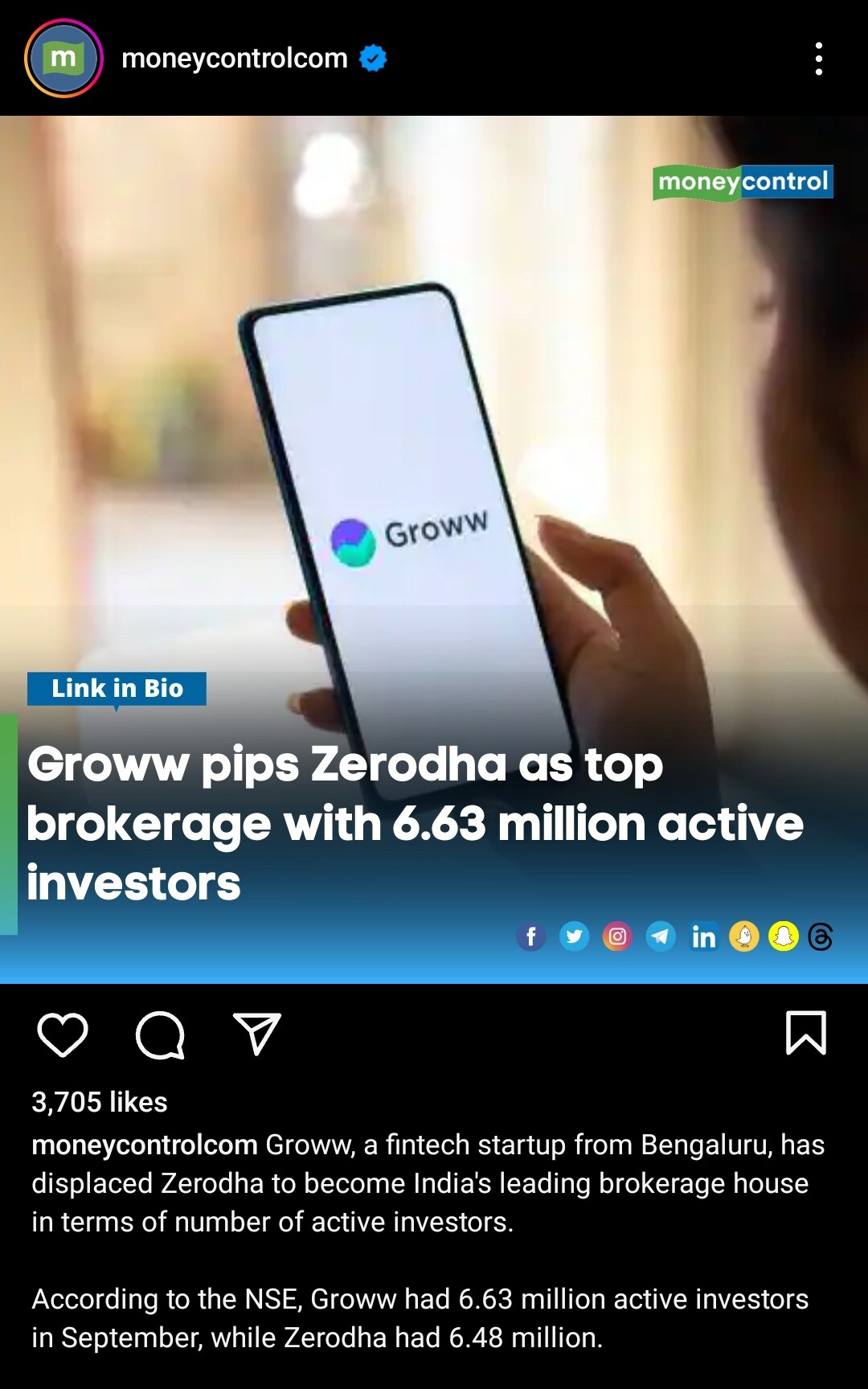

On an earlier thread I discussed with Nithin why Zerodha does not advertise and his explanation has been on point. I believe the recent spurt in Groww accounts is a result of their strong marketing campaign. I do think that Zerodha should start running ads at this point.

-

The simplicity of the zerodha ui and the education initiatives and the open discussions here win my heart and is a major reason of my loyalty to zerodha,

4.Having stated the above,. I do believe that there is room for change and the zerodha ecosystem seems too minimalistic in comparison to competition now and what we need now is a kind of finance superapp as opposed to one platform for trading, one for mutual funds etc. Also kite can be refined to add logos to stock tickers as this instills a sense of familiarity.

- I want zerodha to be a pioneer and shall always root for its success.

@nithin your thoughts would be really appreciated.

Thanks a lot,

Manan.

