In positions once I select option legs and create name for that strategy, can I have drop down such a way that if I have 3 different strategies I should able to select positions I want to see with my strategy name.

1 Like

Perfect … We do have a mechanism to label the individual legs with strategy name under Strategy Marker. Notice the strategy name in red just below the product name. And it works for multiple strategies in a position labelled accordingly.

I understand that a drop down with a specific strategy selection will lead to focussed attention to the strategy. But one can still have it in the next screen by simply clicking Risk Analysis which will only show the strategies in place. Isn’t it?

Did I get your question correctly? Does the next tab of Risk Analysis serves the purpose of focusing on individual strategy and is labelling it with strategy name differentiating it from the rest? Do let me know … Thanks.

![]()

2 Likes

Hey @Sensibull … Nice to have your revert … I thought we will never talk … Lolz … Can we be friends ![]()

Ok. So this is where it gets interesting. Off course it is Algo and you can have better bid and be faster, and I do understand the illegal part in front running is sharing of market interest but how do you differentiate it from the other?

In this case, notice the clock running on top-right in seconds, it was quite quick. Notice the previous bid on 67.1 exactly matching my order size 5200 and notice the teaser best bid just 0.05 away - that is used as a best form of alert to know if someone is interested - to get a fill on your own order. I know it can be a plain vanilla algo but I am inclined to believe it is working on my interests especially with the order sizing.

Mid tier prop desks … I am badly informed about India … Do you know who runs those shops?

Dude! Are you serious? Do you know where the Algo was getting its feed from?

Anyhow, the point was not that if this is legitimate algo or front running. The point was to detect this … and kill the Algo/Insti in its own game. Either ways … ![]()

Hey Risk,

I had deleted the post because I didn’t want to be misconstrued as pointing out a mistake. Thanks for taking this in the right spirit.

So here is the key difference between front running and what happened here:

Front Running is when you have info about an order and you act on it before it hits the market. Your outbidding happened AFTER placed the bid.

For example, this is what they do inside a bank

Look at this hypothetical situation

Let us say I am a client trader in a large bank, and Nestle, my client is selling 1.2 Billion USDCHF. Now the prop trader in my team is my friend, ( or I am the prop guy) and I will tell him that “dude CHF is going to move, why dont you trade?” ,

He hits the order before Nestle. Now I do Nestle’s order and create a small move say 5-10 pips (donno the number these days have been ages since I hit cross currency), then he covers his order.

In your order’s case, there was no front running. They did not know that your order was coming. They saw it after it arrived, and then put a better bid than yours in a matter of milliseconds.

What happened there (most likely) was there were one algo there which said best bid till 72.05 and another one which said best bid till (X) where X> 72.05.

So when he put that 70, the two algos went on a flame war, and one settled at 72.05, and the other bettered it at 72.10, one tick higher. So you put 70, the first guy did 70.05, second guy did 70.10, first went 70.15 and so on and one of them stopped at 72.05 at its limit and the other other at 72.10. Also since this is an option, it is highly likely (99%) that the bidding happened on an IV and not on the price. They were earlier peacing out around 67, may be your order triggered the change in them, I don’t know what happened there.

TL;DR - the difference between front running and this is the fact that in front running you had info about the order pre-facto, and worse, it may have been given to you by someone who is a client of yours to whom you have a what is called “fiduciary responsibility”

Mid-tier - IIFL, Edel, MO, Alphagrep, many

Algo Source - There is no need for feed, this is market tick by tick data. You just need a colocated server in NSE for low-latency.

Come on bro, but you are throwing me under the bus here … ![]()

First, my apologies. Let me be clear, I am not implicating anybody here. And just to put this in perspective and avoid being misconstrued I will go the extent and say it that the video is NOT front running. Period.

But you are completely missing the point. I never said that the video is proof of front-running. I just took it 10 days back for I was missing on a number of fills and it came handy to show how front running will look like and what I suspected then.

How do you know that whose order arrived before? It will require a forensic audit to ascertain that … My only point was that this is exactly how a front running will look like from a retail terminal and thats why I used it as an example.

As a matter of fact, what you are describing is the most basic form of it. We are on different pages here. The game is totally played in a different fashion where it is across exchanges (ARCA,BAT,NYSE,NASDAQ,DJIA). So, if I have a big order that is not going to get filled on exchange1 I will try to get a fill on exchange2, exchange3, exchange4, sequentially. But my interest in exchange1 is recorded and then I will be raced towards getting a fill on exchange2. That is the kind of front-running I am talking about.

And this totally summaries my whole point. It was at the exchange level I am talking about. I am sure you are aware of ‘Algo manipulation’ case: NSE files for consent; experts call it premature - The Hindu BusinessLine

and how certain entities were getting preferential treatment from the same tick by tick data feed on collocated servers and using it for front-running.

