As all Nifty 50 ETFs are benchmarked against the Nifty 50 Total Return Index (TRI), why is the NAV of the majority of these ETFs closer to the Nifty 50 Index instead of Nifty 50 TRI?

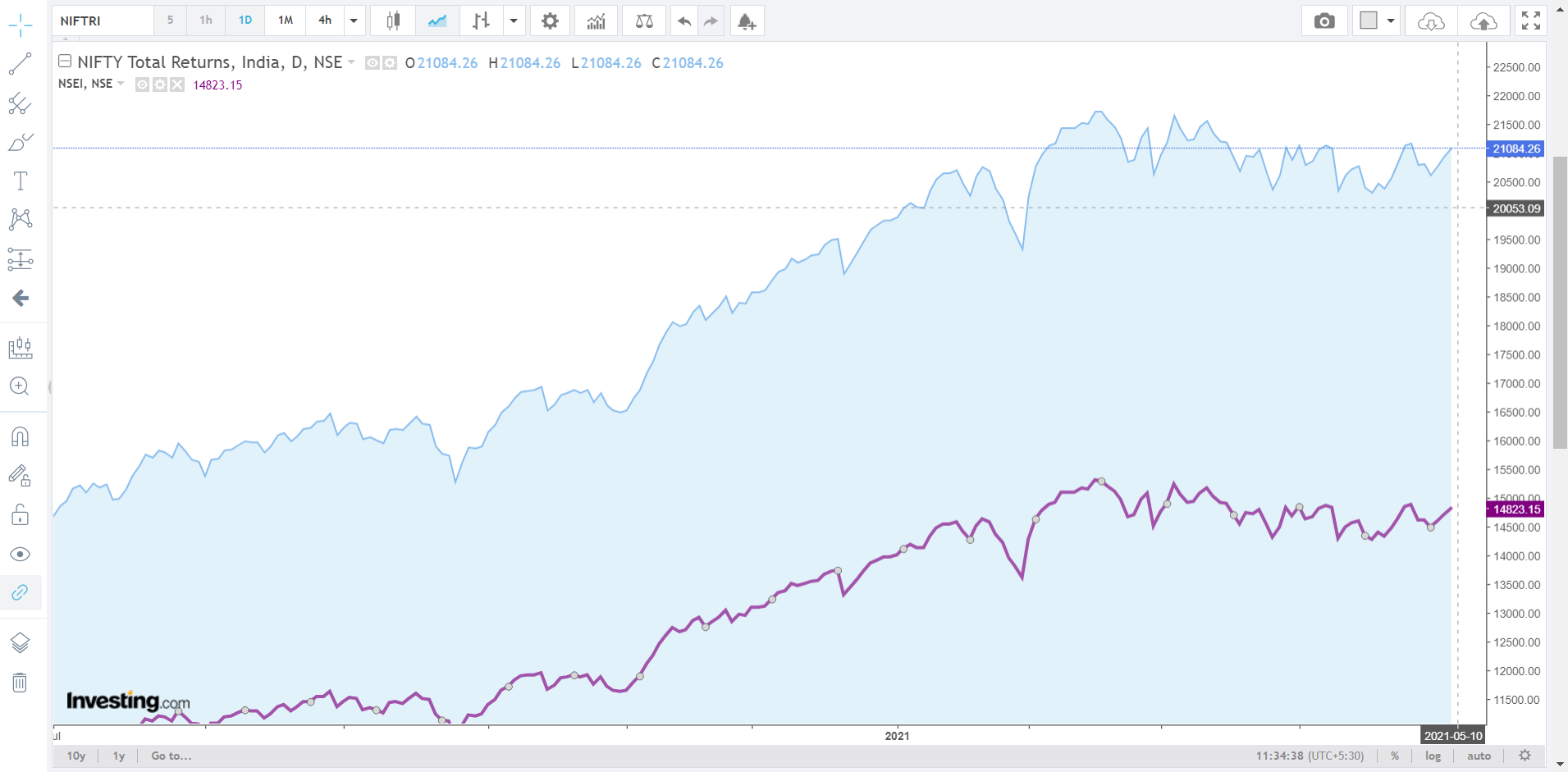

The reason I asked this question is because there is around 6000 point difference between the Nifty 50 TRI and Nifty 50 Index -

As most of the ETFs are around 1/100th the value of NIFTY, this would translate into a 60 point difference when comparing Nifty 50 TRI with Nifty 50 Index. Why is NAV of many of these ETFs around the range of 150-160 (that is closer to the Nifty 50 Index) instead of being around the range of 200-210 (which would be closer to the Nifty 50 TRI)?

1 Like

Hi,

Based on what I had understood from the computation methodology for Total Returns Index variant, it seems that the only difference when compared to the underlying index is that, in the case of TRI, the dividends paid are re-invested back into the index (similar to compounding).

