No safe haven for bulls ![]() . Gold

. Gold ![]() , silver

, silver ![]() , stocks

, stocks ![]() you name it… It’s all going through massacre. Even debt

you name it… It’s all going through massacre. Even debt ![]() by virtue of being denominated in INR

by virtue of being denominated in INR ![]() erodes your capital’s real value and purchasing power of that capital

erodes your capital’s real value and purchasing power of that capital ![]() . Where would you invest to preserve your capital’s value?

. Where would you invest to preserve your capital’s value?

1 Like

Rate after inflation and taxes? And just INR depreciates 5-10% every year. If it doesn’t beat that, it still losses value.

Except the above then.

- Debt not denominated in INR.

- Other commodities.

- Real estate.

- …

Assuming you are looking to brainstorm investment ideas,

while we wait for folks to share their favorites,

an alternate approach to think of is -

Why?

Why do you prefer perserving capital value right now?

Did you have major expenses planned in the near future?

Does it make sense to prefer liquidity instead?

For the flexibility to quickly follow any positive trends in the near future (if any).

Do you expect to have the ability to identify trends reliably in the near future to make good use of such flexibility?

How much risk do you need to actually expose yourself to?

(are the additional returns due to additional risk even necessary for your personal finance targets)

1 Like

No one likes their things stolen.

Of course. Liquidity+ returns just for capital value preservation not even for excess returns. If you just keep cash under the pillow, it’ll lose it’s value real fast. In essence, the government and the world is stealing from under my pillow without me realizing. The objective is to prevent that.

Yes. Still, there are many hurdles put by RBI and government to prevent that and they come with their own risks.

2 Likes

![]() Note: If you are negatively affected by the current market conditions beyond your most conservative estimates, then probably the following might trigger you further.

Note: If you are negatively affected by the current market conditions beyond your most conservative estimates, then probably the following might trigger you further.

Please do NOT read the below if you are already in a heightened state of emotion.

Yes, i am fine. I am not going to engage in a flame-war...

No one is stealing anyone’s capital.

If you lost anything, that is because you risked it. Atleast own up to it.

Sure, you will feel betrayed if certain assumptions that you held true when undertaking the risk, are no longer true. But, ask yourself whether making those assumptions was justified.

Use this opportunity to improve your risk management.

IMHO, this entitlement that one is owed something is a potentially problematic mindset

when owning an asset and participating in schemes that are

not in one’s circles of control and influence, but in one’s circle of concern,

Doing so is expected to lead to feelings of helplessness/frustration,

and likely sub-optimal financial decisions if operating on emotions.

So, evaluate them and pursue the approach with highest risk-adjusted returns.

With one caveat - Do you know if the additional returns are even going to matter to you? ![]()

If you are intending to do this for your personal finances,

please do consider spending time estimating how much more is enough

to then work backwards from it,

to reduce the level of risk necessary to achieve the target value,

and increase the likelihood of achieving it.

I have implemented this strategy for my parents’ portfolio:

They’re still sitting on massive gains from gold, so the current dip is not an issue. ![]()

My investment portfolio OTOH is all in on equities, so it’s hit bad, but these are paper losses and I have no plans to book it. ![]()

Given a long enough timeframe Indian equities will outperform even gold, that is my long term view and hasn’t changed. I’m optimizing for returns. ![]()

In the short term, I have uncorrelated trading returns and some debt to tide me over! ![]()

Still it hurts that even though trading returns were stellar ![]() this year I have lost paper money to equity correction, inflation, and rupee depreciation. Just the latter two comes out to about 10% for last 12 months which is crazy! Even if long term equity gives 12% CAGR, my gains would be only a measly 2%!

this year I have lost paper money to equity correction, inflation, and rupee depreciation. Just the latter two comes out to about 10% for last 12 months which is crazy! Even if long term equity gives 12% CAGR, my gains would be only a measly 2%! ![]()

2 Likes

FWIW, here’s a potentially relevant recent discussion that talks about

reduced magnitude of drawdowns of multi-asset funds

that actively manage holdings across multiple asset-classes.

Worth monitoring how such funds perform during the current extremely volatile period.

