For seller perspective, I’m obliged to deliver 700 quanties of SUNPHARMA at 1450Rs/stock.

However, I bought this stock at 1300Rs and now I’m selling it at 1450Rs,

So, the net credit is profit of 105000 [700*(1450(sell)-1300(buy)] + 21000 (700*30premium ),

Is my understanding, right? or Am I overlooking anything here.

I’m purposefully not considering the money that would have been made by selling 700*(1550 current price) as a loss factor and satisfied with selling at 1450 as per contract.

Yes,your understanding is right.

Only the loss is based on current market price you could have made 1500(spot closing)-1450(strike)=50*700=35000. As already premium credit is 21000, overall loss would be 14000 as you preferred selling the shares via physical settlement.

Kindly note brokerage of 0.25% of the total value of physical delivery is charged due to the additional effort and also all physically settled contracts, like stock delivery trades, will carry an STT levy of 0.1% of the contract value for both the buyer and the seller of the contract.

thank you @Ragavendran_M for the quick support and clarification.

Does the same assumption hold for writing PE option. assuming , PUT writer to willing to take delivery of stock.

same example

Write 1 Lot of SUNPHARMA 1450 PE at 70020 = 14000 credit

SUNPHARMA reaches 1400 on March expiry.

PE Writer needs to take delivery of 7001450 Rs/stock. whereas market price is 1400,?

PE writer expects stock to bounce after a period and hence not worried about current price.

in this case, the PE writer can keep the premium of 14000 and needs to take delivery of stock by spending 1450700 = 9.8 Lacs.

Theoretically the loss could be 700 (1450-1400) = 35000 if PE writer takes delivery and sells it soon. (assumption made: stock remains around 1400Rs with no big deviation)

Is this right understanding, right ?

Please ignore if there are too many assumptions made, I’m just trying to correlate my understanding with experienced people, so as not to take any false understanding.