The inference is that the weights of the constituents of TRI are the same as that of the underlying index. This can also be ascertained by comparing the %change in the indices, on days when no dividends were paid by the index constituents.

Since the weights are the same in the case of both indices, it makes sense that a newly launched ETF’s NAV will be closer (if not the same) to the underlying index rather than the TRI in its initial days. The divergence of the NAV from the underlying index kicks in, once the index constituents start paying dividend (which is reinvested in the case of ETF).

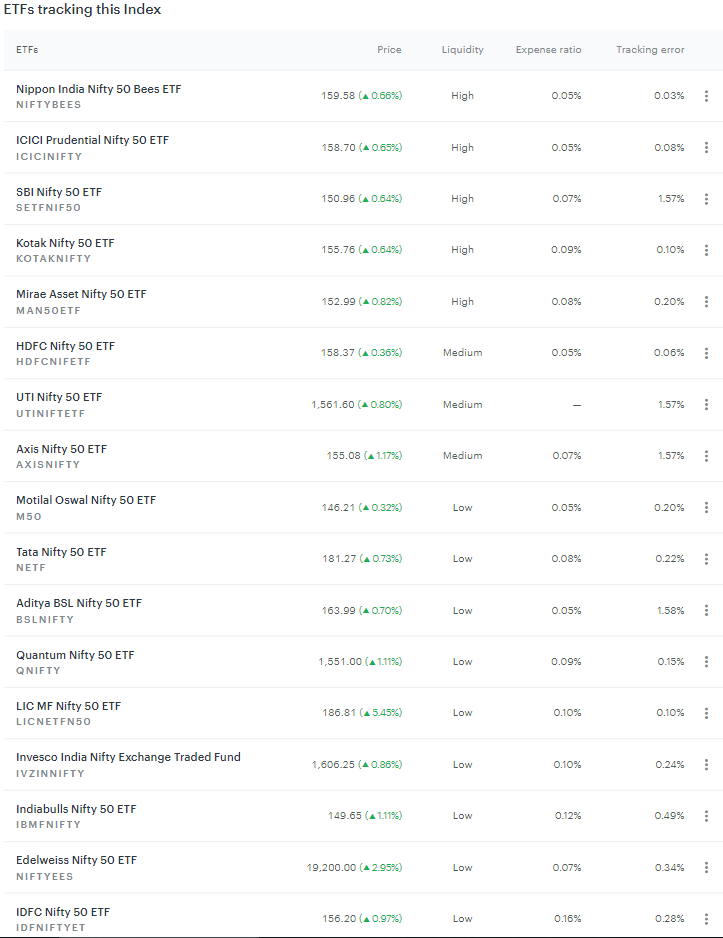

To test my assumption, I took the example of ICICI Prudential NIFTY ETF which was launched on 21-Mar-2013. The NAV as on the launch date was Rs. 56.61 (for reference, NIFTY50 closed at 5,658.75 on 21-Mar-2013). The NAV of the ETF was Rs. 159.04 as on 10-May-2021 (which would have been higher, if not for the dividend of Rs. 2.20 per unit paid by the fund on 29-Apr-2016) while NIFTY50 closed at 14,942.35.

This is to say that the NAV of the ETFs tend to diverge from the underlying index over time, provided the fund does not distribute any income/capital to the unitholders. However, it might seem that the NAV is closer to the underlying index rather than the TRI, because of the higher base of the TRI [both the ETF and the TRI move at more or less the same rate, but in absolute terms the change in TRI might seem higher due to the base effect].

1 Like

@Pratist @Prayag

So are we at a disadvantage when investing in a Nifty50 ETF compared to Nifty TRI or not ?

Hi,

There is no disadvantage, since all Index ETFs track the TR Index by default.

The index ETF and TRI is similar to cumulative debt instruments, in the sense, assume that, you have an FD which pays you a simple interest of X% p.a. and you also choose to reinvest the interest in the same FD. In this scenario, the simple returns is akin to the returns of NIFTY50 while the compounded returns is similar to the returns of NIFTY50 TRI / Index ETF.

The reason for

a) the ~6000 points difference between NIFTY50 and NIFTY50 TRI indices and

b) quantum of divergence between the NAV of index ETFs and NIFTY50 TRI [since the TRI had more time to “compound” when compared to the ETFs, to put in simple terms]

is also attributable to the compounding effect.

Also, in the case of ICICI Prudential NIFTY50 ETF (the example used earlier), the absolute change right from the time of inception (i.e., from 21-Mar-2013) was 193.05% as compared to 196.40% of NIFTY50 TRI. This is to say that, the Index ETFs do closely track the Total Return variant.

1 Like