You very well are aware of the allegation by Cobrapost that the company has siphoned off Rs 31000 crores. If not here’s a short explainer

Anyways, in India, the corporate bond markets are in their infancy. To put that in perspective here’s an excerpt from the CRISIL 2018 Yearbook. The corporate bond market accounts for just 16% of the GDP compared to 46% in Malaysia, 73% in South Korea, and 120% in the US.

Anyway, bond yields and prices have an inverse relationship. Meaning, when bond prices rise, yields fall and vice versa. If you are beginner, then you might ask the question why? Here’s an explainer from PIMCO

A bond’s price always moves in the opposite direction of its yield, as previously illustrated. The key to understanding this critical feature of the bond market is to recognize that a bond’s price reflects the value of the income that it provides through its regular coupon interest payments. When prevailing interest rates fall – notably, rates on government bonds – older bonds of all types become more valuable because they were sold in a higher interest rate environment and therefore have higher coupons. Investors holding older bonds can charge a “premium” to sell them in the secondary market. On the other hand, if interest rates rise, older bonds may become less valuable because their coupons are relatively low, and older bonds therefore trade at a “discount.”

Oh, in case you are wondering about the normal range of yields:

The 10-year government bond is yielding 7.5%

AAA rate PSU bonds are in the range of 8.5% to 9.5%

AAA rated corporate bonds are in the 9% to 10.5% range.

What if company (in this case DHFL) goes bankrupt, still company is liable to pay interest?

Ie if I buy these bonds from second market (zerodha) at discount will I get interest and full amount on maturity date?

If the company filed for bankruptcy then nothing is guaranteed, if the bond is secured enough then you may get your capital back, if it is unsecured then it depends on the cash received upon auctioning of it’s assets, first that cash will be used to repay senior secured bond holders, then secured, then unsecured and finally to equity holders, incase if anything is left out after paying all creditors.

@RahulKhanna, Thanks for posting this. Your post is really helpful.

I set out yesterday trying to understand the bond markets and I realised that information is so so difficult to come by. Cobrapost and other recent default news led me to believe that there are opportunities to make money for investors willing to take the risk.

To make any logical sense of pricing, one has to source data from so many different locations - understanding the nature of instrument, understanding market price, calculating yield, and then finally actually making the transactions!!!

Would you be able to share your information sources please? YTM screenshot is from BSE? What is the best source to view instrument terms, calculate YTM etc?

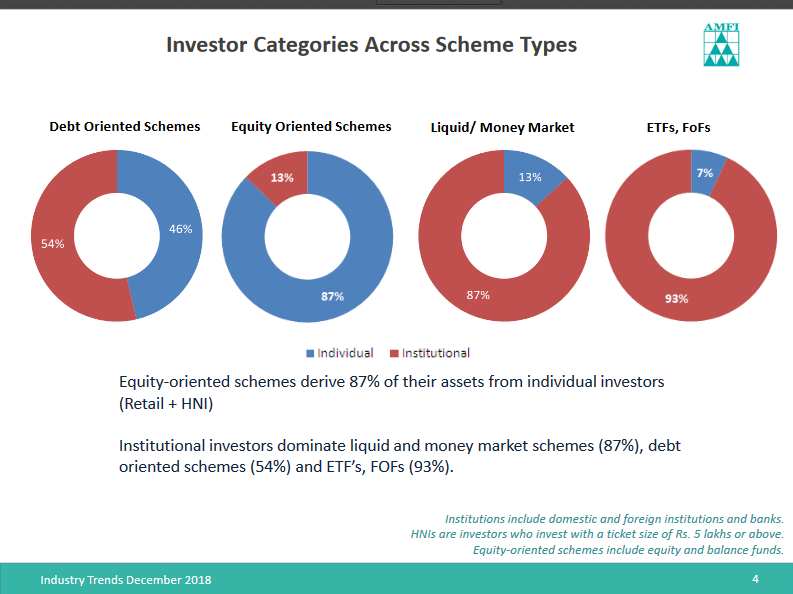

Yea, bond markets are not really our (retail investors) thing in India. Even when it comes to debt mutual funds, the retail crowd has stayed away. Here’s a stunning stat from AMFI

I’d wager a guess that out of the 46% Individual shares, a lions share will belong to HNI’s.