The bottomline remains the same. Let me mention it at the risk of repetition, the following -

Peace. ![]()

2 Likes

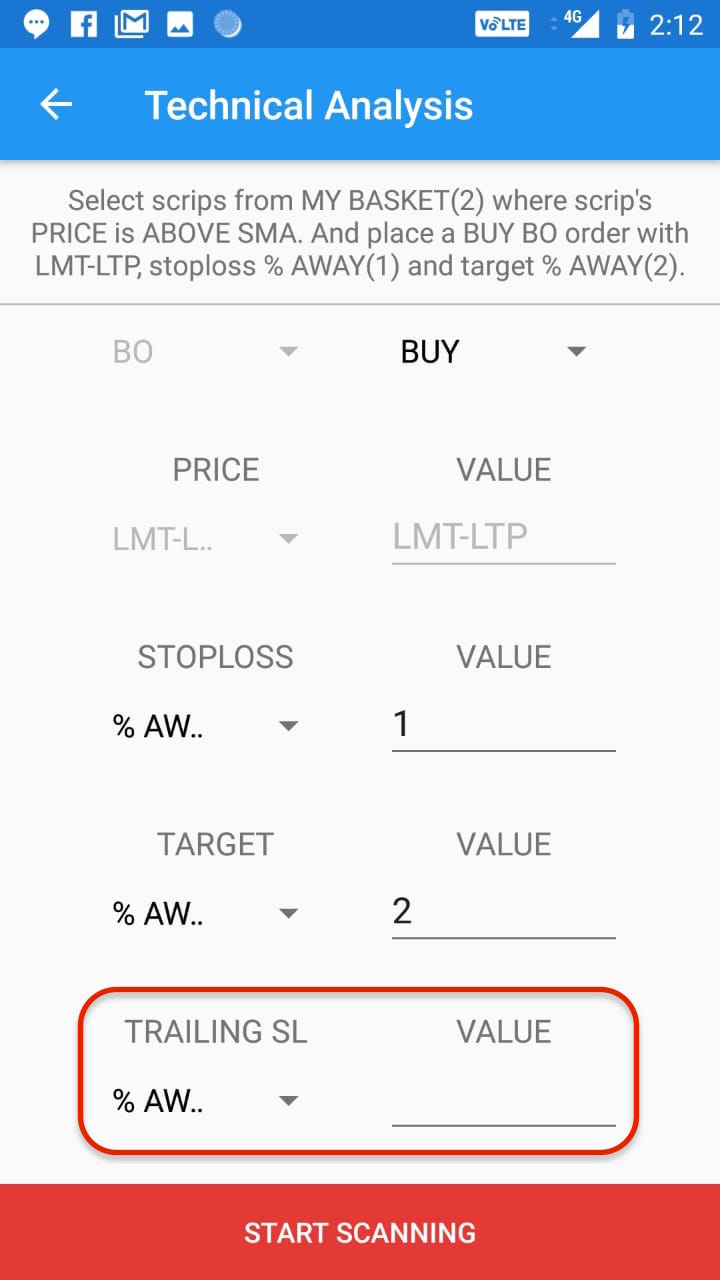

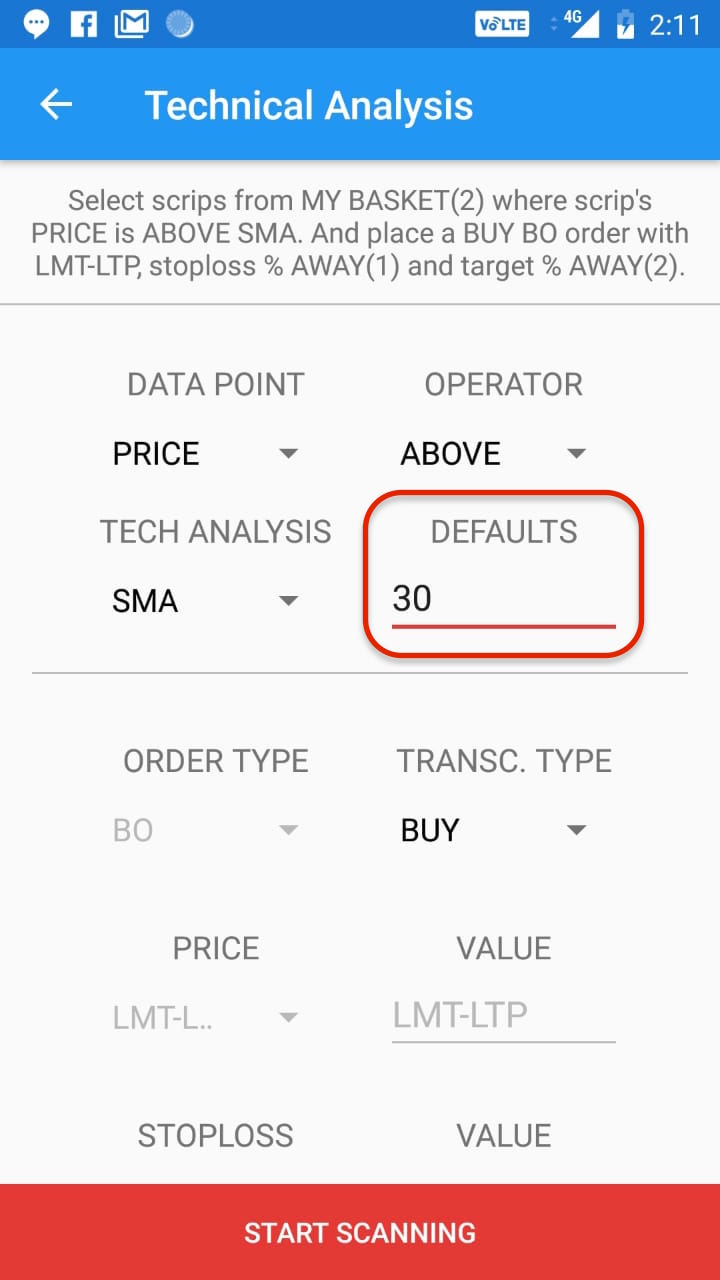

Ok. Implemented an awesome new feature to match a friend’s trading style - under Strategize - AutoRisk Basket Order. So here is how it works -

- You make a basket of stocks by identifying the stock name and quantity you wish to trade.

- On the next screen you set the technical analysis, along with target and stop loss you wish to keep.

- Next, we scan the list of stocks to match the criteria you gave and present it in a Tinder style swipe format with charts.

- Finally, all right swipes create an order entry showing you the stop loss and target for respective stocks carefully filled with the criteria you provided.

- One click execute Bracket Orders.

Workflow to make it crystal clear -

Note: I can extend it to any technical analysis but have put in only 12 to begin with. Unable to prioritise here. So if you elaborate your trading style along with the technical indicator in question, I will be happy to integrate it in AutoRisk Basket Orders.

Add. Note: The idea is to make technical analysis work for you. I briefly discussed one of the ways to make TA work for you via Parameter Optimisation -

Another way out is to distribute the risk across different stocks with the same TA you have been vouching for. This is where “AutoRisk Basket Orders” should help.

Yup … currency is ripe for that kind of manipulation with the kind of participants therein … especially banks and govt. treasury who are not invested heavily in HFT and do it for plain vanilla hedge …

Hi, Any plans to implement Put Call Parity for Nifty Option Chain ?

Hi @prakash1975

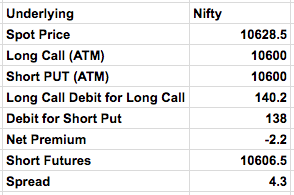

