As we are aware, FNO income is taxable under the head ‘Income from business and profession’ and the gains we generate on trading shares on delivery basis is taxed ur the head ‘Capital Gains’

The existing tax rates applicable are as follows

Income from business: Slab Rates

Story term capital gain: 15 percent

Considering the above I was planning a strategy to reduce my tax liability and I would like to share the same here.

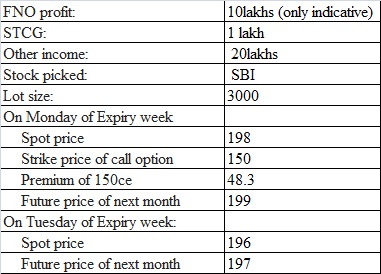

Requirements for this strategy to work:

FNO income falls in 30 percent tax bracket

Good capital

Strategy:

Step 1: Buy Deep ITM (At least 20 percent away) call option of the most liquid stock that you know 3 days before the expiry date. (Monday of the monthly expiry week)

Step 2: Simultaneously sell futures of the same stock of the following month expiry.

Step 3: Accept delivery of the same on expiry.

Step 4: Sell the stock and close the futures position simultaneously once the stock is credited to your demat account(Tuesday following the month expiry)

I will elaborate the same using an example of a stock that I actually used.

Implementation:

Bought 150ce at 48.3 by paying Rs.144,900

Sold futures of next month at 199 for a margin of Rs.160,000

Kept cash of Rs.450,000 aside to take delivery on expiry.

Sold 3000 shares of SBI at 196 and closed futures at 197 on Tuesday following the expiry.

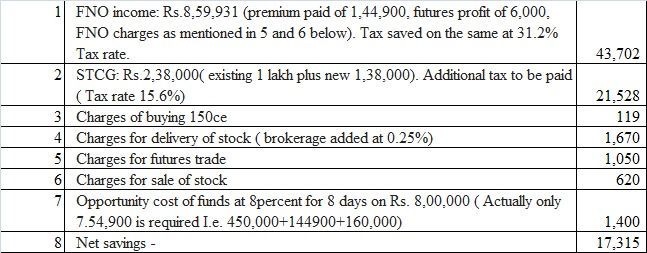

Result:

The questions you may have:

Did I actually do all of this? Yes

Is this tax planning or tax evasion: Well. It’s within the provisions The Income Tax Act. If tax loss harvesting is tax planning then so is this.

Was it really worth it? I was just trying to check if it works. I was even ready to lose some amount if something went wrong.

Limitations:

If you can generate more than the saving from the funds blocked for 8 days then it makes no sense.

If the option is illiquid then, your cost may increase because of bid ask Spread.

Future premium to Spot may change over the period of 8 days. Theoretical it should come down since the days to expiry will be lower. But you know anything can happen.

If you feel I have missed out on something please feel free to comment. Your views shall be appreciated.

Edit: 1. Had made a small mistake earlier in the calculation of profits from futures. Now stands corrected.

2. Tax savings on FNO segment were not considered earlier. Since such expenses are allowed to be deducted, the effect for the same is given.

Future profit is 6000 instead of 9000. Missed that because I saw spot price when I was calculating. Will make the changes by editing the original post.

In option I didn’t lose just 2.3. I lost the entire premium of 48.3. I took delivery of shares at 150 per share (Strike price). Thats how it works when you take physical delivery on expiry.

Since the option is ITM I will have to take delivery of the same at the stike price. That is Rs.150.

I have one doubt. I heard, BTST trades come under business income. So we need to pay 30% tax, even tho, they are kinda technically STCG.

So, what will happen in this case?

I am a bit confused, Zerodha founder says, BTST needs to pay 30% tax, but Zerodha Tax P&L show BTST trades under “STCG”…so how much tax needs to be paid on BTST?

This also seem like a kinda off BTST trade, since ur selling the stock next day.

The figure is not matching because you have taken tax rate for FNO to be 30 percent. After adding cess it comes to 31.2percent (Cess of 4percent on tax liability).

We may still get small difference because I have not taken tax benefit on the expenses incurred under FNO.

Well. I might have to edit the post again.

Thank you for pointing it out. This would further increase my tax savings.

As per the provisions of the Income Tax Act of 1961, the nature of income depends on whether the shares are delivered are not.

If the shares are delivered and then sold from demat then the gains or loss shall be capital by nature

In case shares are not delivered it shall be considered as speculative business.

Lets first understand what exactly is happening with BTST.

Is there delivery of shares (credit) to our demat account before its debited again?

I am not sure but I feel in case of BTST, shares are first credited to our account and then debited again. If this is right, then gains or losses shall come under the head Income from Capital Gains.

Because I made loss, I would be paying less tax than I would have paid otherwise. Its tax savings.

If I didn’t have FNO loss then I would have paid taxes on my 10lakhs FNO income. Now because of this loss I would pay taxes only on 861100. Take the difference between both the values and then apply 31.2percent.

Yes. Thats right. There is a small difference in our calculation because as I mentioned in the above post I have not taking benefit of expenses in FNO.

So if I just see tax savings your value of 22530 is close to the value that I have derived. We are getting small difference in short term capital gains also.

But after that you need to consider the expenses incurred in implementing this strategy. Please refer point number 3,4,5,6 under ‘result’. That totals to Rs. 4859.

I will edit the original post again giving affect to the above so that there isn’t any confusion.