I had kind of addressed this point in the recent business updates post

Businesses can be built in different ways and for different types of audiences. Groww has done a phenomenal job building for a certain type of audience and we have maybe done a decent job for another type of audience. The market is large enough for multiple types of players to exist.

I guess running a business is like playing a sport, we have to play to our strengths. ![]()

Not comparing Groww to Apple (obviously) but the resistance to smartphone evolution and the android ecosystem kind of rhymes here. I guess the ‘indestructible’ Nokia too played to its strengths without attending to what the market was asking for. Just a food for thought as I think the biggest single contributor to business (and personal) success is luck (and what do I know about running businesses).

The core of every business is the product, and that has to evolve. Eventually, the better product wins, there is no doubt about this. Our focus has been to continuously evolve the product, our offerings, and various initiatives, either directly or by partnerships through Rainmatter.

But the point made here was around advertising and marketing. Should we start spending money on acquiring customers and then be forced to compromise on the philosophies that have helped us get here? I am not sure. I think the way products can help differentiate, not being forced to sell to a customer constantly, can also help differentiate. At least, that is how we think. Only time will tell if that is right or not. ![]()

From the post.

There is an actual cost (KYC, documentation, eSign, human verification, etc.) that is incurred while opening an account. If there was no account opening fee to recover the cost, the business could implicitly be pressured to get a customer to transact to recover that cost. This isn’t good for the customer or the business in the long run if a customer transacts due to a push from the broker, which causes the customer to lose money. Any attempt to explicitly recover this cost could also mean compromising on the many core principles at Zerodha, like the no-spam policy, no revenue targets for the team, and more. This is also why we don’t spend on advertising.

Sir, you must be sleeping well at night without all that garbage marketing and loan selling. Please continue to do so.

@abcd5662 Can you elaborate a bit more?

What similarities do you see with the smartphone revolution and new brokerages like Groww?

What are any features that Groww is providing/supporting that other incumbent brokerages are not? ![]()

If nothing comes to mind, then maybe Groww is more like the Freedom251 phone then ![]()

Ah, what a delightful conundrum we find ourselves embroiled in, dear readers.

**

The distinction between Zerodha and Groww

**

Although seemingly arcane and pedantic, it unveils a most intriguing tale of emotional persuasion—a tale distinguished by the divergent charms of our protagonists: the dashing Karthik Rangappa, steward of Zerodha, and the demure Aleena Rais, the luminary of Groww.

In the Zerodha corner, we have Mr. Rangappa, an individual who possesses the uncanny ability to transmute the most perplexing of fiscal enigmas into the very essence of simplicity. Like an alchemist of old, he can turn the base metal of inscrutable financial jargon into pure, shining comprehension with a mere arch of his eyebrow (a figurative one, naturally). He is not merely a purveyor of financial wisdom; nay, he is a raconteur of finance, rendering it as engaging as the latest fashionable novel. One could almost envision inviting him to a soirée, not solely for monetary counsel but also to infuse one’s gathering with the elixir of wit and charm. In the company of Mr. Rangappa, one needn’t fear fiscal discussions, for they are transformed into a most diverting intellectual amusement.

And then there is Miss Aleena Rais, the enchanting curator of Groww. Although lacking Mr. Rangappa’s charisma, she brings to the fore a distinctive narrative style. She possesses the knack for metamorphosing the dullest of financial advisories into a melodious lullaby for the soul. Her discourse on the intricacies of mutual funds is akin to a fireside tête-à-tête with a cherished aunt. One may not find oneself convulsed in fits of mirth, but the solace that emanates from her words can envelop one in a cocoon of financial serenity.

Thus, in the realm of emotional resonance, one stands at a crossroads, akin to a character in a Jane Austen novel, choosing between a dashing wit and an enchanting lullaby. Shall one opt to be enlightened amidst mirthful banter with Mr. Rangappa or prefer to be ensconced in a reverie of financial prosperity guided by Miss Rais? The decision, dear readers, rests solely in the realm of your inclinations. In the realm of finance, choice reigns supreme, and it is incumbent upon you to elect the proponent whose persuasion best aligns with your humorous sensibilities or contemplative fancies.

I just gave a like for the english you used.

Mast tha bhai 75% samaj nai aya.(in a positive tone)

![]()

Would you like me to make it easier to understand? If you wish, please feel free to request a simplification, and I shall gladly oblige.

No need.

Let me try so that I can learn new words & improve by english ![]()

Well, I started by saying that I’m obviously not comparing Groww to Apple or the android revolution (that would be farcical at this point of time, as you also unsubtly pointed out), but rather Zerodha to the Nokia of mid ‘00s (a compliment, you see!).

To elaborate it further, it was more of an observation coming from seeing a lot of responses from zerodha outrightly dismissing ideas/ requests. But I replied on the wrong thread I guess where we were only discussing zerodha’s philosophy on advertising (and I was corrected in the subsequent reply from Nithin), and I shut up right there. However, you never know, a ‘revolution’ might just be around the corner.

