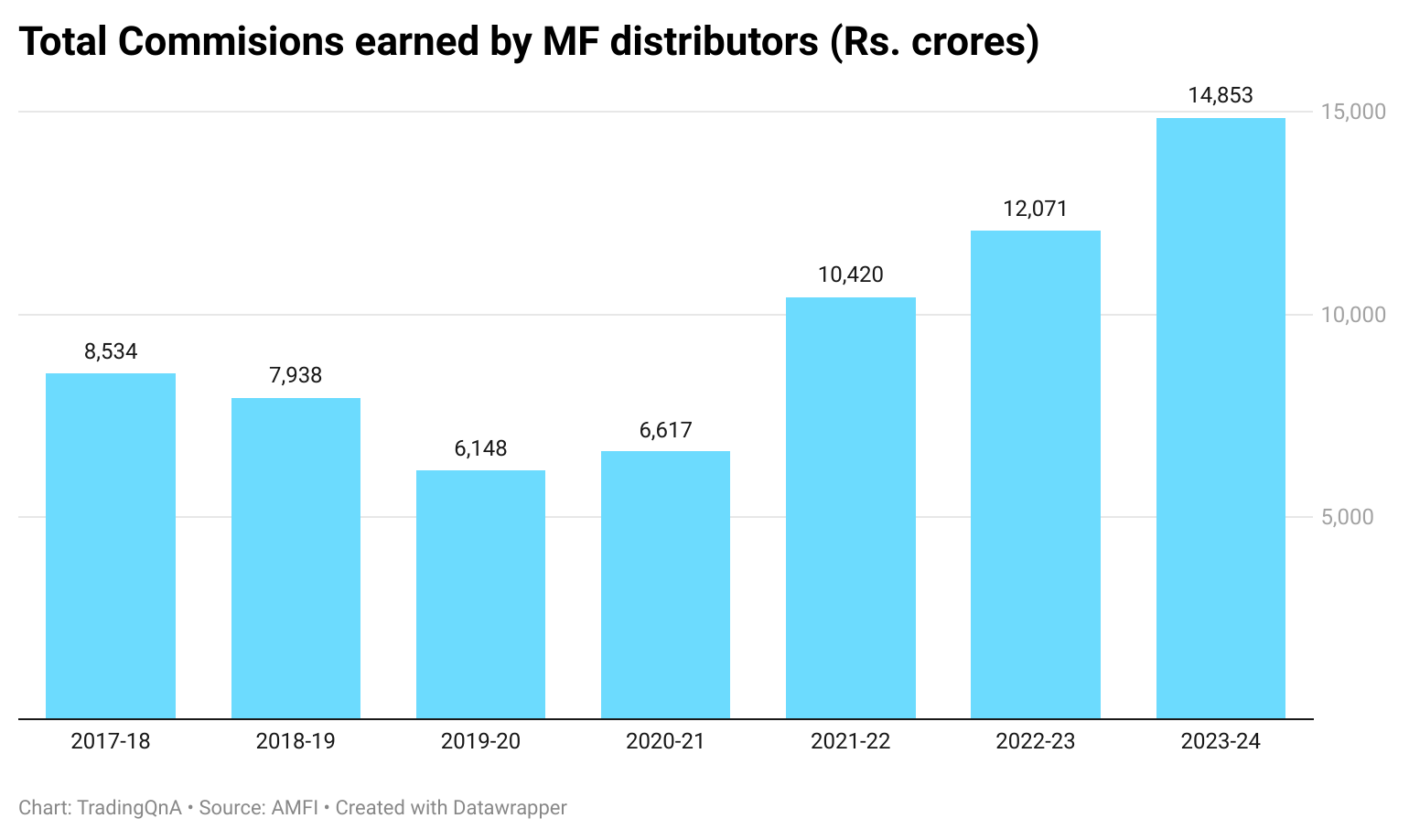

Every year, AMFI (Association of Mutual Funds in India), releases a report on commissions earned by mutual fund distributors. In the financial year 2023-24, the commissions earned by mutual distributors increased to Rs. 14,853 crores, a growth of ~23% year-over-year.