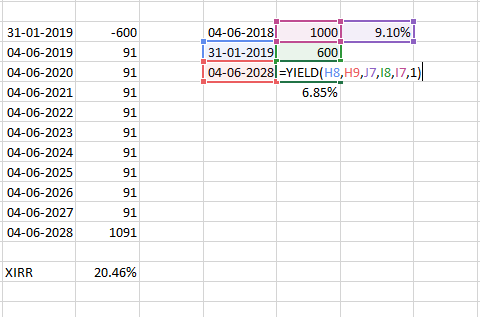

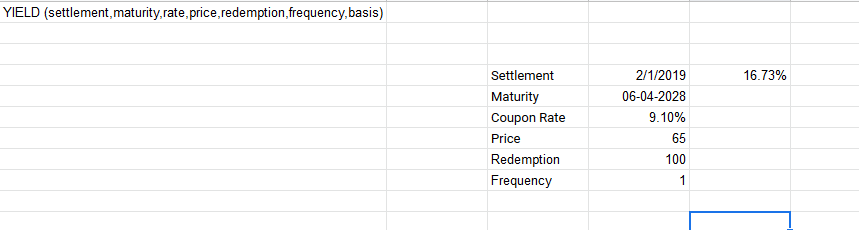

True dat. The screenshot of the yields is from NSE. You don’t have to calculate the yield, but if you want, just use the YTM formula on excel. You can find the FV, coupon in the prospectus of the issue.

Oh wow! This is so so helpful! Appreciate you helping out.

I completely agree with your views on lack of retail participation in the debt markets - I think all the complexity and gaps in information availability have led to this dissonance - and of course, yield movements in non g-secs are not as "sexy"as reporting equity gains / losses on a continuous basis. I do not think there is any resource out there that plots YTM!!!

I was sharing some debt MF performances (8-9%) over the years, compared to the last 3-4 months where most equity MF funds have lost money. I could not get my head around to why debt funds would fare in such a consistent / linear manner despite all the recent upheavals in yields / defaults - clearly, there is an opportunity for retail investors.

Hopefully I will be able to identify some investable opportunities. Do keep sharing insights, like you did for DHFL.

True dat. I remember a quote from this podcast. Reminds of this passage from this podcast

Bond market as being like a giant and anaconda sitting in the corner of the room. The Anaconda sitting there its heads looking out its observing everything and it’s so still that everyone forgets that it’s there but all of a sudden that giant anaconda moves its head a little inch to the left an inch to the right and the whole world shits itself.

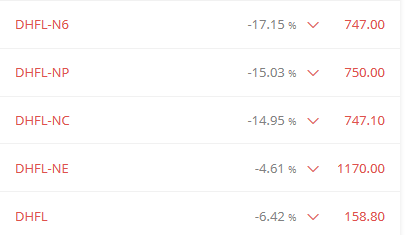

The yields are high for a reason - the NCDs are secured by a first charge on assets; which in the case of DHFL are loans given to their corporate and retail clients. A significant portion of these assets will turn into NPAs if the allegations by cobrapost are true. Hence secured NCD holders would likely suffer a significant haircut if DHFL becomes bankrupt, resulting in liquidation.

Thanks! I was aware that XIRR would not be the right way due to the inherent assumptions of IRR - but just wanted to try it for a ballpark return since I was getting a whacky number through the YIELD formula - thanks to your worksheet also realised the silly error I was making - FV of 1000 instead of 100

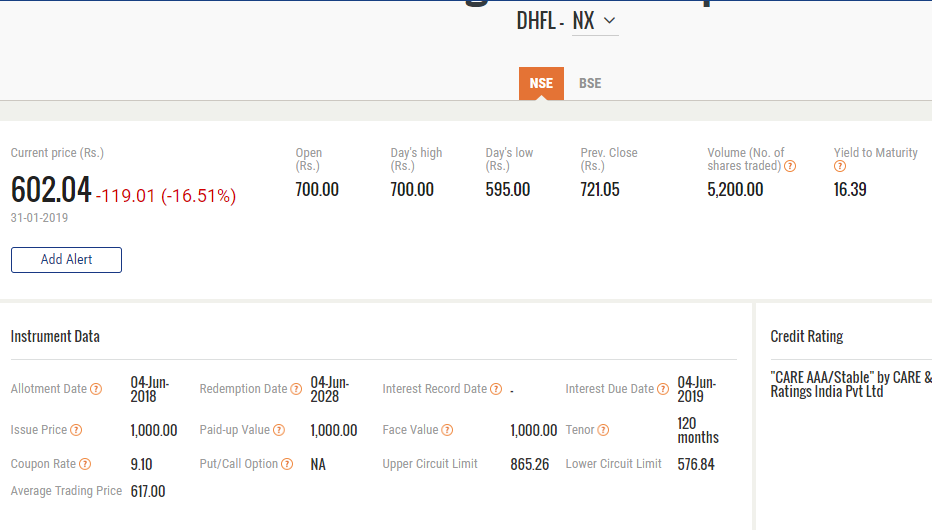

Also any reason why yields are not showing up for DHFL on BSE?