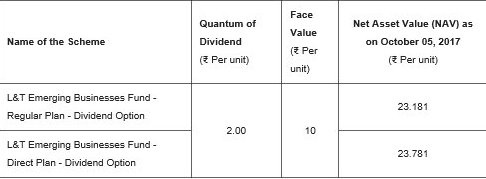

If we talk about Regular plan vs Direct plan of L&T Emerging business fund the NVAs are 23.18 and 23.78 respectively.

The difference between them is 0.6 which is almost 2.6% of Nav (0.6/23.18*100). ie for the Direct plan you have to pay 2.6% more than Regular plan all the time then How the Direct plan by Zerodha Coin is better than Regular plan??

Plz clear my doubt?

NAV of a scheme is derived from the summation of several factors or variables which is known as the profitability metric. It consists of the following variables :

(1) Interest income

(2) + Dividend income

(3) + Realized capital gains

(4) + Valuation gains

(5) – Realized capital losses

(6) – Valuation losses

(7) – Scheme expenses

As you can see the 7th variable which is the scheme expenses is a subtraction so basically the NAV would be lesser if this is higher. The expense ration is nothing but the scheme expenses. The expense ratio is generally denoted as a percentage which is specified as per annum. For the calculation of the NAV, the scheme expense is calculated and deducted on daily basis.

Now, for a regular plan of a particular mutual fund scheme the expense ratio is higher than that of a direct plan of the same scheme which means that the scheme expenses is higher for a regular plan. Thus, the NAV of a direct plan will always be higher than that of a regular plan. This means that the returns generated for a direct plan is essentially much higher than that of a regular plan.

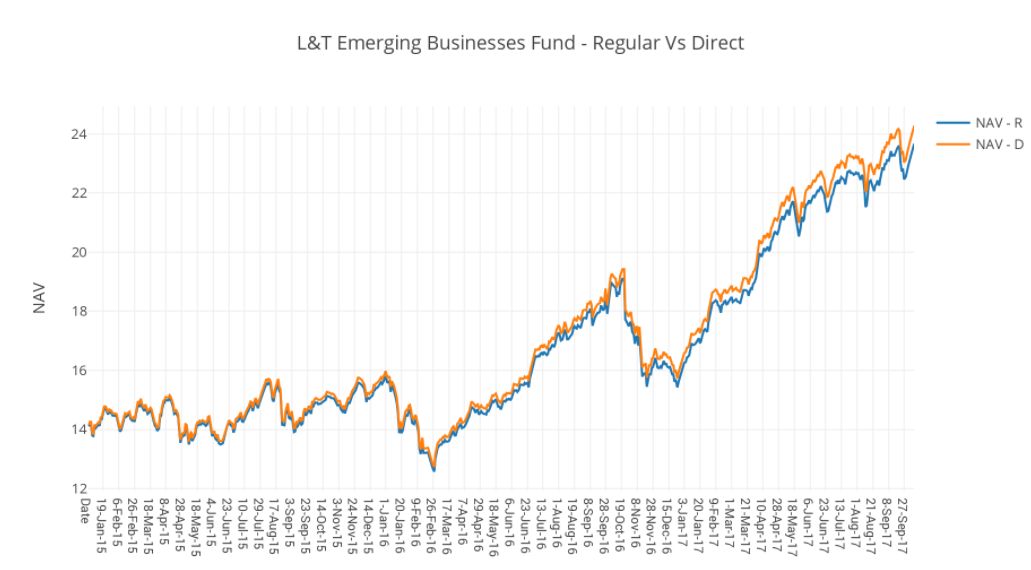

Below is a graph which shows the difference in the NAVs of a direct plan and regular plan of L&T India Emerging Business Fund. The NAV shown in the figure for a particular month is the average value of daily NAVs released for that particular month. The orange line represents the NAV of direct plan and the blue line represents the NAV of a regular plan. You can observe that the lines are slightly overlapping each other from the month of January 2015 and there is a huge divergence in the month September 2017. This is because the AMC had gradually revised the expense ratio of regular plan and the difference in the NAVs of direct and regular plans became more significant.

