As per the Scheme of Arrangement between Tata Motors Limited DVR (TATAMTRDVR) and Tata Motors Limited (TATAMOTORS), Tata Motors DVR will be suspended from trading w.e.f. August 30, 2024 (i.e., closing hours of trading on August 29, 2024). You can check the exchange’s announcement here

What was the Scheme of Arrangement?

Tata Motors will first issue 7 Tata Motors shares for every 10 ‘DVR’ shares and then cancel its DVR shares.

What are the tax implications?

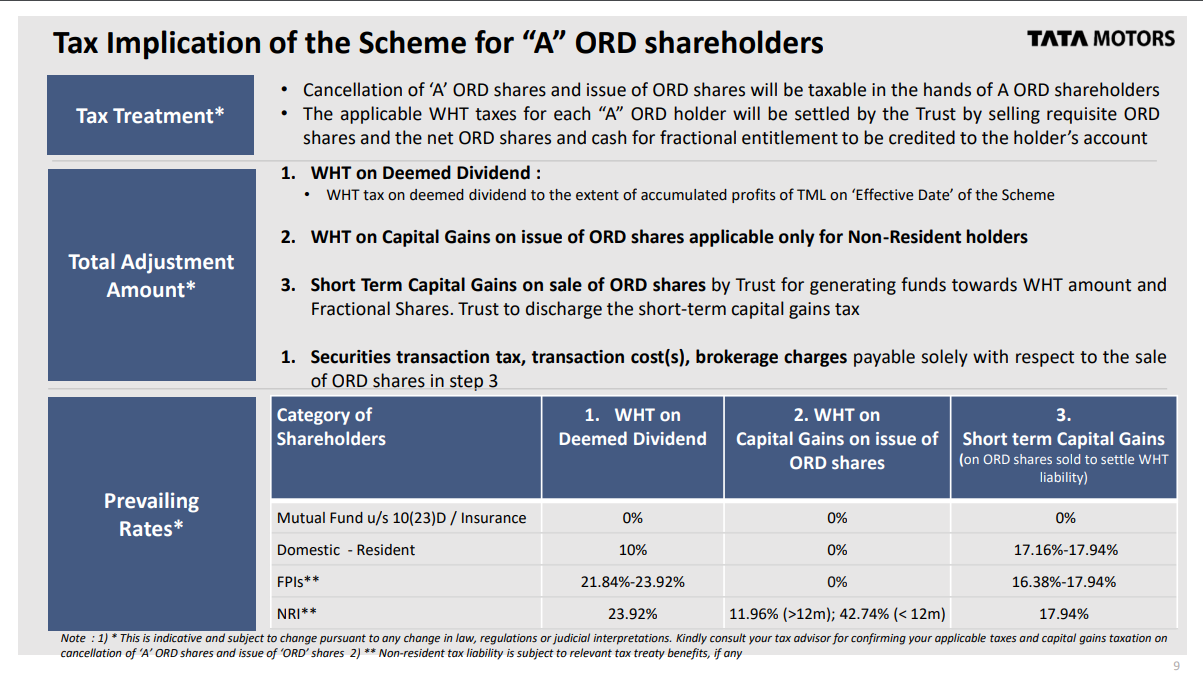

- Firstly, this arrangement doesn’t affect Tata Motors shareholders. For Tata Motors DVR shareholders, It will have the following tax implications:

Before we get into the details, it’s important for us to know about the Deemed dividend and WHT

What is Deemed dividend?

As per the Income Tax Act, Any consideration in a capital reduction scheme distributed in the form of new shares is treated as a distribution of accumulated profits to the shareholders.

Accordingly, accumulated profits as of the record date will be treated as “deemed dividends” and taxed in the hands of shareholders.

What is WHT?

WHT stands for Withholding tax which is deducted in advance, and the same is deposited to the government before the amount is paid to the payer. it is generally applicable on payment to non–residents and foreign transactions.

Difference between WHT and TDS

- TDS and WHT are essentially similar with the only difference being that TDS applies to Indian residents while WHT applies to cross-country payments.

