This is currently not possible. But some updates are planned to be released which will allow this in the future.

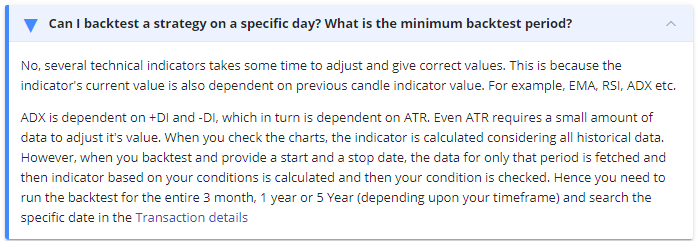

Testing a strategy only for a day is statistically not significant. Such a short period has a very less probability of generating alpha. Having said that, this was done because several technical indicators take some time (data) to smoothen.

When you check the charts, the indicator is calculated considering all historical data. However, when you backtest and provide a start and a stop date, the data for only that period is fetched, and then indicator based on your conditions is calculated and then your condition is checked.

For example, your strategy is Close crosses above EMA 200

When you run the above condition for one day, the data for only that day is fetched and then a 200 period EMA is calculated. One EMA value is this scenario is calculated by averaging 200-period data. Now, depending upon the timeframe, you might not have enough data point to actually calculate a 200 EMA.

Also, EMA works with the principle that it gives more weight to recent data, in other words, current EMA is also dependent on previous candle EMA. If you calculate, EMA on 1,000 data points and 10,000 data points, you will find that EMAs calculated on the same candles would be different. This is because the more EMA data is calculated, the smoother it becomes.

If you compare the difference of the EMA values in the above example, there might be a big difference. Now instead of running the condition on 1000 data points, you run it on 5000 or 7000 data points, you will find that difference has decreased significantly. In other words, smoothened averages have a negligible difference.

So if you backtest on more data, there will be a negligible difference between the EMA that you see on the chart and the one which you backtest upon.

Also, EMA is not the only indicator, that requires smoothening. RSI, ADX, Supertrend also requires more data.

Ideally, users should not backtest for a day. It does not serve the purpose. Many users did not understand this and it can be a bit heavy. Hence we had to add the limit so that users do not make this mistake.

A lot of thought is put into every option that we add/remove. Our efforts are always in making our client’s life easier. Hope this gives a better clarification.