This is about point (I) in Mr Nagpal’s twitter thread about FM’s rationale: Will only re-look at international funds/ gold funds categories if AMFI or Industry represents to the govt

Pls don’t get your hopes up guys…I wouldn’t expect anything to come out of this even if the industry represents… They have already mentioned in the previous point that these categories are collateral damage but their AUM is too small. The MF lobby is considered powerful but despite repeated representations they have failed to get a level playing field wrt NPS or ULIPs (if you switch ULIPs or change plan sponsors for NPS tier1, then you don’t have to pay capital gains tax). But this is not the case wrt MFs - say if you want to switch from regular to direct plan of same scheme or dividend to growth plan or even two schemes of the same fund house, you have to pay capital gains tax since it is regarded as sale transaction under current I-T rules. This is an inherent taxation flaw.

Imagine NPS & ULIPs offering flexibility without invoking tax liability while MFs don’t offer this? I am bringing this up here especially because the FM mandarins are talking about having a level-playing field. What level-playing field ya?! So many years have passed but the ‘powerful’ MF lobby hasn’t been able to get the FM to remove this flaw & their pleas have fallen on deaf ears.

[side note: i know i know ULIPs are tulips & never invest in ULIPs]

@ShubhS9@Quicko@nithin

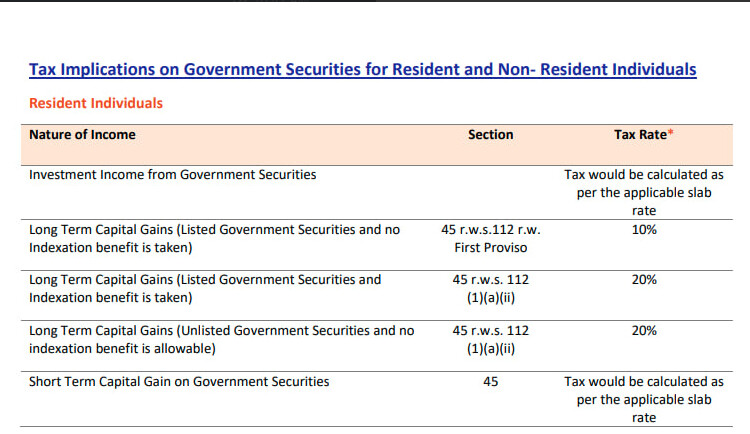

Have these new rule changes … impacted Gsecs (long-duration central gov bonds) too?

Or we can still avail of the LTCG as per below on them

Looks like so , lol. Or Banks are stressed needs deposits. Today , UPI is also no longer free. They introduced new charges . With so many fintech disruptions, Banks are loosing free avenues or existing business model might not sustain . In US, I read people are getting T-bills and GSEC to invest in no longer wanted to put in banks who provide them 0%

Yes, we can definitely expect new offerings with the ratio tweaked towards equities/ derivatives so as to use the new taxation law changes favourably… I would expect large AMCs to jump at the opportunity to launch new pdts.

btw, the taxation changes have claimed its first wicket already- the new Quant NFO - Dynamic Asset Allocation Fund was forced to tweak its structure from Debt to Equity.

Quant Dynamic Asset Allocation Fund was initially floated as a BAF that would dynamically switch between equities and debt assets based on a risk-on, risk-off environment. The twist was that unlike other schemes in the category, QDAAF would not necessarily have had a minimum 65% equity exposure at any time.

@Quicko … Any insight about NPS Tier 2 account tax applicability ?. Given enormous flexibility to adjust asset classes, would be interested in knowing how it will be taxed under new tax era. .

As NPS is a pension scheme, one cannot withdraw before the age of 60 or retirement. NPS tier II are voluntary accounts, hence there is no limit on withdrawal.

Read about the NPS Withdrawal Process.

All withdrawals from the Tier II account are taxable at the investor’s income tax slab rate. Withdrawals within a year attract a short-term capital gain tax.