Let me explain this in another way to what Faisal has. This fund was launched Sep 2014, both direct and regular would have started with a NAV of 10. By investing in direct the NAV is 23.78 and by regular it is 23.18. 2.6% more because this much commission wasn’t paid out. So you would have made 2.6% on your capital.

So NAV for direct will always be more than NAV for regular. When you invest in direct today at higher NAV, in 3 years say 2020, you would have seen direct outperform regular by another 2.6%. For you investing today, the outperformance will be 2.6%, but for the person who invested in 2014, it will be much more than 5.2% (2.6+2.6) as he had invested at NAV of 10.

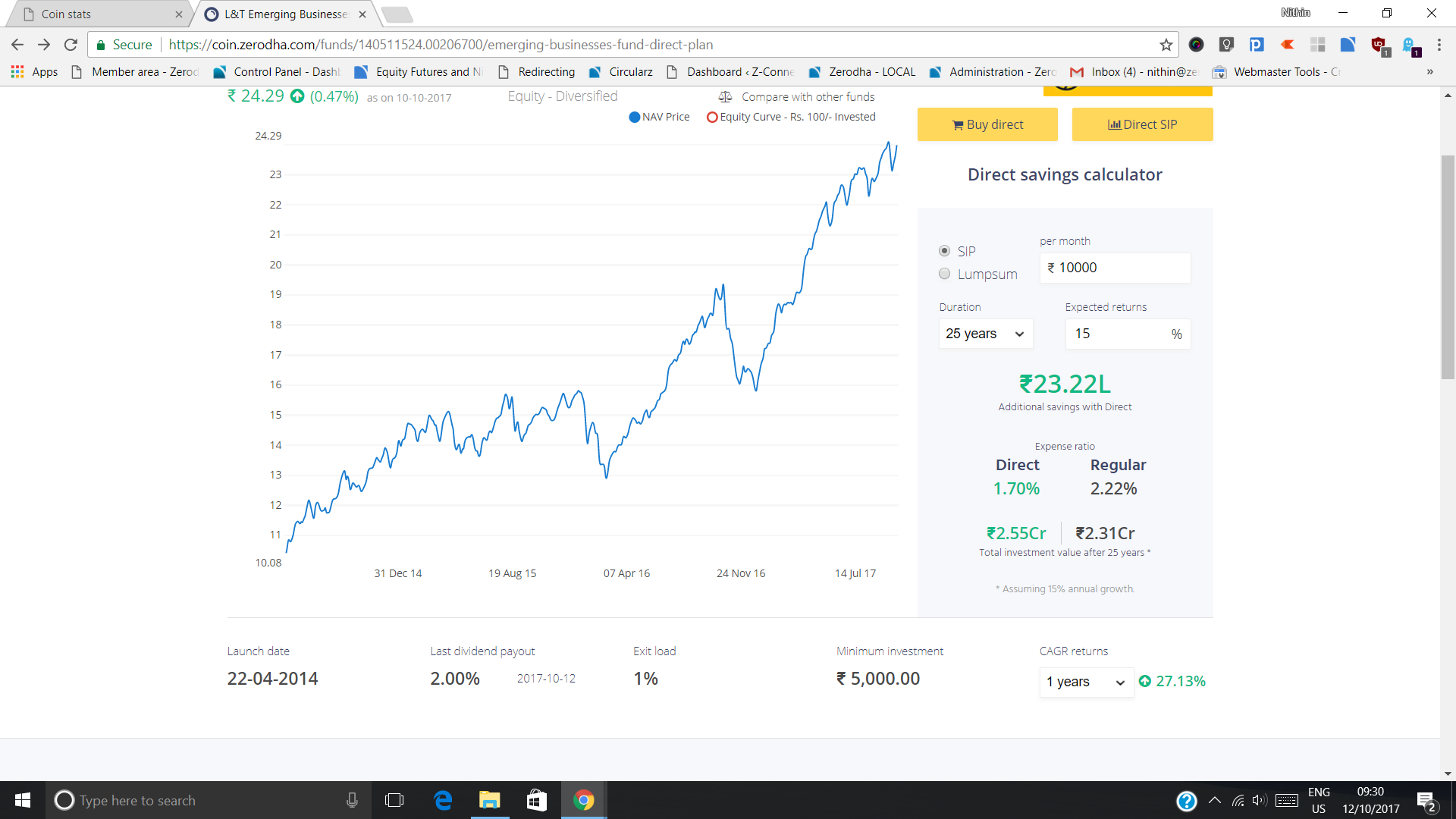

If you visit Coin page for this fund, you can calculate how much you can save in commission by investing into direct scheme instead of regular. Saving of 23lks in direct if you start a SIP of 10k today (NAV at which you invest doesn’t really matter).