1 Like

Fixed Deposits

Not really. I mean if you do want to take that view, there’s something called inherited risk. Just by being born in India and being a resident, you’re forced to invest in a risky asset called INR with no real way out. And that asset is regularly stolen by the government by inflation. You should look at INR as a equity share, a share that you’re forced to invest in and that which will give negative returns yearly.

GPT puts it aptly:

Inflation can be seen as a way for governments to reduce the real value of their debt, effectively “stealing” purchasing power from citizens. This occurs because inflation erodes the value of money, allowing governments to pay back loans with less valuable dollars, which can disproportionately affect those with fixed incomes or savings

2 Likes

Someone once said something very releavnt to this scenario -

it’s really about managing emotions.

If one needs to tap the value in the near future,

then holding it in the form of a volatile asset is a sub-optimal decision.

Best to move to stabler/liquid assets or even cash.

The perceived loss over time to inflation is not a concern here as one intends to spend this in the near future anyway.

On the other hand,

if one has no immediate need to tap the value / spend it,

then adopting a maximin strategy right now is sub-optimal.

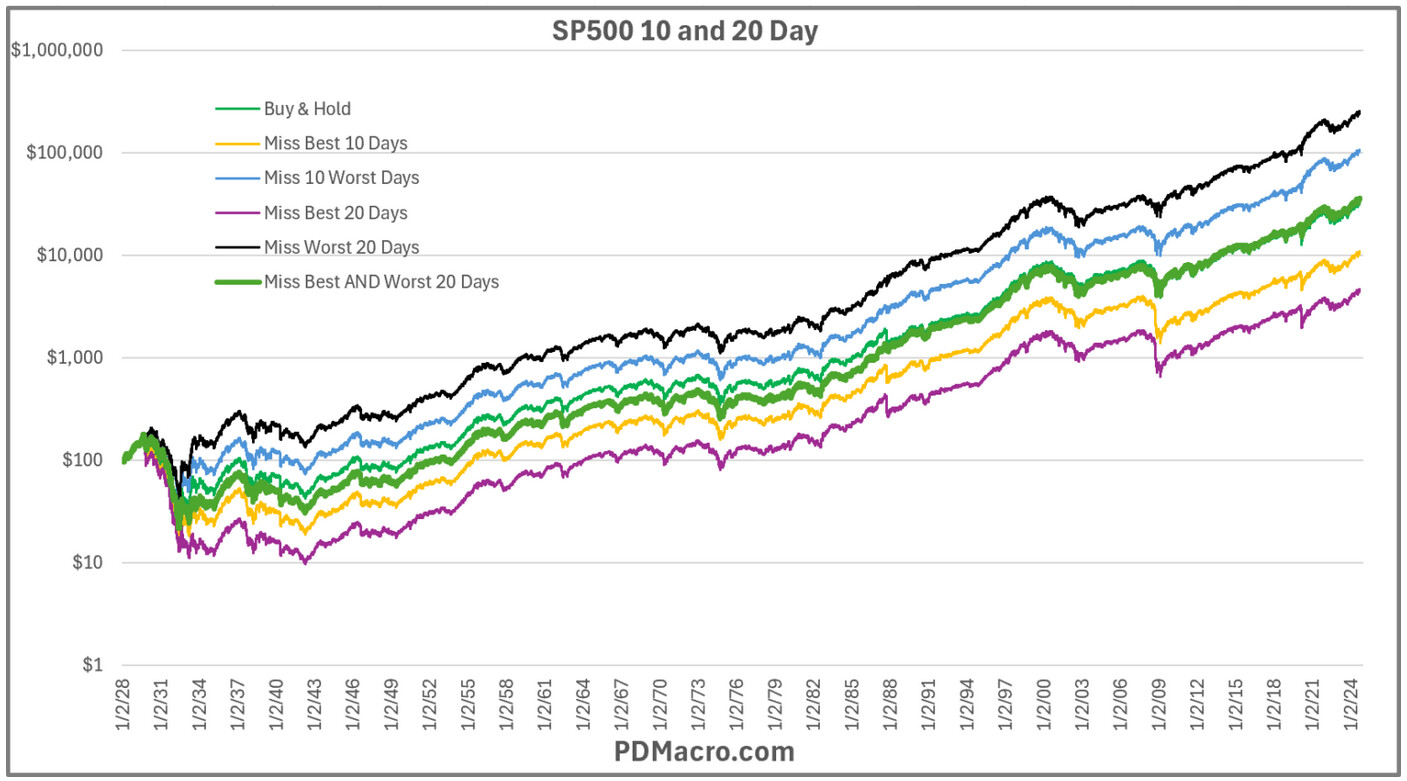

One reason is that the best days and worst days in the market occur close to each other.