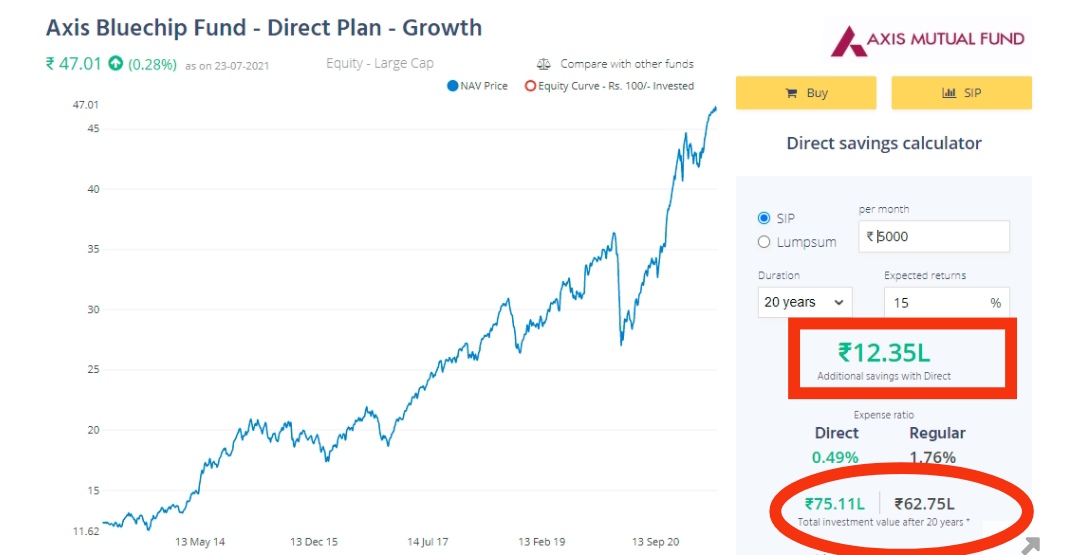

When you invest in mutual funds, you can choose between regular and direct plans. If you opt for regular plans, you have to pay commissions, which can be as high as 1%, charged every year on the invested amount, as long as you’re invested.

If you opt for direct plans, you have to pay no commissions. Btw, on Coin, we offer zero commission direct mutual funds. ![]()

Many investors think that 1% makes no difference and opt for regular plans instead of direct ones. It may not make a difference in the short term, but it surely does in the longer term. Commissions compound over time, the more your corpus grows, the more you pay in commissions. If you’re a DIY investor, it makes no sense to invest in regular plans.

It is important to keep the costs of your investments low. Costs are the biggest drags in the performance of your investments in the long run.

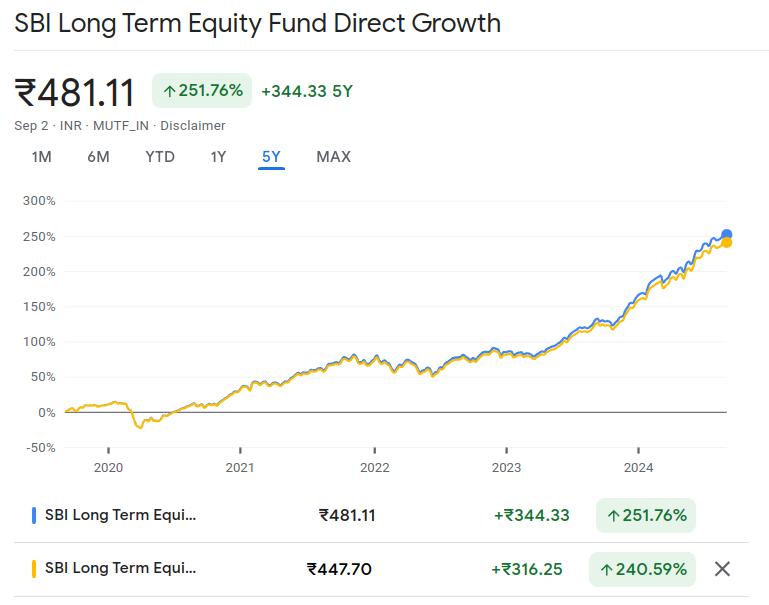

Here’s an example of the performance of direct (blue line) and regular (yellow line) plans of the SBI long-term equity fund over the last 5-years. The direct plan has outperformed the regular plan by ~11%.

