SEBI has asked AMFI to direct all asset management companies to restrict inflows into international exchange traded funds (ETFs).

What does this mean?

SEBI has prescribed the following limits for international mutual funds, fund of funds (FOF) and exchange traded funds (ETFs):

Mutual Funds can make overseas investments subject to a maximum of US $ 1 billion per Mutual Fund, within the overall industry limit of US $ 7 billion.

Mutual Funds can make investments in overseas Exchange Traded Funds (ETFs) subject to a maximum of US $ 300 million per Mutual Fund, within the overall industry limit of US $ 1 billion. — Circular

In 2022, Indian funds started hitting this limit of $7 billion for mutual funds and $1 billion for ETFs. So funds started restricting fresh inflows and ETFs halted fresh creations.

After the correction of global markets, especially the US in 2023, funds started accepting money because there was some space. But given that most funds are US-oriented and the US markets are at or near the lifetime highs, there doesn’t seem to be any space left in ETFs to create new units. Also, fresh inflows into the fund of funds (FOF) that invest in the underlying ETFs will have to stop as well.

Will the Reserve Bank of India (RBI) increase the limit?

Don’t think so. In general, the government isn’t keen on letting money go outside India. Also, here’s what the RBI governor had said when a journalist asked him the same question:

Neil Borate: Sir, this is Neil Borate. I am a Deputy Editor at Mint. The mutual fund industry’s overseas investment limit of US$7 billion has not been raised by the RBI. All funds were stopped from investing fresh money overseas from February 1, 2022 and in fact, this limit of US$7 billion was set in 2008 as far back as that. Now US$7 billion is a tiny blip in our Forex reserves of more than US$600 billion. So, what is the RBI’s stance on this? Why should this not be raised?

Shaktikanta Das: This request has been coming to us from the mutual fund industry from time to time. We have just come out of the pressure on our currency which we witnessed in the aftermath of the starting of the Ukraine war. From February 2022 onwards, the Rupee exchange rate was under a lot of pressure. Initially, there were a lot of outflows. So, it is a question of timing. We do not question the basis of their request. It is a question of the right time for us to do it. We have just come out of the stress on the exchange rate of the Rupee. We experienced huge outflows. Now things have stabilised, and the Rupee has remained very stable. Of course, some people read it wrongly and call it a stabilised arrangement. But it is not stabilised. It is market-determined. If somebody wishes to call it stabilised, so be it.

In the description of the Indian rupee as a stabilised arrangement, the fundamental strength of the Indian rupee is being missed out. They are, the strength of the macroeconomic fundamentals of the Indian economy, the resilience of the Indian financial system, the return of inflows into India, FPI inflows in particular. FDI inflows this year are less than what it was last year, but given that the global FDI volumes have gone down, in that, India’s share is one of the bigger ones. So, these are the points which are being missed out. Our exchange rate system, our economy today is not what it was a few years ago. But that is beside the point.

Coming specifically to your question, I am not questioning the genuineness of their demand. It is a question of timing. When we feel confident that things are, it has to be stable on a durable basis. It is already stable. We will take the call at the right time. RBI

What will happen to my investments?

Your existing investments in ETFs will be unaffected, but the AMCs will stop creating fresh units. However, the existing units will continue to be traded on the exchanges.

Let me simplify that further.

