As we all know SEBI had in 2020 introduced peak margin requirements, taking 5 snapshots at random intervals to check whether sufficient margins were maintained or not. And if there was any shortfall it resulted in a peak margin penalty.

SEBI in its recent circular made changes to this. According to the circular:

The margin requirements to be considered for the intra-day snapshots, in derivatives segments (including commodity derivatives), shall be calculated based on the fixed Beginning of Day (BOD) margin parameters. The BOD margin parameters would include all SPAN margin parameters as well as ELM requirements.

There shall be no change in methodology of determination and collection of End of Day (EOD)margin obligation of the client. Also, there shall be no change in the provisions relating to collection and reporting of margins in the cash segment.

All the changes will be applicable from 1st August, 2022.

While this doesn’t mean we will get leverage for trading in F&O segment like we used to before the peak margin rule came into effect. But it does provide relief as we will not have to worry about intraday margin spikes resulting in peak margin penalty if we didn’t have sufficient margins.

If a trader has taken positions and the margin goes up intraday, there won’t be any peak margin penalty on those positions. This was the biggest reason for margins going up. The flip side with this is that since the beginning SPAN file is used as reference for the day, if the margins drop, there won’t be margin benefit intraday.

But this circular still doesn’t solve the issue of margin going up when a trader who has multiple F&O positions exits one resulting in overall margin going up and peak margin penalty on that.

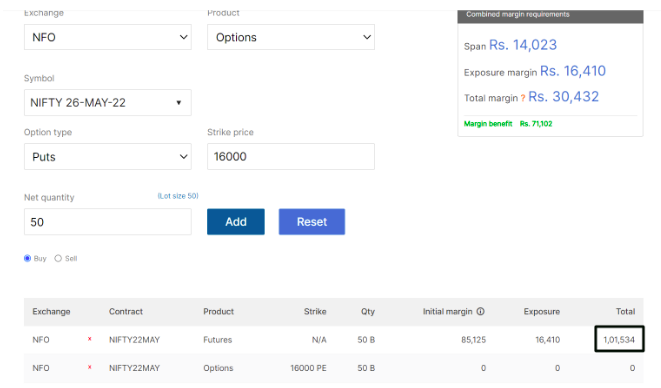

Assume a trader has Rs 1.05 lks in the account and takes a future position with a long put as shown below. Since the position is now hedged, the margin for both positions drops from Rs 1lk to Rs 70k. Assume the trader withdraws Rs 35k from the account on the next day and the money in the account is only Rs 70k. If the trader exits the put position, the margin for futures will go up to Rs 1lk again leading to peak margin penalty.

I think that it is a good move and a step in the right direction.

But if one takes F&O position in morning and does not change it throughout the day, do we still expect margin requirement to change intra-day based of market movement/volatility?

Last week I took position in morning, and at 2:30 zerodha send margin shortfall alert and squared off some of my positions. They say new rule is only applicable for “penalty”, but margin will keep on changing based on market volatility.

That’s right. The onus will now be on Brokers for peak penalty.

Yes. It can happen due to the following reason(s) :

Increase in margins consequent to import of latest SPAN file

SPAN files (files on the basis of which margins are calculated) are updated by the exchanges multiple times a day, on the basis of which the margins for client positions change. The possibility hence arises wherein a client could have brought in, sufficient margins at the time of entering into an intraday position, only to realize subsequently that the upfront margin requirements have increased, after the import of the latest SPAN file.

If i take intraday positions in multiple stock futures, without any hedging, and square them off before 1520 - can my positions get squared off due to intraday margin changes after having taken the position ? If yes, how to manage this ?

if your margins become negative , there is a chance of square off. As, the risk of penalties still exists and if it is related to MTM shortfall, penalty may have to be borne by clients. As penalties for MTM (mark to market) shortfall, delivery margin, additional margin, etc. will continue to be passed to the customer (regulations allow for this to be passed).

Best way is to ensure there are adequate margins and second best way is to take hedged trades as naked trades are both risky and also require higher margin

As i said, use case is intraday only. I thought peak margin penalty no longer applies. All delivery related margin

issues are not relevant for intraday. Are there still going to be penalty issues ?

This whole episode has been a complicated mess from start. BOD margin as reference made a lot of sense and delivery guys can bring in money if needed EOD. But no time to do that for instantaneous margin changes.

Yes, so ill likely try to use say 95-90% capital as max limit and see how it goes. Hedging is out of question as stock options are not liquid and i am only trading intraday. I don’t need extra slippage complications.

I currently trade stocks cash only, looking to start doing same in stock futures. I cannot see how it is any more risky, with only 2-3-5X margin in Futures vs 5X in stocks.

I thought BOD margin requirement had solved peak margin mess, but it seems SEBI rules are still not going to be easy to comply with. On one hand it looks like retail does not need to manage instantaneous margin changes and on other hand we have talk of square off. I understand it might be needed for extreme cases, but naked futures intraday with low margin (2X-5X usually) does not seem to be an extreme case …

As an intraday trader in stock/index futures, is there any kind of penalty possible, apart from 40 brokerage? Asking as i don’t trade futures yet.

Please try to allow a slight buffer of negative margin on existing positions - or ask/have an option for extra margins upfront - say 5-10% to mitigate all of this. I understand there can be many different cases and in some case account can go into large negative margin, but for my use case with naked intraday futures - Its much more likely for slight breaches only in rare cases. Also M2M intraday losses with stops in place generally should not lead to positions getting closed either. It would also help if rules are completely transparent.

There won’t be any peak margin penalty for you. If at all, there is a shortfall and CC captures a screenshot, Zerodha will have to pay the peak margin penalty on behalf of clients.

As there are still lots of issues on this front currently esp for us brokers, We are working on an ideal scenario where both brokers and clients are not at loss. Will keep you updated if there are any changes.