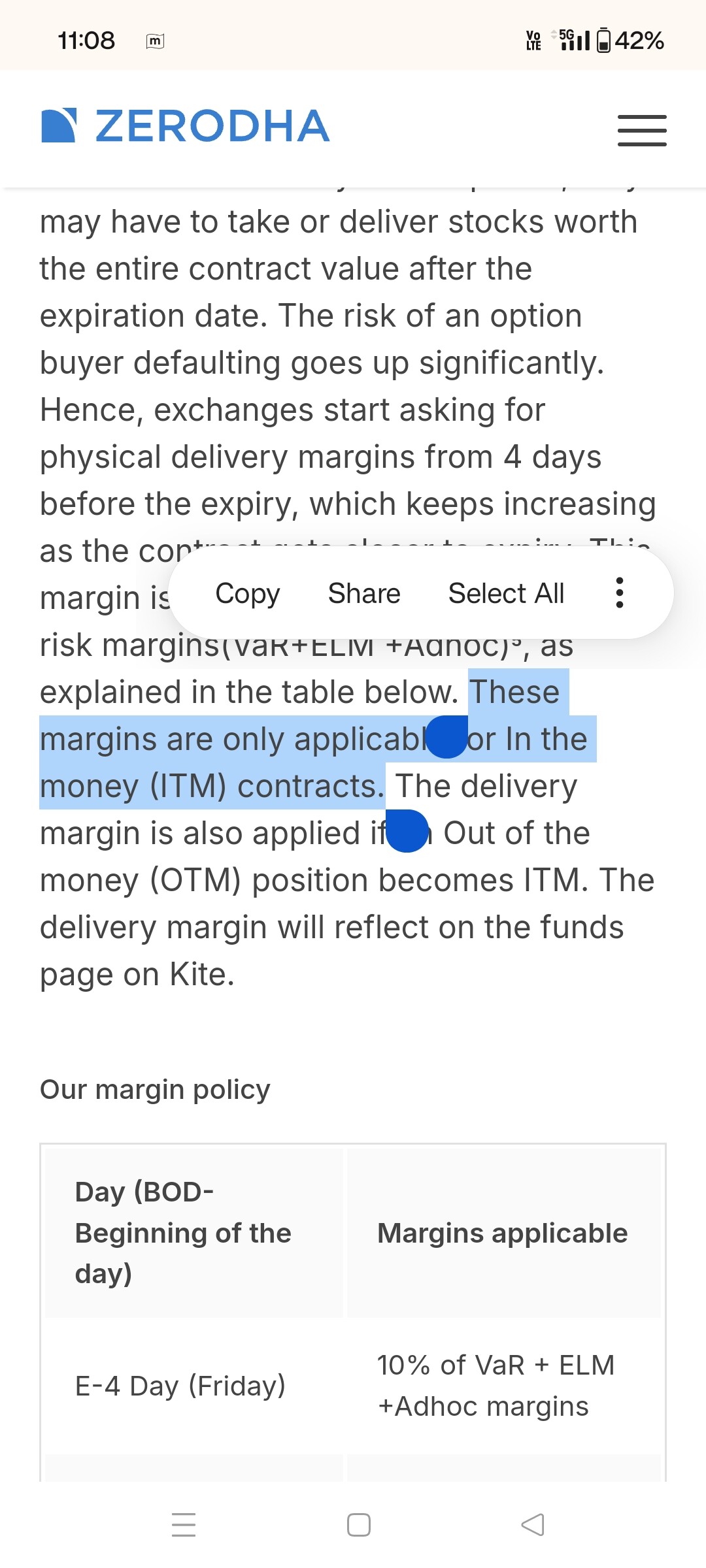

“Taking or giving delivery of the entire contract value worth of stocks requires either full cash or stocks in the Zerodha account post-expiry.”

If client already holds the stock worth the contract size, will there be an increase in margin,

close to expiry if CE option is turning into ATM/ITM ?

[apart from the original margin blocked during the contract entry]

Yes, if you have having short option position, on expiry day margin will be increased to 50% of the contract value or 1.5 times NRML margin (whichever is lower) irrespective of stocks available in the demat account.

@Ragavendran_M sir.

Can you please guide about the following scenario?

Suppose I have 1 lot futures short and 1 lot stock pe short?

I suppose these positions will net off if pe goes itm…

But I want to understand the increased margin requirements near expiry…

I have read the physical settlement link…

I suppose the margins for both legs will separately increase…

Because I am short pe, the margin requirements will increase only on expiry day for this pe leg?

What will be the increased requirements for futures short leg? Expiry day or expiry week?

Can you please guide in detail?

Thank you

Thank you…

So, as per my understanding, margins increase in expiry week only for futures and options long…while margins increase only on expiry day for futures and options short…

Am I correct?

@Ragavendran_M sir.

Good morning.

I have one more query.

Suppose my futures short and pe short are netting off on expiry day, what will be the total charges I’ll have to pay?

I see the brokerage is 0.1% of contract value…

That means 0.1+0.1=0.2% for both legs

+Stt?

Can you please explain with example, say sunpharma 1 lot futures short+pe short net off scenario?

I just want to know how much it will cost total if I let it expire VS square off even if pe leg is illiquid?

Thank you once again.

Brokerage will be 0.1% of total turnover.

Sun Pharma’s contract value for One lot is around 1092000. Overall turnover in this case is 2184000. So brokerage will be Rs.2184.

@Ragavendran_M

If a “short index option” expires ITM or slightly ITM or even ATM with some intrinsic value, will any brokerage or other charges will be applicable for settling it.

Eg: if I write a nifty option at say ₹50 and say it settles at ₹45 or ₹55. Will in any case brokerage or other charges will be levied for settling it

Hi sir,

Suppose I short an index option that expires on the same day. The option expires out of the money (OTM), and I did not buy it back. Will brokerage fees still be charged? If so, why? Since the contract expired with a value of zero and was settled by the exchange, there should be no additional work required by Zerodha

@Ragavendran_M sir…

Good morning.

I have read the varsity article regarding physical settlement.

My doubt is, does the increased margin requirement apply to otm short/long options?

Or does it apply only to itm option contacts?

I understand that the future contracts will always require increased margins near expiry, whether short or long.

Thank you

For long option - only ITM contracts physical delivery margin will be applicable. For short options both ITM and OTM physical delivery margin applicable only on expiry day.

@Ragavendran_M sir.

Thank you for the reply.

I now understand that otm long options don’t have any increased margin requirement. The margin requirement may increase if the otm strike turns itm. I get it.

