Anyone can answer how it is better than Kuvera where there is no charges for Direct funds with no limits. Why Zerodha could not provide such service. I recently opened Zerodha and planning to move my MF from Kuvera to Zerodha. But Rs.50 per months feels like too much for direct funds as we are already paying AMC for Zerodha

I really don’t understand this “I want everything for free logic”. Coin is a business and it costs money to run a business. Ok let me try to understand this,

you want lots of features

Good support

But you don’t want to pay? If you were a CEO of a direct MF platform would you offer it for free?

How much are you investing every month?

Charges are not everything. When you pay to use a platform, that means the platform has the responsibility to continually better itself. That is one of the major reasons why you pay. I really don’t see how Kuvera can offer it for free and survive in the market.

When they went free a friend of mine received an email from them which said that they are going to make money for PMS and advisory? Now we have people who have qualms about paying a meager Rs.50 do you think they will pay at least 6X that for advice? Sound fishy to me.

It is not like i am looking everything for free. I am trying to understand a comparison between a free service and paid services. When i am paying obviously i will look for a platform better than free one. I am trying to get is it really a worthy spend for that platform.

@nithin, @Sanket

Please can anyone of you clarify on the question put up by Vijay?

This is important query as i also would like to clarify on the same as we are talking about long term investment.

The charges might go up over the years. It has to adjust for inflation. But how much ever it goes up, the savings will be much much more compared to regular funds. When inflation goes up, the value of your investments also would ideally be going up. Instead of 5k, you might be investing 10k per month in 3 years, and so on.

If you are comparing us to another competitor who is offering direct MF - what we earn forms less than 0.5% of our revenues. Whereas competitors are relying on this 100%. So if anyone can keep the rates low over longer period of time, it would probably be us. We started our broking business at Rs 20 per trade almost 8 years back. The rates are still there, actually has gone to 0 for equity investors.

4 Likes

@nithin

Thanks Nitin for the clarification.

Will the Rs. 50 charge be for each MF in the portfolio or would it be every month Rs. 50 for entire portfolio??

Rs 50 is for entire portfolio, as much of as many funds as you want. Also this Rs 50 starts after the first 25k worth of investments.

Thank you Nithin… I appreciate the promptness for your replies for clarifying my doubts…

Hello Nitin,

Must Appreciate for lunching coin, it’s literally a Departmental store for any investment needs…

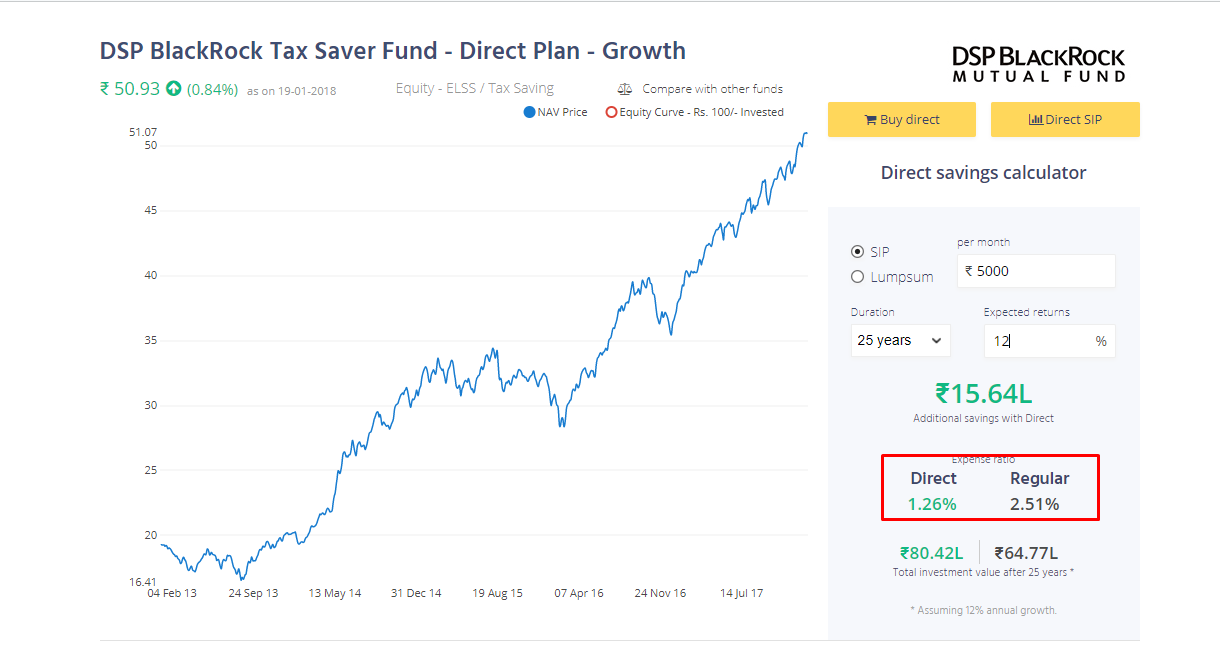

My Questions are : if someone buys a *DIRECT mutual fund from (For, Ex: hdfcmf.com) , The expenses ratio is : Approx 1.3% .

- Now what *monitory extra benefit Coin is Providing (i have already gone through The advantages you have on coin.).

- Do we have 1% *Upfront & 1% *trail commissions every year, on our investments in Direct Plan as well .

- if “NOT”- then -> It’s Saving rs.600/year (beyond 25k investment ), Buying/sip Directly from Mutual Websites on any Direct plan ? -> am i correct.

i am already coin user (i.e: know the demand of running business rs: 600/year is logical), But it would be really Helpful if you clearly answer my 3 questions & correct me -if my understanding is wrong.

The difference between a regular and a direct plan is in the commission you pay. In a regular plan, you pay higher commissions and direct yo don’t. The reason is the AMC pays distributors commissions to distribute the scheme and those commissions are paid out your invested monies. In a direct plan, you save out on those commissions. Before you think that 1% is negligible, check the screenshot below to see how big of a difference a small % can make.

This screenshot is the answer to your question

Irrelevant.

Please clear my minor looking doubt…

If I invest (lumpsum) Rs. 20k in MFs, then I am exempt from Rs. 50 pm. But after a year NAV goes up and current value of investment crosses Rs. 25k. In that case, do I have to pay Rs. 50 pm, even if my initial investment was less than Rs.25k?

Penny wise pound foolish.

I am just watching people are desparate to save Rs 50/- per month and just forgetting the larger picture of making millions.

1 Like

@Ashis_Saha

Yes true you will save ₹600+taxes every year if you go with direct purchase with fund house.

But suppose you need to purchase SIP of four/five different AMCs you need to login to their website and keep a track.

If you want to pause, increase, decrease, stop…it’s very easy in Coin wrt to websites.

It’s like hiring yellow cab (old ones) in Kolkata and hiring Ola/Uber for a ride. Depends on you, which one suits you.

3 Likes

@nikhil27 perhaps winding your neck in is not the right approach if you do not know the answer. Ridiculing is not helping anyone where.

deactivates means I have to sell all Investment in MF ???

Yes, you can deactivate your subscription once you have exited all your investments.

Which AMC provides daily sip? Could u pls list them

I m newbie

Just placed 1 order. So is it going to execute tomorrow at 1:30 PM and 5000 INR will deduct from my account?

I think so.

If I were you I would have placed order of "DSP BlackRock Tax Saver Fund - Direct Plan - Growth"

There is no exit load.

The current Price is attractive to buy right now.

Update:- 1

I see Exit load of 1% in Reliance Small Cap Fund - Direct Plan - Growth