First of all I would like to appreciate Zerodha and team for doing great work to the investors and traders.

I would like to know the difference between investing directly to a mutual fund through their website (for eg: reliance mutual fund) and investing directly to a mutual fund through Coin. Any difference in amount will be there in the end?

Easy SIP, start stop whenever you want without any NACH requirement. Increase or decrease SIP values at will.

NAV tracking orders. Similar to stocks, place orders to purchase or redeem funds based on NAV.

MF in demat form and hence fungible. Extremely easy to pledge and take a loan against in case of emergency.

Single capital gain statement, P&L, visualizations, and more.

MF or stocks in demat are much easier to claim by dependents (nominee of demat) in the case of death. Direct plans with multiple AMC’s would mean multiple folios, difficult to aggregate and claim.

If no investment (lumpsum/SIP) done in a month still subscription fee of Rs.50/- applicable for that month after first free Rs.25000/- investment limit is over?

Then why is Zerodha offering regular plan, if direct plan is more profitable as claimed? Anyhow investor has to pay upfront and trail commissions (at least 2% as said).

We went direct this April, until then there was only regular as there was no way to sell direct in demat for us. Once we went direct in April, surprisingly some clients wanted us to continue offering regular also. So yeah, as you can understand not everyone gets the concept of direct funds.

Hello Shivam

We’ll start by answering the second question first.

Balance is an everyday savings app. Investment is simply incidental. Balance helps you save towards your short term goals, by building an automated saving habit around your lifestyle. Think of Balance as a savings coach, that helps create save suggestions and offers a seamless way to save while going about with your daily life.

To answer your first question. Yes, Balance invests your saves in regular funds, which do carry an upfront and trail commission, however for the ICICI Prudential Money Market fund, there is no upfront commission and the trail commission is as low as 0.025% .

Balance at the end of it all, is a FREE everyday saving app, we filter out the noise that is present in an overcrowded investment market and hand pick the ideal fund to use as a saving tool. On top of this all, we adapt around your lifestyle, we do all the dirty work associated with saving and investing, ensuring that you never do more than picking a goal and approving a save.

Hello,

You are saying that if someone invest Rs 5000/- per month over the period of 25 years, he will pay Rs 15000 for 25 years of Zerodha’s Coin service.

Now my question is will Rs 50/- per month will remain for next 25 years. If yes that’s great. If not what will be the increase in % or as compare to Zerodha competitor.

Thanks.

As i understood, with Rs 600 per yr, as subscription of coin, you break even if you purchase MF worth 1,20,000 and compare it with 0.5%trail commission which the fund houses generally charge. (IIFL for ex). Thus, if your total purchase from coin is between 25,000 and 1,20,000 rs you would be at a loss. If it is more than 1,20,000 (over all mutual funds on coin) you stand to gain.

PS I have discounted upfront commission as it would be marginal in the long run and also assumed that zerodha will not incr Rs 50 per month subscription at least for the next 10 yrs