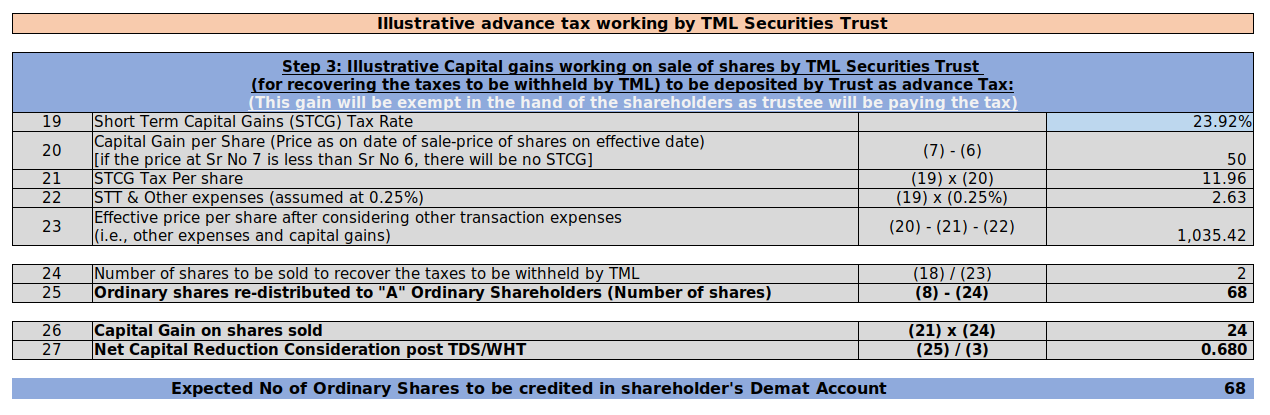

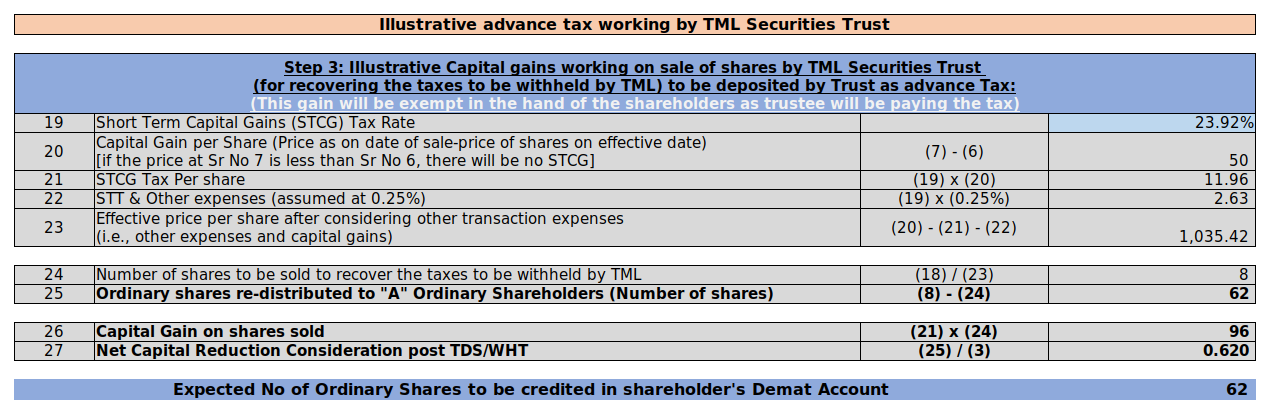

To pay for the TDS and the WHT, The trust will be selling ordinary shares accordingly, pay the STCG liability that arises on this sale transaction, and credit the net ordinary shares and cash for fractional shares to the shareholder’s account.

TL;DR:

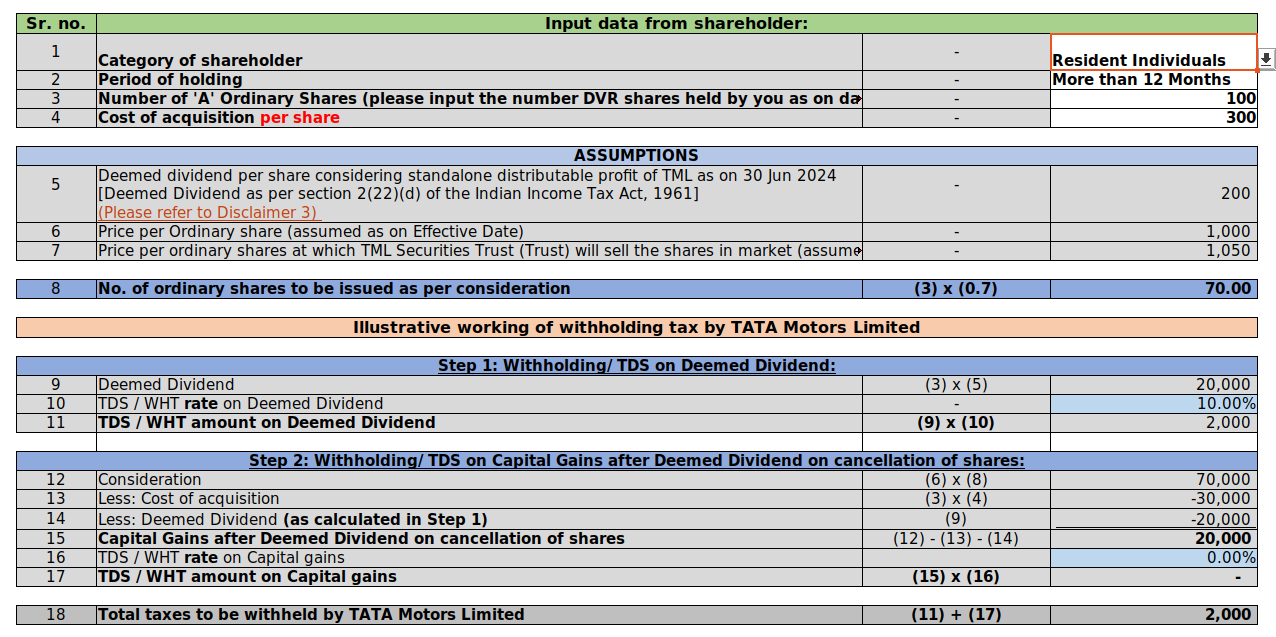

For Resident individuals:

Allocated ordinary shares as treated as dividends

The trust sells some shares to collect TDS.