you mean if I would have invested in 2014 in Direct plan, I would have been gotten 2.6% more than regular one? So if the growth of company remains same for next three years like previous, I would get 2.6 % more than regular plan?

Yep, when buying MF and comparing between regular and direct, NAV doesn’t really matter. You can’t say direct NAV is more than regular and hence regular is better to invest. What matters is that direct will always yield you more than regular whatever the NAV you invest in as the costs are lower. Everything else between regular and direct other than the expense ratio is the same.

Direct plans in India started Jan 2013. . Most funds went live much later, so the track record to compare direct vs regular historically is around 3 years now. So the NAV difference between direct and regular is not much, but in 10 years - the regular NAV could 60 and direct 75 or higher. Hence even if you invest at more NAV for direct, the returns will be much more.

It’s nice platform to invest direct funds but thing is ,whenever stopped scheme in middle of tenure by AMC it will not continue for next installments in this platform i observed recently stopped Reliance small cap fund-Direct and I was invested from 1 year suddenly stopped & it’s for only for new purchases or additional purchase,Not for existing

folio . If i would invest direct from AMC on that time .Today it will be in active .This disadvantage in COIN Platform, I would suggest you to come up with ECS link. It would be better for those are looking achieve goal. I am paying coin Charges Rs.59/month(Including Tax) only for using your coin platform for direct funds it loss for who are investing less than 2k 0r 1k. There is no much difference between regular vs direct funds. It doesn’t make sense to invest in your coin Platform.

I am a bit confused,

If NAV of direct plans r more than of regular, then the person investing in direct would be purchasing unit costlier compared to regular, so is this purchase on direct wud nullify commission saved compared to regular over time??

Pls clarify

The NAVs of direct funds are higher because their expense ratio is lower. What you should be looking at is the returns and not the NAV or the number of units. Check this post for a detailed explanantion -

I totally agree that direct funds are better than regular. With this thought only i joined zerodha coin platform. With in a month i invested almost 1 lakh through SIP’s.

But now when i got to know that you charge ₹59 monthly and 300 yearly which is equal to ₹1080 per year. Even after taking the direct funds i will be loosing a lot of money over a long period of time. With time these ₹59 will also increase and then i am more screwed.

So anyways these charges would have given me returns upto 1 lakh in less than 2 decades.

Didn’t see anything attractive to pay these charges.

1000/year( Zerodha charges) for 20 years can give me 1 lakh after 20 years. Moreover i am assuming current charges remain same for 20 years. For sure, these charges will also increase so total amount will be more than this.

Rs.300 they charge is an AMC for your demat account, it isn’t exclusive to coin.

Dude, the prices of everything in your life go up. That’s called inflation. By that logic, do you compound all your expenses in life? The Rs.50 is a subscription fee, you cannot calculate compounded returns on that is incorrect.

We Indians have a tendency of expecting everything for free,

Totally agree but i am not interested in trading into stocks. I am only interested in Mutual Funds so they should come up with a platform or an option of Mutual fund separately with charges of 50/month.

Not even Indians but everyone compares the services from other competitors. Happy to pay 50/month if the UI and more features should have been there in Coin. I am a new investor and I have seen some portals which shows per day NAV’s of your fund with just one clicks and we can even add our funds from other sources as well.

There’s no actual conversion of Regular funds to Direct. You essentially have to exit Regular Funds, and invest in the same plan on a Direct Fund on Coin. Transferring a Regular Fund to Coin doesn’t make it Direct either.

You can set-up a fresh mandate for Direct SIPs on Coin.

P.S, Coin is completely free to invest in and is super flexible.