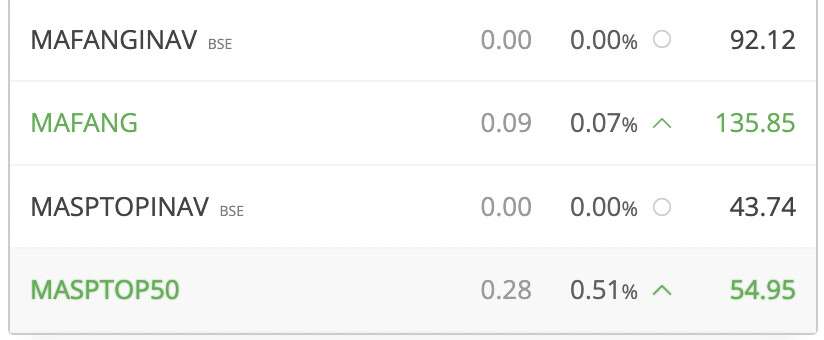

I check this and other two etf of mirae asset regularly and buy them too ie fang and s&p500 top 50

Many days in last month on all of the above 3 etf. there were no sellers and only buyers and hence the iNAV and market price had a lot of premium. This changed from last week of may when there were buyers and sellers. When it was active the market price always had a premium.

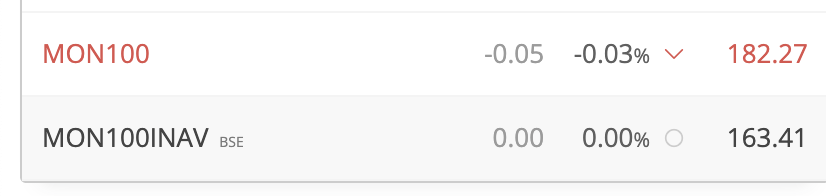

Today after reading the post and was surprised to see nasdaq 100 market price and inav price was the same.