My query now is regarding increased margin requirement for otm short option on expiry day.

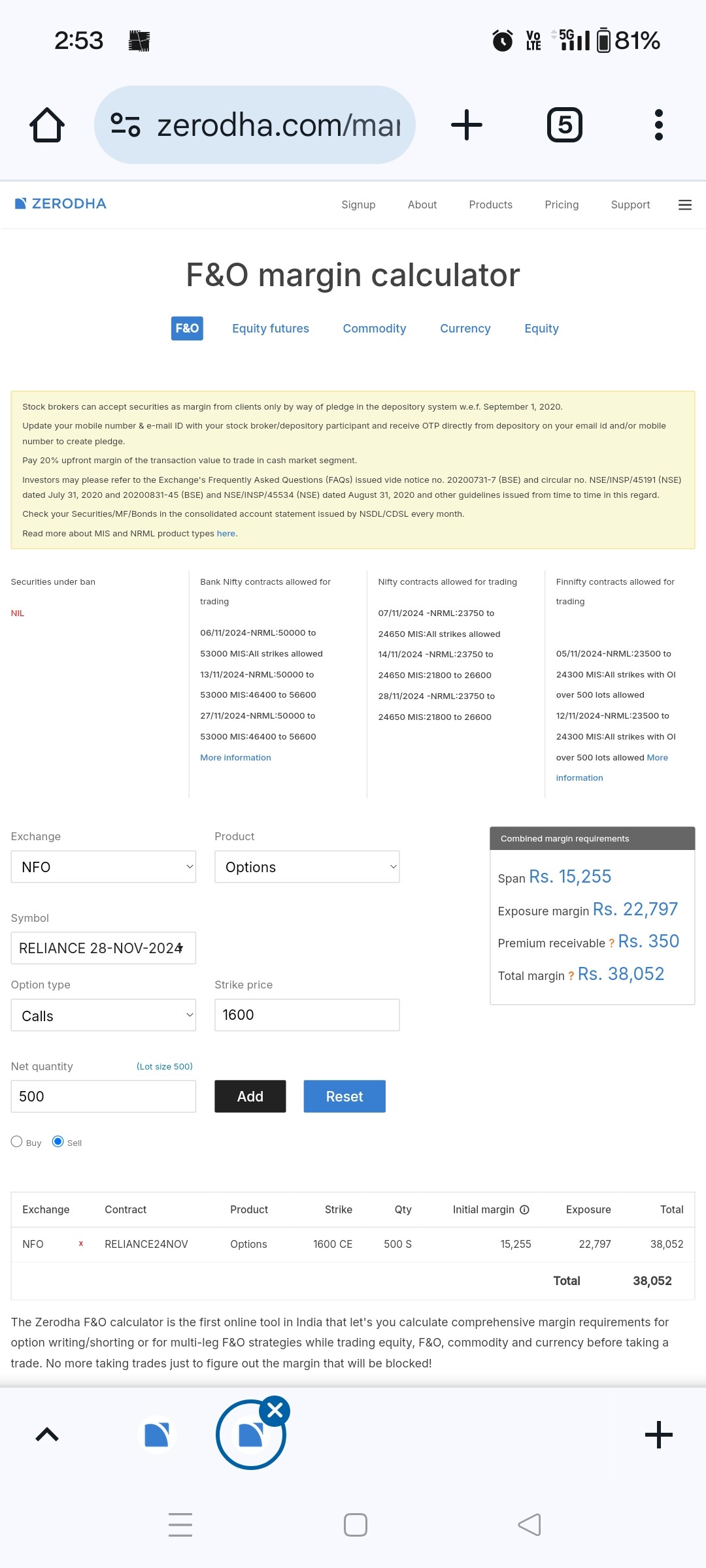

I have tried to use zerodha margin calculator.

The article says: The margin requirement for all stock futures and short options contracts increases on the expiry day to 50% of the contract value or 1.5 times NRML margin (whichever is lower).

Can you elaborate on the scenario, screenshot attached.

Say shorting otm strike of reliance, contract value: 1600x500= 800000

50% of contract value= 400000

So, is 4lac the requirement on expiry day?

Can you please guide regarding 1.5 times nrml from the screenshot attached, and solve my doubt?

Thank you for your time and support.