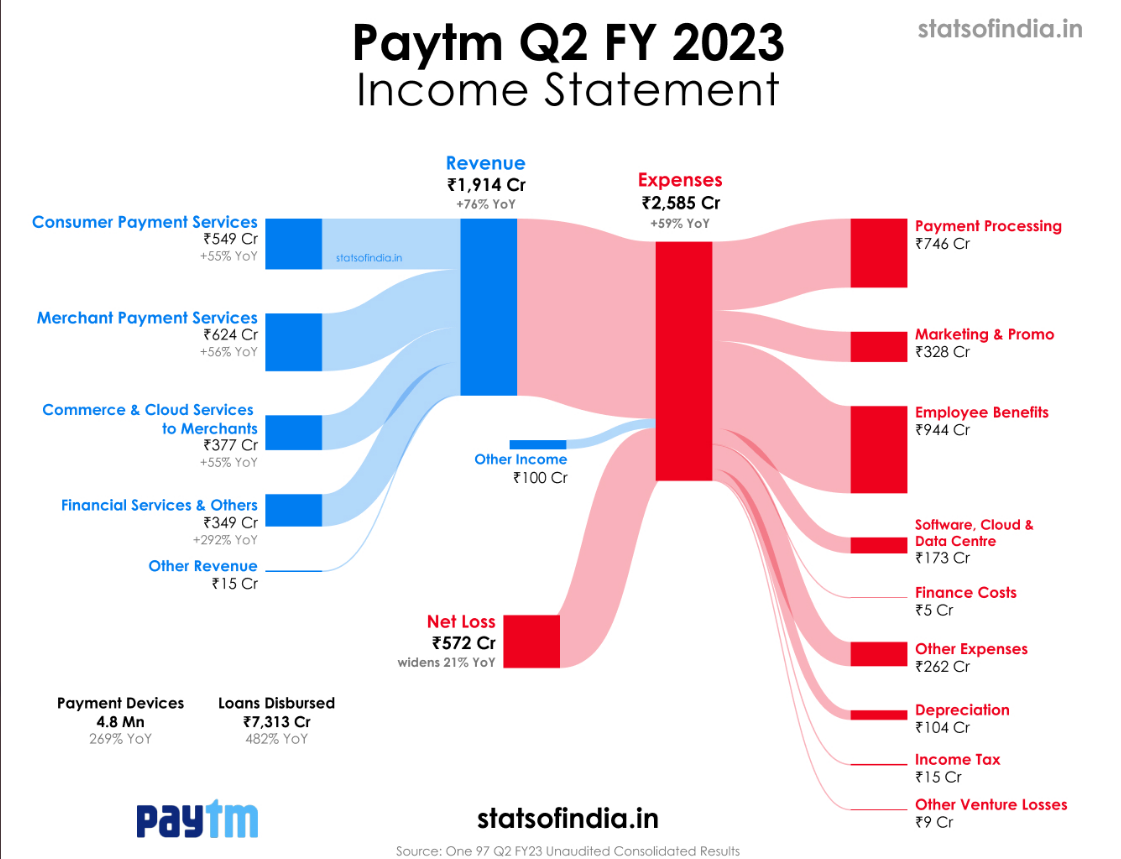

Paytm just announced its results for the second quarter of financial year 2023 and the company seems to be on the right track to become profitable operationally in the coming year. Here are some of the key highlights :

Source : Stats of India

Revenue is up 76% YoY to 1,914 Cr

This healthy growth was mainly on the back of:

- 58% YoY growth in cloud revenue, which is 14% of revenues, led by scale up in credit card distribution and traction in PAI cloud.

- 292% YoY growth in personal and merchant loans disbursements. Its contribution towards operating revenue now stands at 18% in Q2FY23 (vs 9% in FY22). Although optically, the growth looks extraordinary, the devil lies in the details as BNPL and personal loans form the >80% of their loan portfolio. That’s super risky.

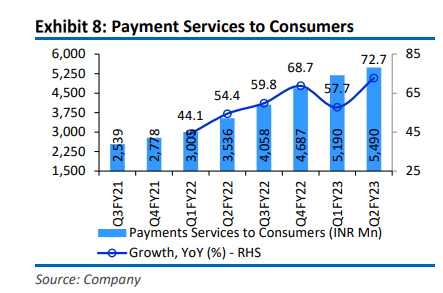

- 55% YoY growth in ‘payment service to consumers’ (29% of revenues) revenue based on platform fees and convenience fees from customers in certain use cases.

- Payment gateway business (32% of revenues) was the main growth driver with 56% on the back of higher Gross merchandise value (GMV) in online merchants, particularly e-commerce and growth in the number of device subscriptions.

Net loss widen 21% YoY but improves 12% QoQ to 572 Crore

-

Marketing and Promotional costs are 328 cr up 34% YoY due to promotional cashbacks and incentive expenses and other direct expenses.

-

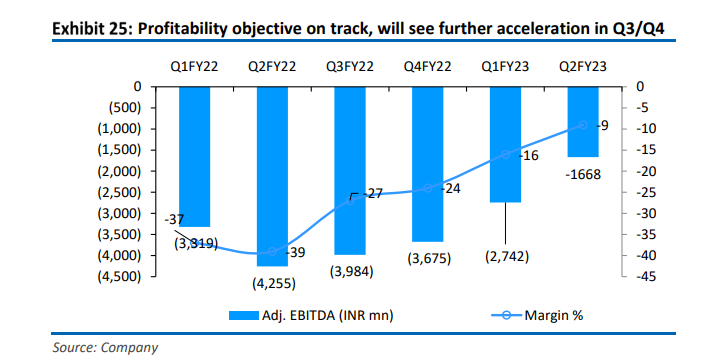

Excluding ESOP costs, EBITDA losses as a % of revenue are down from -38% to -9% (426 crore loss to 166 crore loss) , inching closer to breakeven and hitting their targets of turning EBITDA positive by September 2023.

Note: As ESOP costs don’t result in a cash outflow, it wouldn’t result in Cash flow loss to the business even if the company reports losses.

Source for charts : Dolat Analysis