While one may try to avoid exposure to the volatile assets in the markets during the worst days, by doing so, one almost definitely ends-up also unable to be exposed to the volatile assets on the best days (closely clustered to worst days), which effectively provide returns close to a buy and hold approach.

Note1: The Y-axis is non-linear, logarithmic scale.

Note2: Based on historical behaviour of close clustering of best and worst days.

[ Source ]

If one has already been exposed to

a volatile asset in the market during a “worst day”,

then by liquidating the volatile asset,

- subsequently potential best-case outcome

- manage to invest back in time to get exposure to the subsequent “best day”.

- achieve returns similar to a buy-and-hold approach.

- subsequently potential worst-case outcome

- miss to invest back in time to get exposure to the the subsequent “best day”.

- achieve returns worse than a buy-and-hold approach.

Basically, significant potential-downside and no/limited potential up-side.

So, not a good choice to liquidate unless one has reasons to believe that

one can accurately time one’s re-entry into the volatile asset in future.

(In general, unlikely).

The following bit from an earlier post in this topic-thread,

attempts to state the above in a very brief/concise manner.

Not sure whether the concise bit gets the point across.

If it didn’t, hopefully this longer post helps. ![]()

1 Like

Absolutely. But, why stop at only risks?

In the same vein, let us also account for various inherited rewards as well. ![]()

So if someone is “stealing from us”, then someone is also “gifting to us”.

For now, i would like to avoid the inherited-rewards aspect

as that inevitably leads to the “Are the rewards worth the inherited risk?” angle,

and i do not think there is a general consensus on the value of the rewards,

due to different people with varying value-systems, valuing the rewards differently.

If the focus of the question in the title of this topic-post,

is to highlight the “inherent risk” of INR.

That is true irrespective of the market condition bull/bear.

And putting together the 2 constraints -

- Looking for Debt (as a bear market)

- Looking to avoid INR (due to inherent risk)

the obvious solution is

On the topic of preserving or maximizing “real value”,

it is essentially looking to preserve/maximize future cash-flows,

Something discussed in this topic-thread, starting from…

So, focusing on the inherited-risk part,

for most folks in this country,

neither of these are in one’s circle of control or even influence.

except for an abstract/coarse/slow-moving/limited “lever to pull” once in a while - voting.

By spending time exploring/modelling these inherited-risks,

is there something one would do differently?

@BB789 If yes, what?

If not, (which is what i believe)

then given a limited amount of time/mind-space/patience that one can invest,

why invest it in topics that can provide no additional returns / minimal returns?

Let’s spend time/mind-space/patience on topics

where one can impact the outcome significantly

by taking a better decision.

PS - Anything to do differently knowing one's 'inherited risks' ?

By spending time exploring/modelling these inherited-risks,

is there something one would do differently?

Over the years, having spent more time thinking about this than i would like to admit,

all responses that i could come-up with, i was able to dismiss them with a -

“Well, one should be doing that irrespective of the “inherited-risk”.

i.e. not something one would do differently.”

So, curious if there are indeed any such implications…

Not going against this, but this made me remember a podcast. I have forgotten it and will go through it again in future, but MF often talk of staying in the market all the time, which isnt bad but is also in their interests.

This guy had some ideas

Time the market, not to ensure that you are in for the best days but to ensure that you are out for the worst days. Research has shown the best and worst days of the market are usually in close proximity to each other and if you end up missing both the best and the worst days your returns are far better than just being in the market all the time.

Not sure how it sets up his investing to miss most of the best and worst days.

2 Likes