See as a resident indian and retail investor there is no scope for me to buy usd and keep it for my children education. Now they have gift city etc.

earlier nri could open fcnr usd deposits and save it for their kids education

For retail redident investors. We have no option. The only alternative is usd denominated investments as mentioned above

The advantage is apart from the growth from the undersyling securites we indians get the benefit if inr depreciating. This is constant

See as an example in 1991 the conversion was around 18

In 2018 it was 69

Now the rate is 87

How do i protect myself. By buying this. If i had bought any of the three etf in 2018 apart from the growth of the underlying securites currency depreciation from 69 to 87 would be a bonus.

This is what i meant.

Apart from this you can think of investing in tcs.

This is because almost all of their revenue is in usd.

So if revenue is x in 2018. Actual revenue woukd be x muktiplied by 69

If revenue is still x in 2025. The actual will be x multiplied by 87.

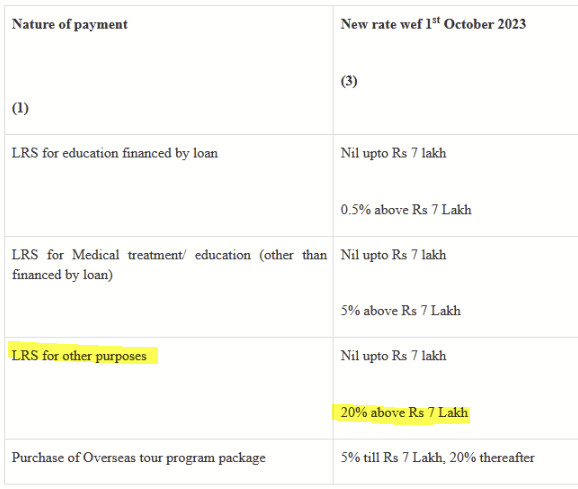

What’s the current %-premium on these instruments?

Is it larger than the friction due to TCS withholding on any outward-remittance under LRS?

If not, then sounds like investing in US T-Bills or some high volume US ETF tracking S&P500 directly might be a more flexible option for resident indians as well?

I mean investing directly in equity and debt products listed in the US stock exchanges using a broker that supports investing in foreign stock exchanges - not some proxies (like these Mutual funds listed in India) or derivatives listed in the Indian market that provide indirect exposure to the same underlying instruments in the US.

For example, can buy and hold QQQM, or VOO or even BND using an online international broker like Charles Schwab or IBKR or Vested or some such broker whose offerings and pricing one is comfortable with.

etfdb.com appears to be a site with various handy tools to explore and evaluate the huge array of international ETFs on offer.

For, significant sums of money,

this approach of direct overseas investment

would currently add some friction

in the form of TCS on any outward remittance under LRS.

TCS on LRS is NOT an actual tax-liability. It is simply amount paid/withheld upfront during outward-remittance under LRS. It can be adjusted against any actual taxes due (eg. quarterly advance-taxes, monthly TDS on salary, …).

Note, that the effect of the TCS on LRS can be reduced/nullified in certain scenarios as the TCS amount can be -

claimed periodically to offset any TDS / advance-taxes due.

i.e. avoid having to wait to claim it at the end of the year upon filing one’s ITR.

Also, if one already has foreign-assets (and is looking to diversify them), or has foreign-source income, one may be able to re-invest the proceeds without having to repatriate them first to India, thereby avoiding the friction due to exchange-rates and TCS on LRS. Here’s an example scenario How to Diversify Foreign ESOP & RSU Holdings Through Vested Platform. Please consult a CA for other specifics including disclosure of foreign assets, tax on income, and claiming tax-relief of any tax withholding in the US (eg. IRS - W-8BEN, 1042-S, ITR - Schedules FA, FSI, TR and Form-67) as would be applicable in each individual’s case.

Could you give us a number (x number of rupees) that you do to protect from downside? I want to understand it because the larger it gets the better it provides health against depreciation and riskier it gets (downside of concentration, liquidity etc)

The purpose of buying these ETF is to invest in a USD denominated instrument. @CVS had mentioned to directly invest in US Markets, which with my limited income and ability not be able to do so. These ETF as long as the underlying is US Market companies, I am perfectly happy to invest in these in INR.