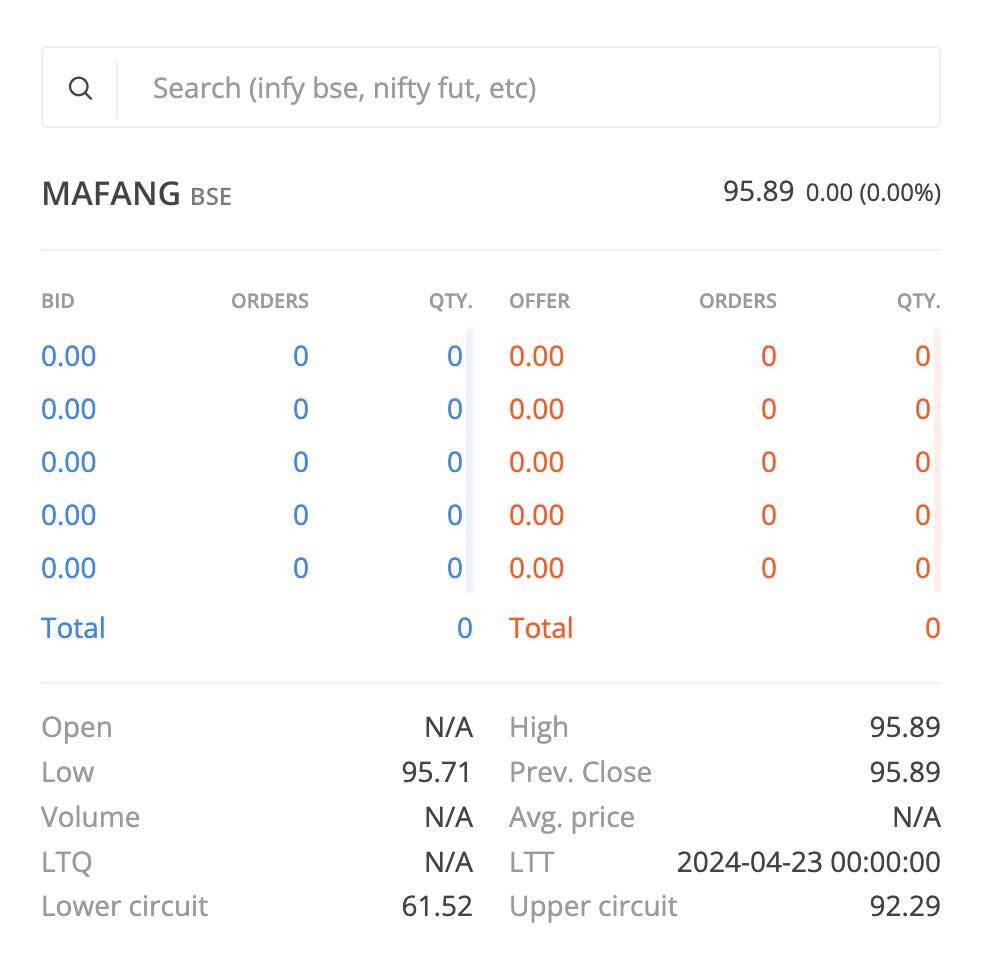

ETFs are a little different from MFs since they are listed. If a mutual fund stops accepting fresh inflows, there’s no way you can invest more in the mutual fund. But an ETF is different. The way ETFs stop accepting fresh inflows is to stop the creation. In other words, they stop creating new units, but the existing units can be bought and sold without any issues. But this can create a problem. When buying an ETF, you have to pay attention to two numbers:

- The price of the ETF that you see on Kite or other trading platforms. This price is based on the demand and supply of the ETF on the stock exchanges.

- iNAV or the Indicative or Intraday Net Asset Value (iNAV). This is the fair value of the ETF, or the current market value of the underlying holdings.