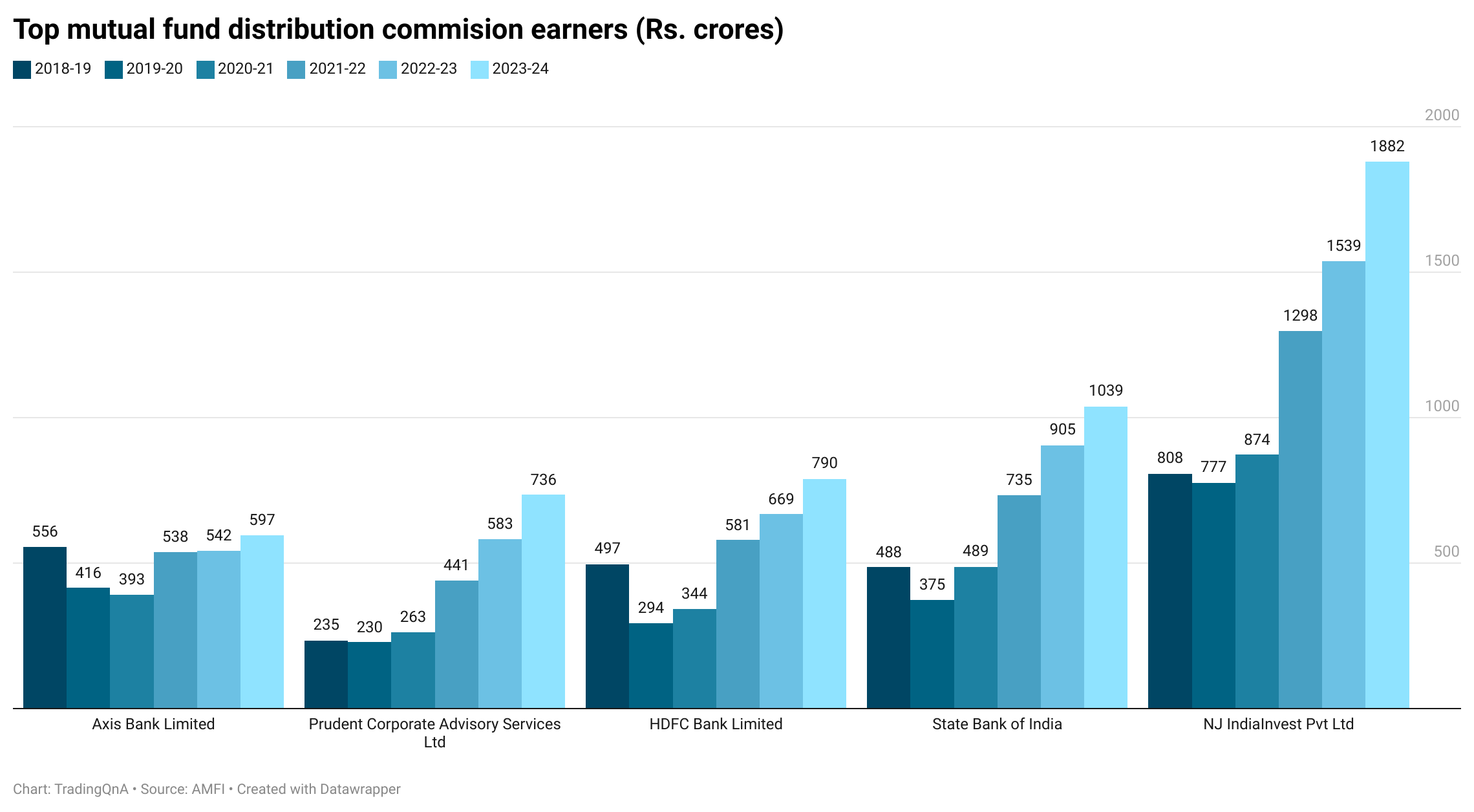

Commissions earned by top distributors.

Commissions earned by top 20 distributors (Rs. crores).

| NJ IndiaInvest Pvt Ltd | 1,881.81 | 1,538.98 |

|---|---|---|

| State Bank of India | 1,039.33 | 905.46 |

| HDFC Bank Limited | 790.31 | 669.27 |

| Prudent Corporate Advisory Services Ltd | 736.24 | 583.04 |

| Axis Bank Limited | 596.62 | 542.25 |

| ICICI Securities Limited | 521.38 | 453.63 |

| ICICI Bank Limited | 399.90 | 397.82 |

| Kotak Mahindra Bank Limited | 324.48 | 297.28 |

| ANAND RATHI WEALTH LIMITED | 291.21 | 212.79 |

| Hongkong & Shanghai Banking Corporation Ltd. | 168.63 | 135.49 |

| 360 ONE DISTRIBUTION SERVICES LTD | 147.47 | 123.64 |

| Standard Chartered Bank | 140.44 | 120.95 |

| Julius Baer Wealth Advisors (India) Private Limited | 139.27 | 111.10 |

| HDFC Securities Ltd | 127.05 | 96.69 |

| Bank Of Baroda | 123.58 | 99.82 |

| Bajaj Capital Ltd. | 116.95 | 102.40 |

| Geojit Financial Services Ltd | 94.90 | 81.72 |

| JM Financial Services Limited | 89.08 | 73.68 |

| Wealth India Financial Services Pvt Ltd | 86.24 | 75.80 |

If you are new to investing in mutual funds and all of this seems gibberish, Don’t worry, you can learn all about investing in mutual funds on Varsity: