Would like to know about the taxability of gains earned from NPS Tier II account also is it really worth putting money in Tier 2 account. Is it safe as Fixed Deposit?

Tier II is an add-on account which provides the flexibility to invest and withdraw anytime. The official documents do not explicitly mention about the taxation of the withdrawn amount and, thus, consider that any appreciation (equity or debt) will be added to your taxable income

Read more at:

Of course NPS is safer but can’t compare it with fixed deposits as returns are dependent on underlying instruments you have chosen. I mean returns are variable unlike in fixed deposit. Quicko may reply on tax part.

Hi Siva, Thanks for your reply, do you think LIC Tier II G type is the safest bet? I did some portfolio analysis, they have all long term government bonds in portfolio that too max 2-3 percent.

Need your analysis and opinion.

Are G-Secs inside the LIC fund safe - yes. Should you invest? That depends on your risk profile etc. Remember, the reason why Gilt funds have done well recently is because interest rates have fallen sharply. The returns won’t be so great in the rates rise. If you aren’t aware of the relationship between bonds and interest rated, I’d recommend you check out the debt funds module on Varsity:

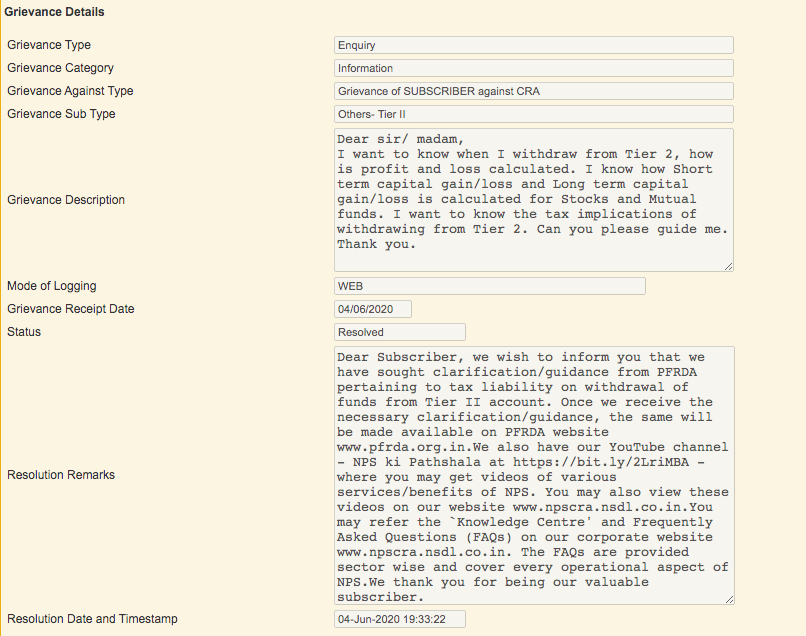

@Hum_Sa Back in June, I had asked the same question to NPS and I didn’t receive any concrete answer to this.

I then asked the finance and taxation team in my office but there too I didn’t receive a satisfying answer.

I don’t know where did I ask on the internet somewhere or either @quicko answered on this forum. I checked my activity but couldn’t find any trace of it. But the answer was NPS Tier 2 has 3 different components - ECG. E - Equity, C- Corporate Bonds and G - Govt bonds. In your NPS Tier 2 transaction statement, you can see the distribution between the E,C and G components.

So the Equity taxation rules would apply for redemption of Equity units. And the Corporate Bonds and Govt Bonds would be treated as Debt instruments. Quicko can confirm the same and correct me if I am wrong. While redeeming you can decide which units (Equity, Corporate Debt and Govt Securities) and how much you want to redeem.

BTW, NPS allows you to change scheme distribution and the Pension fund manager once a year. And FYI, it does not incur any tax liability. I had confirmed this with NPS. Back in March, I had switched my Pension fund manager and also reduced Corporate bonds and Govt Securities ratio while increased the Equity portion to the maximum allowed 75% to switch the NPS vehicle to 4th gear. Also, I had invested Rs 50,000 in Tier 1 as an additional tax saving contribution under 80CCD (1B). So NPS for me has been the best performing instrument for 2020.

2 Likes

This is really helpful. Thanks for your factful response and helping out. Me to starting utilizing the full tax benefits of NPS 1 via 50K and employer contri. But not also want to enter the Tier 2.

Prior to moving into Tier 2 just had lots of doubts and felt this would be the best forum.

The flexibility of moving from T2 to T1 and changing % allocation is really a good option.

Is it possible to change the fund manager online or is it a a physical process involving going to POP?

Really good point @Bhuvan. But couple of points, 1) in India rates will not go down further (USA and Europe are different). 2) Specific to LIC - G they have very long term G - Sec bonds with int rates of 9+ % . That will keep the return on G portfolio higher for long term. Only the new money needs to be invested at lower rates of 5 to 7 % and that too might be for 2/3 years post which inflation will push the rates up in India. Europse and USA yields will remain low and that would result in flow of foreign money to indian equities and debt instruments. Dollar going down will also help the money flow to India.

Doesn’t work that way ![]() Fund managers churn the portfolio across the yield curve to position themselves for interest rate changes. You can check out the monthly portfolios of the fund to get an idea.

Fund managers churn the portfolio across the yield curve to position themselves for interest rate changes. You can check out the monthly portfolios of the fund to get an idea.

Agreed. but frankly speaking, out of more then 5000 MF schemes many have performed so badly.

Do they provide Transaction statements of their MF schemes? Are they truly transparent?

Switching units from T2 to T1 may incur capital gains and thus tax liability, if I am not wrong. @Quicko please help.

100% online. On one of the menu you would find the option. Just remember only one PFM can be chosen for entire portfolio. You can’t be picky like you want T1 to be managed by HDFC and T2 by SBI. You can’t choose Equity managed by HDFC and Govt Securities by LIC. So no heterogeneous combination allowed as of now. Only blanket selection of a particular PFM. Once a year you are allowed to switch and rebalance portfolio and scheme percentage distribution without any tax liability.

@This is possible. I have different for T1 and T2

Also no tax on moving funds from T2 to T1

1 Like

Ok. Thanks for the information. I don’t know but when I had tried switching somehow it didn’t let me do so. There may be some fine print that I missed. Maybe. Regarding T2 to T1, technically it’s redeeming from T2 so capital gains and tax liability should apply. No? As I mentioned I am not sure about this and I may be wrong. Hence if @quicko is listening, he may confirm.

Looks like @Quicko is on a looooong weekend vacation.

Meanwhile, @Hum_Sa I suggest you also register for D-Remit to get same-day NAV for your NPS investments.

Just visit eNPS website and click on ‘National Pension System’ and then click on ‘Register for D-Remit’ and proceed further with the instructions on your screen. Once D-Remit feature is activated, it creates unique virtual bank accounts for your NPS Tier 1 and 2, which you have to add as a beneficiary in your bank account, and through netbanking/ mobile banking you can transfer funds to the virtual accounts before 9:30 am to get the same-day NAV.

Great thanks a lot for the advice. Will do it asap. I saw your thread on SGBs too. I feel spread the buying buy bonds from secondary market maturing at different dates. Best part is no tax on SGB gains provided gold moves up.

Silver - Do you think long term charts look good and what is the best option to do SIP in silver?

Yes. I do have a few SGB as I have mentioned in the thread (had invested in bulk 3 years back initially, and added few more just before covid, and then bought from the secondary market later) but I have invested in SGB while keeping in mind the Gold drawdowns, risk of low trade volume of the secondary market, and if gets sold in secondary market, it comes at a cost of a discounted price than the current market price of gold. Because of such risks attached, which all financial instruments have, I was against tagging it ‘the best’ universally. All I had mentioned was to make people aware of the pros and cons of SGB, the risks attached, and then let them make an informed decision.

Well, Silver contracts are available on MCX but I am not a trader. I do have some digital silver on Augment App, the only place I found where you can invest in Digital Silver. I had mentioned the costs attached to investing in digital silver on this thread. One thing about Silver is that its price is more volatile than Gold. And though there are many industrial usages of the metal (unlike Gold), Silver being a natural resource is limited and a significant amount of the metal is not recycled. Also, in some use cases many other metals like Platinum, etc have replaced silver, which was used earlier. So such risks make silver even more volatile in nature.

2 Likes

can we invest in platinum ?

Tanishq has been selling for a long time. ![]()

Hi @Hum_Sa,

Just like @rupeshmandal said, Tier 2 account of NPS invests in 4 different asset classes, the profit from the same should be taxed under the head capital gains.

Depending upon the holding period it is taxed as long term or short term capital gains.

However, on the transfer between NPS Tiers there is no clarification provided by the authorities on its taxability.

Here’s a read for your reference by the NSDL.

1 Like