A complete bolt from the blue for the mutual funds sector.

As per many reports, Starting April 1st, 2023, Mutual fund investments having not more than 35% invested in equity shares of an Indian co (every other MF excluding equity oriented MF) to be deemed short-term capital gains

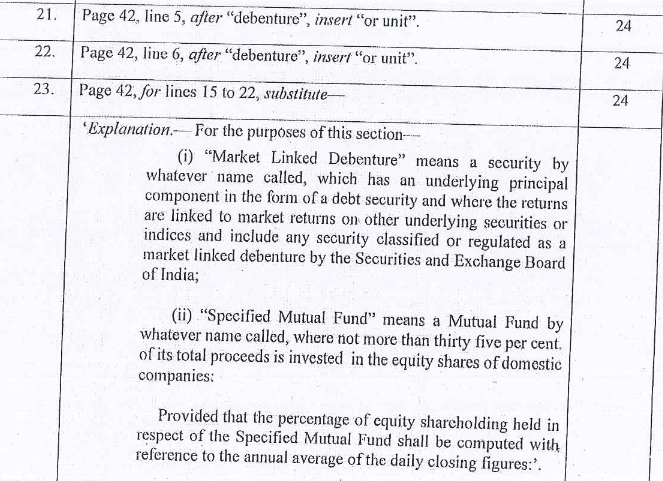

That means the indexation benefit is lost for all the Debt/Gold / International funds / FoFs going forward once the amendments are passed in the parliament later today.

If all gains from debt mutual fund schemes are treated as short-term, they would be taxed as per slab rate. So, individuals in the highest tax bracket would pay a tax of 30% on such gains.

“I hope the proposed change in the Finance Bill to remove LTCG with indexation status on debt funds is reviewed. Financialisation is just happening in India, and a vibrant corporate bond market needs a strong debt MF ecosystem,” said Radhika Gupta, managing director and chief executive officer at Edelweiss Mutual Fund, in a tweet. “The success of a programme like Bharat Bond and target maturity funds in the last year was just the beginning of what could have been a lot of innovation in the bond category.”

On the face of it, this is bit strange. What is expected that bring common treatment to capital gain taxes across different asset classes to simplify taxation. This rationalization was not tabled during budget and now all gains from debt mutual fund schemes are treated as short-term.

It may be possible that in future capital gain concept it self is removed… and everything is brought under slab rate.

Big loss for the bond markets as it’s still very much under-penetrated. AUM shanti.

IMO, Govt. seems to want people to shift from a saving mindset to a spending/consuming one. A lot of the changes, including the new tax regime, seem to suggest that.

On a personal level, I had a decent chunk of Liquid Funds reaching the 3-year mark in May, and considering the rates are expected to peak out maybe this year, had thought of redeeming & shifting it to Gilt Funds. Now, am not so sure…

Yeah seems that way. We had multiple years of negative real interest rates, only now we have slightly positive. Inflation takes away a major part of the returns. And now to tax on returns that were taken away from inflation basically makes real rates even lower or negative. Either you keep compounding whatever little real returns you get or just spend it now.

Makes it even tougher for old retired people who had decent savings and decent enough quality of life to exceed 7L. If they don’t manage things well ( god knows how to do that without large proportion in volatile equity), a decade or two will quickly degrade their finances.

but short term gains are generally not taxed at income bracket right. So I am trying to understand what made him to come to that conclusion ( or “assumption”).

yeah, it seems fairness does matter in taxation, only political feasibility. So there is not talk of closing loopholes around agriculture and the like. People are happy if 5L limit becomes 7L but do not notice the impact of inflation over all of these years.

We have high taxation in India, unless you can work with loopholes. And in return state of air, water, healthcare, education - the basics - for large portion of the country is self evident. Sorry for ranting.

Now this is dead end for manual rebalancing in different asset classes.

DIY retirement planners are in dire need of NPS Tier2 like mutual fund which invests passively in ( index of )different asset classes and allow end use to control the allocation percentage.

Zerodha… are you listening? Pls come up with target dated retirement fund.

I guess some may not excel at one thing, for any reason, by choice one among them, and may have some level of expertise regarding many things.

Happens in the markets too. One need not necessarily excel at one particular aspect of the markets but is reasonably good at at a few things that pertain to the market and can still be profitable.

I do that too and don’t plan to change anything. CG is on redemption and i wont redeem. Gains will accumulate and you get more margin. Was going to do the same earlier as well so nothing changed other than taxation impact whenever i decide to redeem. It sucks a bit but better than any interest bearing debt which has immediate taxation impact.