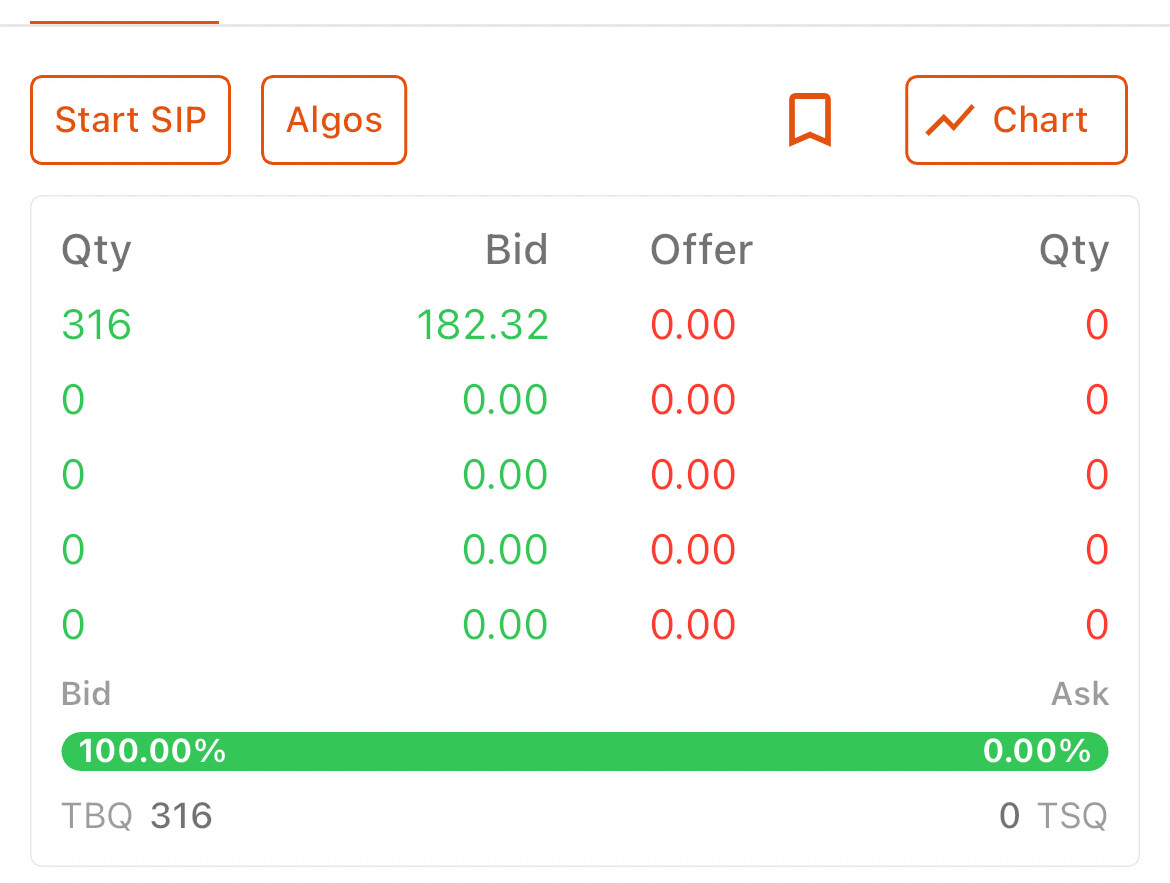

There was a buy order of 316 qty for a price of 182 and not a single seller both bse and nse. This was after market closure. In money control where i put my investments, the market price shown was always inav which was alwsys lower than the actual market price when buying/selling. I wrote to money control of this but never got a reply even during market time. The market price is alwsys dynamic for other shares and etf except these

I go to their main site to check inav only when I need to like this time.

Most of the time, my benchmark is my average cost (I am already invested) and what I perceive this fund will do for me in future. Not too much into if I got the inav price or not when I buy as the purpose is for long term, so not too bothered if the premium is 4 or 5 rs higher.

I am a Icici Direct customer so not able to guide you on zerodha details. Not sure why it shows 163. It should be a mistake either way. Either the AMC website is wrong showing inav as 183.15 or zerodha is wrong at 163.

Going by logic as I monitor two other us based ETF, I have a feeling the inav is 163 and market price is 182. I was surprised to see AMC website showing inav as 183.15. In any case I bought few units.

Hello,

its been 2 years since International etfs got banned

1.any 1 has idea when it going to unban?

2.amc fund houses progress about unban?

3.is it safe to invest in this premium?

as US market is going down now a days

I am a investor in all three

Motilal oswal nasdaq 100

Mirae asset s&p 500 top 50

Mirae asset faang

All three etf not fund. Motilal has everyday sellers and buyers like any other etf

S&p 500 top 50. Has sellers generally when market opens. And faang no sellers at all on most days

I invest as currency hedge against inr to usd depreciation.

Yes it is quoting at a premium of approx 15 percent to its inav but this does not bother me. I will be holding it for a long time.

The constituents are well known names and i want to be invested in this.

I started few years back with motilal nasdaq, did sell a portion to reduce my average cost. The other two are one year old

If u have a demat ac think of etf instead of funds. Only my opinion.

My view is rbi may not increase the limit in view of the current inr depreciation.

I see this as a popularly stated reason for pursuing exposure to foreign assets.

What are the risks you’ve identified with exposure to such ETFs?

I ask because, one risk that i keep seeing in several discussions these days is -

these ETFs have increasingly gotten to have concentrated positions (60%+)

in a few limited stocks/companies (mostly Tech).

So, diversification from INR, yes,

but worth it at the risk of concentration into <10 individual stocks/companies in the US ?

Also, has anyone considered any other alternatives to hedge against INR-USD depreciation without exposing oneself to a handful of companies like these ETFs do?

Any other challenges/risks involved compared to investing in these ETFs? if yes, what?

Faang is extremely tech concentrated approx 10 constituents. Also nasdaq is mainly tech driven but 100 constituents.