PS: we see things the way we want to see them (selective distortion)

Thanks for clarifying.

About Zerodha,

i believe most of the comparisons with “competitors”

and the “Why don’t you do this…” questions that we see being posed to Zerodha/Nithin,

are making an assumption that Zerodha wants to be the largest (or wants to grow further),

and wants to cater to every whim of the fickle-minded public to retain/grow its market-share.

From what Nithin has mentioned several times in many public forums, that is NOT the goal. ![]()

IMHO, not really.

That (Nokia), was admittedly oversight (in hindsight).

This (Zerodha), apparently is by choice.

People dont do what they think is unnecessary. It is only later on that it is proven to be oversight/bad choice or good choice.

If God tells @nithin his “choice” will destroy Zerodha, he will do his best to avert it. Its just that he doesnt think he needs to do “more” right now. He probably feels enough work has been done as per Indian Standards (not global), now its time to relax (wrt Zerodha) and rake it in…

At the risk of spamming the whole community here, here’s my follow up response (it’s hard for me to resist the temptation of responding to an online argument, specially when hiding behind anonymity).

Being more specific with an example on the why/ why don’t discussion - and this has nothing to do with being the largest broker in the market. Zerodha reasons that higher brokerage disincentives over-trading and thus saves retail traders - helping people do better with their money. I don’t think we have data that indicates that there’s an optimal trade count for profitability, post which we start seeing decline in profits, so just a convenient thing to say. A counter argument to that will be: low brokerages will help small traders better position size their trades - brokerage is a significant cost when trading in small lots, hence incentivises retailers to trade in larger lots to improve the cost efficiency (I guess only data can prove which will help retail traders more - avoiding overtrading at the cost of higher brokerage or better position sizing with low brokerages).

But again, I must admit this was not the best thread to discuss this - thereby creating confusion.

I missed using the term ‘hindsight’ and am glad you referred to it. I guess how things pan out ultimately decides if a strategy was good or bad. What’s actually bad is that we’ll only get to know that in hindsight.

i am not sure that is the case. ![]()

Especially if this “destroy” results in the greater good.

But hey! that’s just my opinion based on what i have seen/heard.

(Feel free to share any observations that contradict mine. Happy to catch anything i may have missed.)

Again the same old assumption i was trying to highlight.

Depending on what one values the most,

Zerodha has already surpassed what any brokerage has achieved globally.

Note that this does NOT mean Zerodha is at its end or has stopped growing.

It is growing and will continue to grow.

Just not in the ways other brokerages are trying to.

Nor how the “pachees-din mein paisaa double!” crowd is looking to.

Continuing with the Nokia analogy,

did you know that -

before focusing on phones and networking devices,

Nokia used to make toilet-paper and rubber-boots ?

…and Nokia “destroyed” their paper and rubber businesses,

when they entered (and later dominated) the electronics business.

Have you explored Rainmatter ?

(and noted its focus/brand, as it has been evolving over time)

PS: Not sure about the others reading/participating in this topic-thread, but i am finding this discussion weirdly satisfying//fulfilling.

Sharing the bits i had noticed. Getting to know few bits that i had overlooked.

In the end, not knowing which ones are the significant "bits".

What according to you are choices taken for the “greater good” of retailers?

I guess the real threat to zerodha will come from banks. Hdfc launched its discount broking platform sky few days ago. Soon others may follow. This will allow seamless transfer/withdrawl of money from bank to trading account to bank and vice versa. The likes of zerodha can tie up with banks to offer 3 in 1 account but it involves two entities. If everything is done by single entity it gives more confidence. Same thing happened in case of full service broking. Once all major banks were into it, they became market leaders. The likes of sharekhan, angel etc still existed but were behind the banks

Unfortunately HDFC Sky is not viable for most Option traders, they charge interest on collateral margin unlike most discount brokers. Kotak fits better.

Current banks will never be able to compete with new age brokers like Zerodha or Groww imo. They are stuck in the old mindset. Just see HDFC Bank netbanking UI. It’s not even full 16:9 and just has whitespace. The UI is so old (I think 10+ years at this point). Their support is so hard to reach with very bad implement of IVR. A lot of things can’t be done in their mobile app and many thing can’t even be done in netbanking and you have to physically courier forms. The only important thing imo where you have to courier forms to Zerodha is DDPI. All other major things can be done fully online.

Also most people don’t really care about 3 in 1 accounts and seamless transfer/withdrawal. With UPI upto 1 Lakh instant and very easy to do. And with the new ASBA method by SEBI you don’t even have to transfer money to Broker.

The only banks who would be able to tech advantage of these seamless features would be new age neo banks. But they aren’t really building a brokerage business right now.