Hmm. I did wonder if those kind of arbitrage opportunities still exist especially in NIFTY. So I went ahead and did a calculation for NIFTY 10600 CE LONG @ 140.2, NIFTY 10600 PE SHORT @ 138 and NIFTY JUN FUT SHORT @ 10606.5 considering today’s EOD prices. The spread was only for 4.3 Rs.

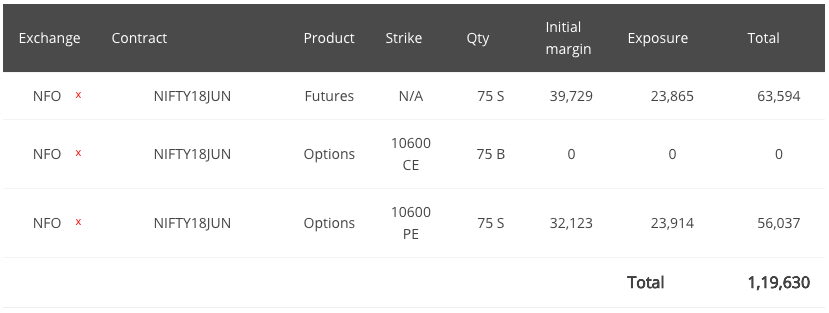

Putting it in span -

So for Rs. 65876 in margin you will be earning 75x4.3 = 322.5

Subtracting Brokerage = 20x3x2 = 120

You are left with 202.5 Rs. which is a mere 0.3% monthly returns totalling to 3.6% annual returns matching bank interest rates.

Not worth the effort at the moment … unless you have some other way to trade put call parity … do enlighten …

Cheers!

1 Like

While adding stock it is saying “Please enter a valid stock”. May be symbol search option is not getting connected.

Aaah. I see the issue and was able to reproduce it. Basically, the user action expected is to select the stock name from the drop down to load the stock details. I will rephrase the error message in a better fashion.

Thanks @siva for pointing it out. ![]()

I am not able to find how to add scrips to basket, can you please guide me.

Sure. Make sure you have latest release (v42).

Home > Risk Dashboard > AutoRisk Basket Order > Add New Basket (+ On Top Right) > Click on Newly Created Basket > Add Stock (+ On Top Right) > Search For Symbol > Click on the stock name from DropDown List > Qty is PrePopulated > Click Add To Basket

Workflow for Reference -

You may add as many stocks as you like. Once done click on “Set Scanner” to place order defaults and TA analysis to be carried out -

1 Like

This is awesome.

1 Like

Do something on trailing stoploss

Can you please add the default parameters you are using to calculate those TA?

Ack … Will add trailing stoploss by EoD.

Yup. It is currently using the defaults. But sounds fair.

I will give an option to load the defaults and edit it if required. By EoD.

One more thing sir… Screening the nfo scripts which are far above or far below from max pain strike…

Thank You

1 Like