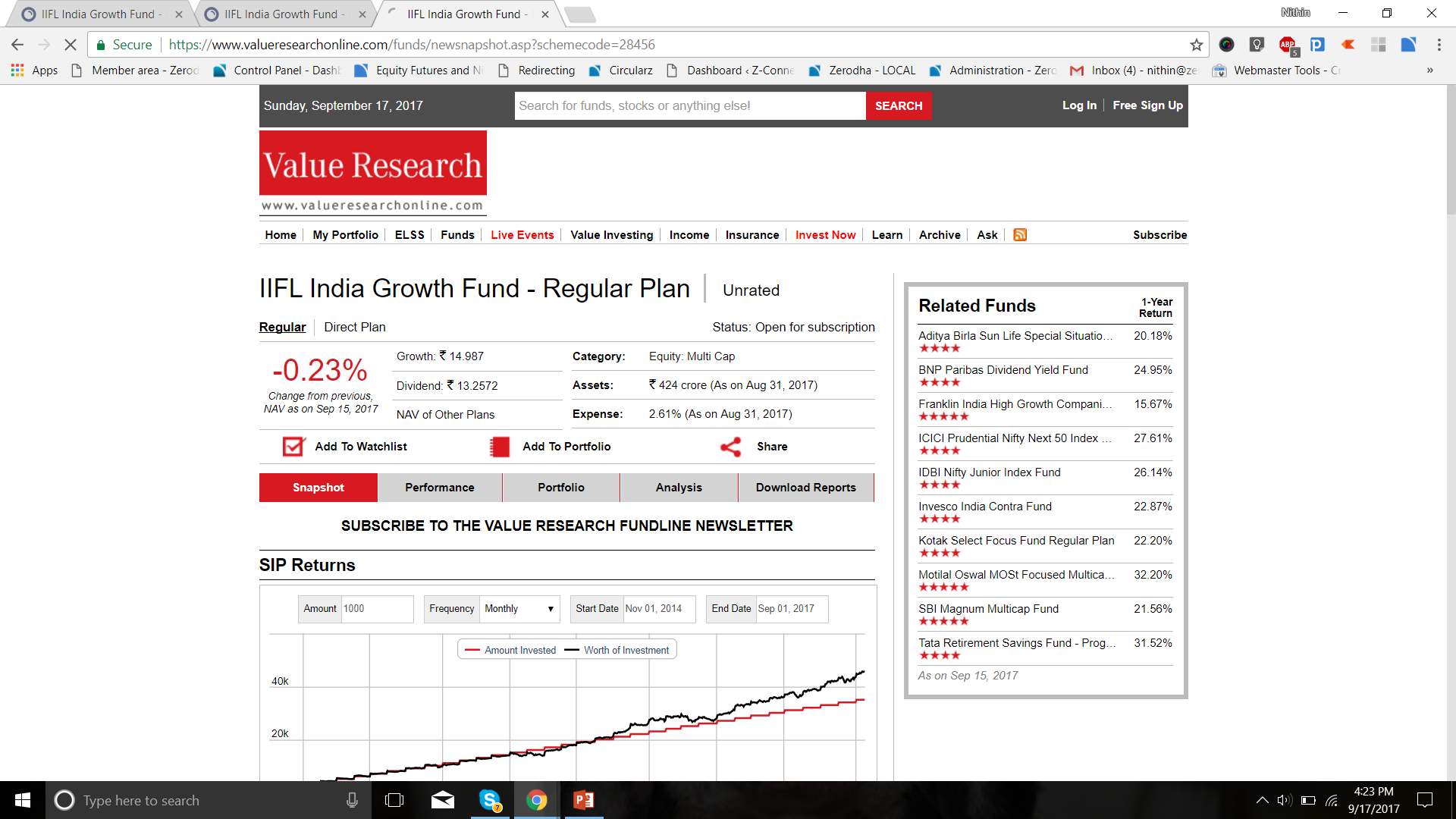

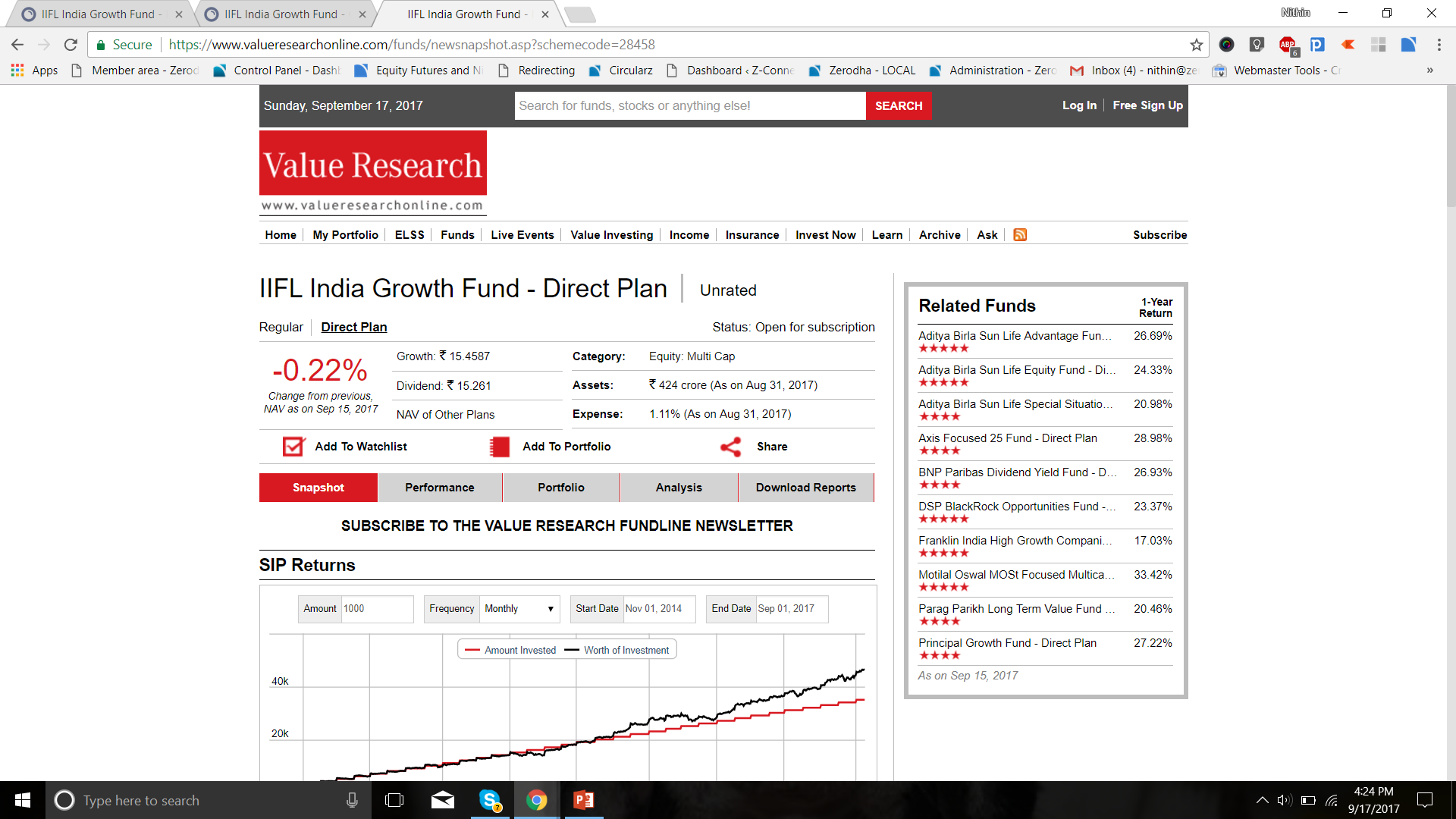

hmm @nachiketa02 … I don’t know where you got this info on expense ratio of IIFL. Here is the link at Valueresearch, Expense ratio Regular 2.61 Direct 1.11. That is a difference of 1.5%. Expense ratio is debited end of everyday. So this 1.5%/365 daily extra is what you will pay for regular funds. This in absolute terms will be much more than 1.5 if market goes up because it is debited everyday and also since the value of your invested capital reduces everyday.

Also your comparison is not right, because you are comparing for only one year and also assuming no capital appreciation or addition of capital. Expense ratio is a % charged daily. Coin charges are flat 600 bucks a year (maybe cost of a meal for two at not an expensive hotel) :).

Anyways, we had done the calculations on DSP, which has similar difference in expense ratio. 5k SIP over 25 years, if markets returned 15% would mean almost close to 30lks extra by investing in direct. Even if 50 on coin increases over the 25 years, the savings can’t be compared.

If i sell mutual funds and my investment through Coin platform decreases to below the limit of Rs. 25000, will the subscription charges be applicable then too ?

@nithin

What if i start a SIP of Rs 5000 per month for say 10 months. After 5 months i would be charged for Rs 50/m for next 5 months. After 10 months i stop this SIP. But the holdings of this SIP is still present. Will i be charged Rs 50/m till the time am holding ?

Yes, it will be applicable. There wont be any charges applicable for initial investments upto Rs 25000 but post that if you redeem and invest again or if you invest further, then charges would be levied.