Net shares and cash for frictional shares are credited to the investor.

To give you an example for resident individual investors:

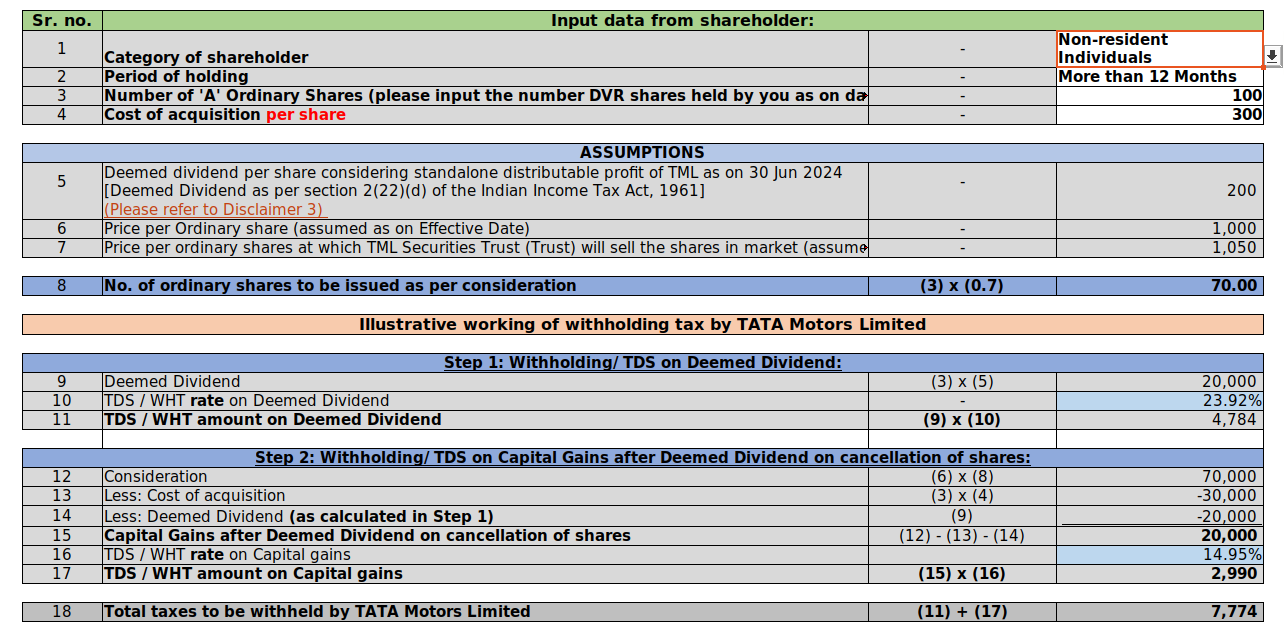

For Non-Resident individuals:

TDS is deducted on dividends (as above) + TDS is also deducted on capital gains.

To give you an example for non-resident individual investors:

Important dates - Indicative timelines:

| Particulars | Timeline |

|---|---|

| Record date/Effective Date | 30th Aug 2024 (T) |

| Initiating action of allotment of New Ordinary Shares to the Trust | 30th Aug 2024 (T) |

| Finalisation of WHT details of Shareholders | T+9 days |

| Listing & Trading Approval of the New Ordinary Shares | T+10 days |

| Sale of the requisite number of New Ordinary Shares by the Trust for WHT recovery (including other taxes & expenses) and fractional entitlement | T+15 days |

| Credit of balance New Ordinary Shares to the “A” Ordinary Shareholders account | T+ 17 days |

| Remittance of cash (if any surplus on block deal + fractional entitlement sale) | T+20 days |

Source for the above timelines

What is the Tax implication for you as an Investor?

-

If your overall taxable income while filing your Income tax return (ITR) and overall tax obligation is less than taxes deducted:

-

You can claim the TDS refund while filing your ITR

In case, You’ve sold the new shares once you received them:

-

In the case of LTCG, you can carry forward the LTCG amount, if it is below the exemption limit of 1.25 lakhs per annum

-

In the case of STCG, you can set off against the basic exemption limit if you’re overall income is below the basic exemption limit.

Please consult your financial advisor while filing your taxes.

We’ve also explained all the FAQs in our support article