S&p top 50 is well diversified. Constituents include 50 stocks out of 500. This including banks and my fav berkshire hathaway as well.

Incremental monies are going into

Currency depn is one of the factor but not the critical one.

The constituents of all three overlap but ok by me. The names are well know company and if available in india would in any case bought the same

In addition to constituents growth the currency depn adds on to the returns for indian investors.

The risk is if and when rbi increase the limit the price will fall by 15 odd percent to the present inav.

15 percent is my calculation may not be accurate.

As a hedge I have only few options gold or these funds to invest or open usd ac at gift city. Not sure it is open for retail customers. And my choice is these funds.

One other option is indian companies where sales revenue is in usd like tcs. This is a indirect hedge i guess

Right. Then you don’t necessarily see this concentration as a negative risk. Got it.

I would like to take this opportunity to highlight that

since these ETFs are tracking market-cap weighted indices,

investing say 100 rupees uniformly across these 3 ETFs

is effectively investing >65 rupees in ~10 tech companies

and the leftover is spread across some other ~90 companies

( <50p out of 100 INR invested in most of these other companies).

Here's why...

Yes. MIRAE ASSET NYSE FANG+ ETF tracks the NYSE-FAANG+ index which is 100% tech (10 tech stocks).

True. However these same FAANG+ companies make-up ~50-60% of these 2 indices as well.

A concentration risk associated with the current market-cap weighted indices in the US

as FAANG+ has grown so dominant in terms of market-cap/evaluations.

Hmmm… Would i be correct to guess that

investing without using a US-brokerage is still an additional constraint ?

If yes, then that can explain the limited options being considered,

i.e. not considering USD-denominated sovereign bonds or debt-funds.

Retail access to International USD-denominated Sovereign Treasury bills is common available in India these days. The easiest approach for resident Indians that i am aware of is through a regulated broker operating in the US.

Here’s a discussion thread containing experiences with few such brokers. (the sub-reddit has several such discussions on international investing.)

With all such brokers offering their respective websites/applications

for digital registration/on-boarding,

to perform all investments (one example)

to transfer funds digitally (one example),

for simple hassle-free investing (not trading), the differentiation ends-up being

how much one feels like trusting a broker

and their charges

IMHO, among the various brokers offering this, Charles Schwab is very similar to Zerodha with its no-marketing-sales-push, simpler design, and zero commission/brokerage offerings.

Some major aspects to be aware of (compared to investing domestically).

Foreign-exchange rates and currency-conversion charges

Some Indian banks charge 1-2% margin by default for nominal amounts / infrequent transfers and no prior significant relationship with the bank.

Most offer as low as 0.05% (Inter-Bank-Rate - 5p) margin on currency conversion upon negotiation depending on amount/frequency/relationship.

Taxation

TCS on LRS

TCS is NOT any additional tax-liability.

Rather it is upfront collection of a fraction of one’s outward remittance (under LRS).

One can claim tax-credits to the amount of TCS withheld, either against quarterly advance tax (if any) or while filing ITR at the end of the year.

Certain types of income attracts tax-withholding in the US (eg. Dividend income)

Such tax withheld, one gets to claim tax-credit on it in India (eg. while filing ITR)

If holding more than 60,000USD, estate-tax applicable on the US-domiciled assets upon death of the individual holding such foreign assets.

Tax Returns filing

Requires disclosure of foreign assets in one’s ITR.

Even assets simply held and not sold yet. (Unsold stocks/bods, Dividends/interest received)

Relevant schedules in ITR-2 for the year.

FA - disclose all foreign assets.

FSI - disclose any foreign-source income (if any)

TR - disclose any foreign tax withholding and claim tax-credits/relief (if any)

Form-67 - declaration/proofs for foreign tax withholding (if any).

While i personally believe it is easy to do all on this one’s own,

a consultation with a CA who is aware of one’s personal finances

can definitely help clarify these aspects and smooth the process.