So yeah, the new margin framework finally is going to be applicable from June 1st (as per this circular). Check this post to read about the new margin framework:

We have been getting many requests asking us for some sample calculations on what the new margins will be when trading F&O.

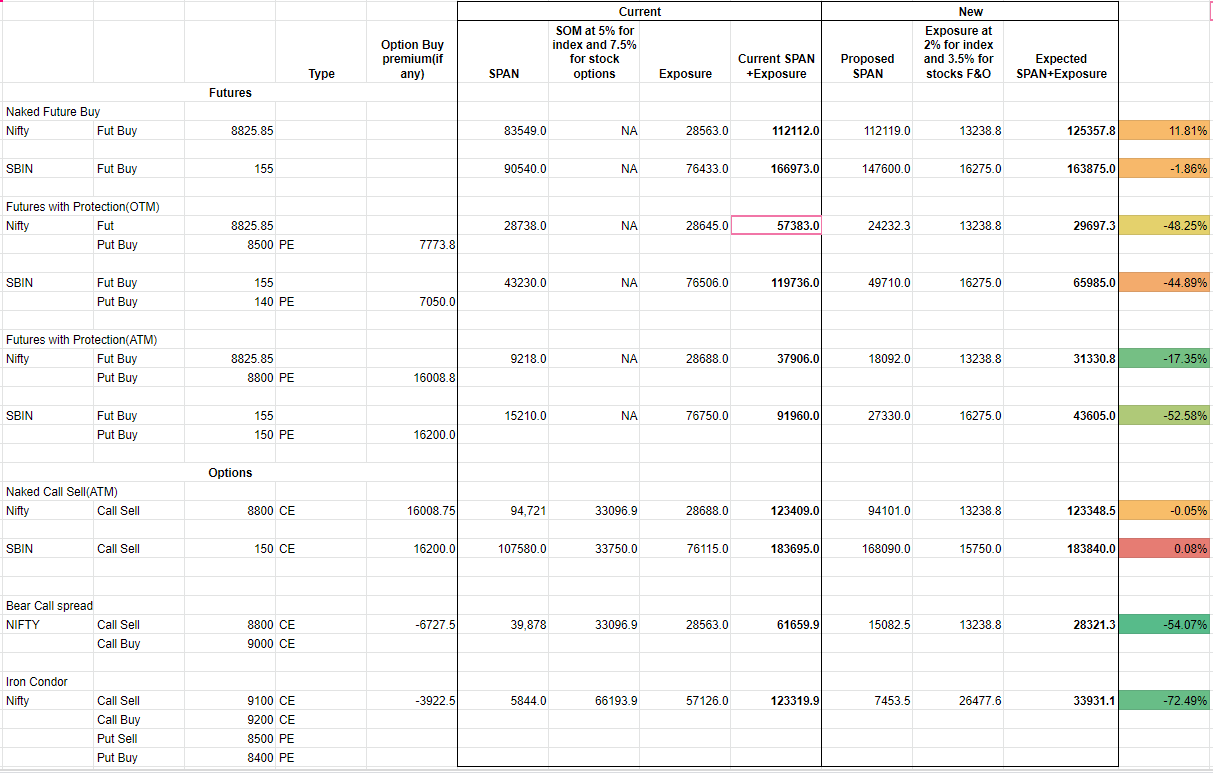

Here it is: Check this document if the below image isn’t clear.

Margin required is relatively the same for naked F&O positions.

Margin required for positions that have limited risk drops by up to a whopping 70%.

Price scan range is now 6 Sigma vs earlier 3.5 Sigma (both for stock and index F&O contracts). This means that if volatility picks up, margin increase will be higher than before for naked positions. This is the reason the Nifty futures margin is around 12% higher due to current increased volatility in the markets.

We will try putting out a new margin calculator soon, so you can try out the margin requirements for various strategies yourself.

Clearly this benefits people who trade spreads with limited risk significantly in terms of lower margin requirements. Here is once again, hoping that this new margin framework is the catalyst for the evolution of a new breed of low-risk option traders in India.

Updated 23rd May: NSE had a presentation on the new margin framework. Checkthis presentation, it has good info.

Naked options are always risky with or without margin framework. This new margin framework will encourage more traders to hedge and thus eventually rise in liquidity in options

I somewhat disagree for the margin of Iron condor. Why would extreme loss margin of 2% be blocked for both the sides when the risk is on any one side? @nithin@siva-reddy

Exposure margin is blocked on both sides. While SPAN calculates the net risk of the portfolio, exposure margin is levied on each leg of the position(2 short legs in this case).

Both SPAN and Exposure margins are subject to volatility of the stock. Since Covid-19, markets have been volatile leading to higher margins. If volatility comes down back to normal, so will margins.

Naked OTM Option selling will have same margin as they are now?

Also hoping that new margin calculator will include weekly option expiry for nify, banknifty so that we can figure out margins required for shorting the same.

Hey,

if you are adding few example then add one for the strategy shared in learnapp by jegan.

Sell Monthly strangle & Buy weekly strangle (Same strikes)

!. -8500PE Monthly

2. +8500PE weekly

3. -9500 CE Monthly

4. +9500 CE weekly

Please tell me if i am correct or not

Nifty bear call spread for 100 point difference margin is 21000

and for bank nifty 500 point difference margin is 18000 @MohammedFaisal