I buy these funds regularly in very small quantities. Few months I dont even buy. But the intention is to accumulate and keep it for a long period of time hoping that when I need actual USD, these funds will be of assistance.

Did not understand your question entirly - but could say this

Nasdaq 100 ETF - I started buying when it was 134 - 140, sold a portion when it went to 200, Now it is 210 or so. My average cost now is very low and the balance units I will not sell even if it falls. The profits from sale is kept it in a separate FD. So when I actually need to buy USD, this profit and sale from the existing units will act as a buffer against the future currency depreciation. This is my thought but as they say “women proposes, God disposes”

With regard to Liquidity - These ETFs are facing the same hence on days you see only buyers and not sellers. However, the liquidity crisis is not affecting the existing investors as they are the beneficiary as these ETFs are at a premium.

Yes, the reverse could happen where there are only sellers and not buyers - but I am willing to take a chance and it might fall back to the real NAV.

For the sake of completeness, i would like to leave a mention of purchasing fractional units of US stocks (or even ETFs) being supported by major US brokers. The additional risk being that the fractional units are guaranteed by the broker, so extra risk concentrated with the broker.

This enables one to start investing into US securities with as little as 500 INR fractional-units/slices at certain US brokers.

Note: None of what i’ve shared above is a recommendation to invest in US stocks or get USD exposure. Personally i believe that it is a sub-optimal venture right now. However, if one is interested to get USD exposure, these are direct alternatives (with their own distinct risk-reward profiles) to the ETFs / Mutual Funds in India that provide exposure to the US market, and are apparently trading at a premium due to their limited supply.

@Bhuvan Good knowledge share but how can one ascertain that he has etf are really consisting actual international etf .like I have mon100 bought 20sep2021 to 19jan 2022.

Are they really mon100 as you said RBI has stopped new mon from 2022.

Secondly when the etfs are transacted despite RBI stopage.are these exchange of etfs internally in Indian market consist of actual mon100 consisting shares of us.

Nicely written, though i don’t fully agree with below

To reiterate, if you’re getting Nifty-like returns with half the risk, you’re in the process of being scammed. If you want less risk, you will have to sacrifice returns. You have to be OK with underperforming a dumb strategy like buy-and-hold.

Nifty is not a very high bar in either returns or risk from active trading pov. Hopefully this applies to investing type trading too, but i haven’t done that yet.

Anyway, would be interested to see if commodities other than gold can give some diversification too. Ray dalio i think suggests that as part of a mix. Perhaps we have periods where other things don’t work well ? Maybe with longer data including 70s and earlier ?

Also, when can we expect to get a Zerodha Mutual fund that implements these insights ? This would be esp good for retired folks. An all seasons Zerodha fund, backed by research

What I said is in the context of investing. If someone tells you you can get equity returns with debt-like volatility, then I don’t know what it is if not a scam. It’s not about trading or “beating” something, although even that has been a big bar for a lot of people. If you are able to beat Nifty, then you are a better investor than I

This is a nightmare of a debate. In theory, yes. For example, commodities (a basket of them) are often the best hedge for inflation, but they are inaccessible for retail investors. You can implement it through futures, but you’ll get killed because of roll costs and the associated taxes. So, does this offer a diversification benefit? Yes. But the penalty is in the form of lower returns. I’m not a fan of these for most individual investors.

Only intraday trading, so not fair. And nothing like debt risk. Will try for investing in future, hopefully will get something.

yeah, from individual point of view, this is too much of a hassle anyway.

I meant mutual funds. But if costs are too high here, then i guess advantage is lost.

Dunno, never tested myself.

Nice to hear, will be good for pledging too.

Another possible thing in future - With SIF funds coming up, shorting could be a way to reduce risk too. Would be a challenge as stocks go up, but even something that makes no money but hedges in crashes could be useful.

The data in NSE seems to be officially filed. So Kite(and BSE) seems to be in the wrong. This along with the nudge stating there may be too much premium/discount paints a misleading picture to investors that it is trading at a heavy premium when it is trading at par. @Bhuvan@nithin Kindly fix the Nudge to point ONLY to official website and remove “recommendation to check iNAV in kite” from the nudge.