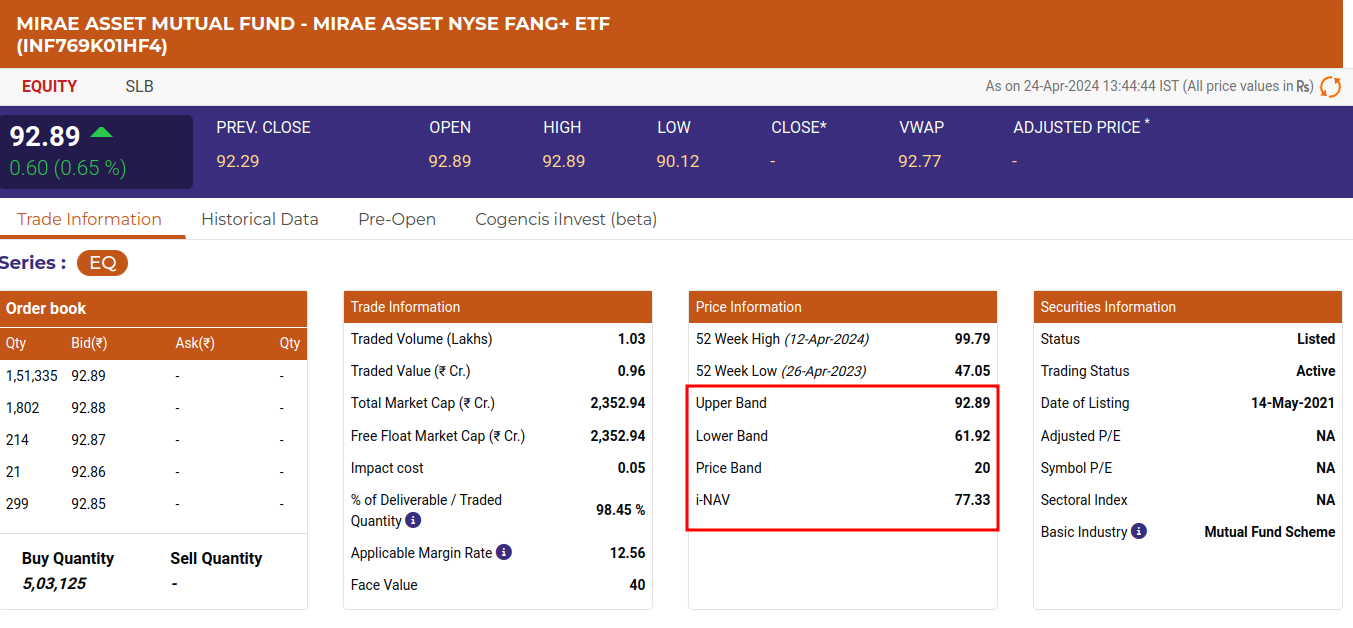

If an ETF is liquid, both the price and the iNAV will be close to each other. But sometimes, they can diverge quite a bit. In such cases, the market makers and authorized persons of the ETF can go to the AMC, give them cash for ETF units or ETF units for underlying stocks, and arbitrage this difference. I’ve explained creations, redemptions and arbitrages in detail on Varsity:

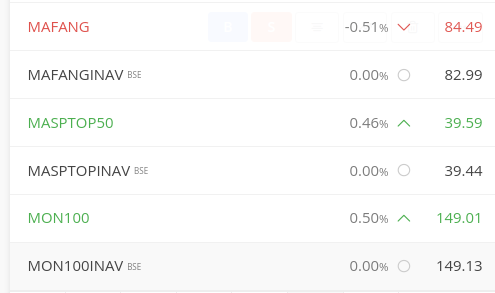

This means that these ETFs can trade at premiums and discounts compared to their underlying NAV. So always check the Indicative or Intraday Net Asset Value (iNAV) of the ETFs before placing an order. Search for an ETF symbol and you will see the same symbol with the “INAV” suffix.

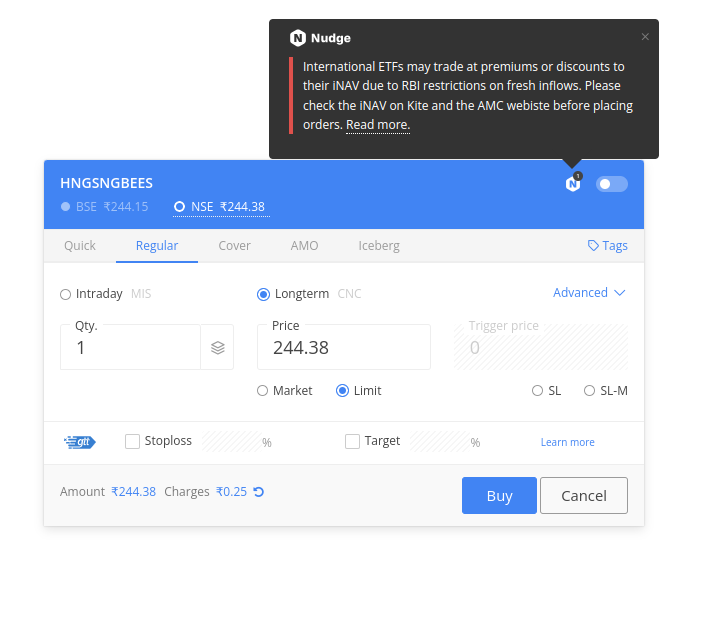

We will also start showing a Nudge on Kite like this:

Does this affect international mutual funds?

It depends on how much space the AMCs have. But it’s safe to assume that if the international markets keep going up, whatever space the MFs have will be exhausted, and they will have to stop accepting new inflows. So far, only Motilal Oswal has stopped lump-sum investments but is accepting SIPs in two of its international mutual funds:

MOTILAL OSWAL NASDAQ 100 FUND OF FUND - DIRECT GROWTH

MOTILAL OSWAL S&P 500 INDEX FUND DIRECT GROWTH

Let me know if you have any questions.