This is not true, and this is probably where your scheme fails.

Whether the profit from sale of shares is treated as capital gains or business income does not depend (only) on whether the shares were in your demat account or not.

Instead, the intent behind the share sale is taken into consideration. If the share sale happens “in the nature of a business”, then these gains are required to be treated as business income and not as capital gains.

And whether the sale is “in the nature of a business” is determined by how frequently you do share (and related) trading.

The following is not true as stated. Please see my comment below for the nuance.

If you are a frequent (say, day) trader, then you essentially don’t have any recourse to claiming profits from share sales as STCG: all share sales before the completion of one year will be treated as business income.

Edited to hide. This is not true as stated, please see my comment below.

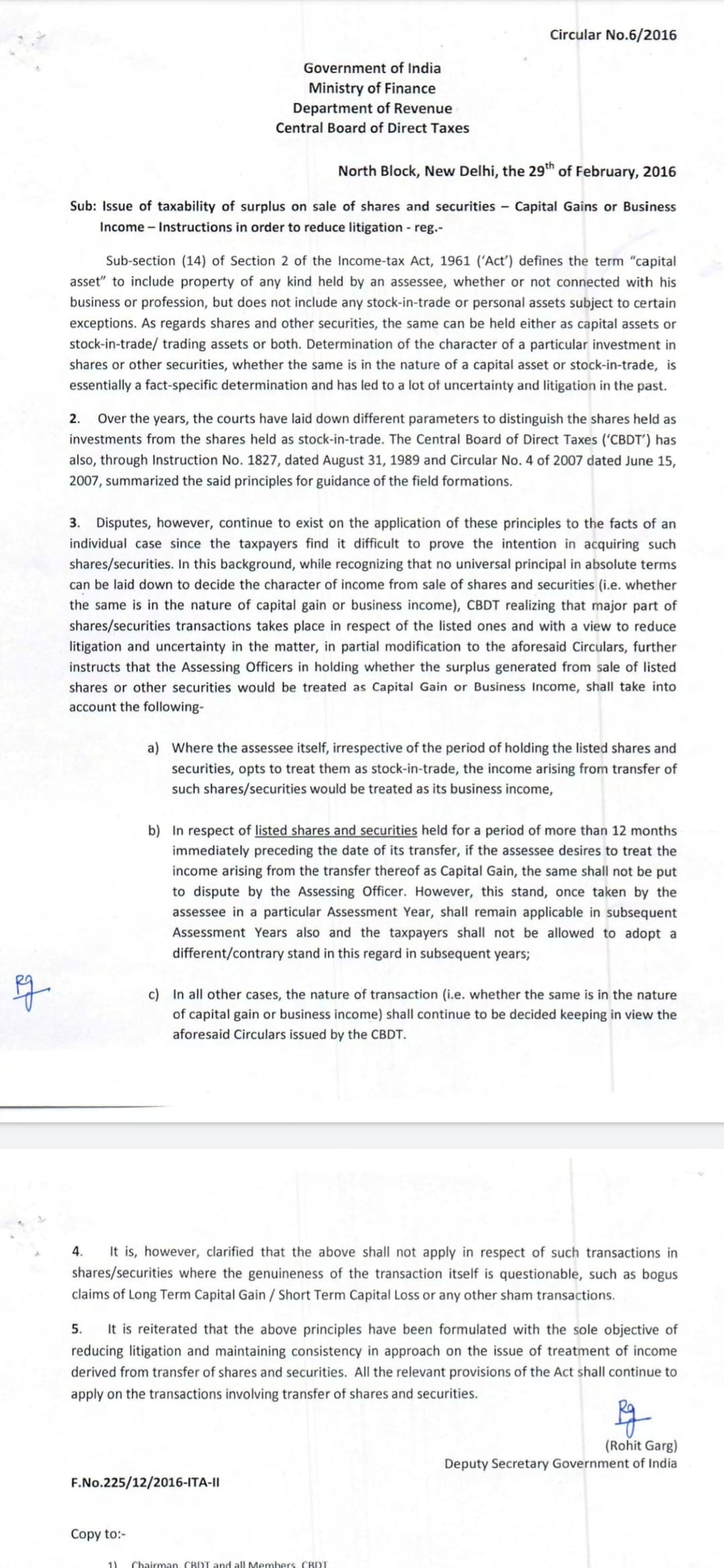

CBDT has issued a circular with the details of how this criterion is applied.

Here are some more references for this: [1], [2], [3], [4].

With all due respect to you, I must say the information provided by you above no longer stands good.

The circular you have mentioned are links to some random Web pages which are certainly not updated.

In support of my stand to treat any gains for delivery trade as STCG I state the following.

Let us understand what circulars are. Circulars are issued to the department and they are only directive by nature.

Hon’ble Supreme Court on various judgements has held that Circular is not binding on a Court or an Assessee. Hence, the Assessee is at discretion to follow the orders, instructions and directions if it stands beneficial.

Further, it is worth noting the overriding preference in Law.

A) An Act cannot override the Constitution

B) Circulars cannot override notifications and the provisions of the Act.

C) Circulars cannot override Supreme court rulings.

D) General Act cannot override specific Act.

The Income Tax Act clearly defines a capital Asset, transfer of an asset, Short term, trading income and so on. (I am not mentioning the sections and clauses because I believe you agree.). Irrespective of what CBDT says in the circular it cannot override the provisions of the Act.

Further, having said all the above, the circular you have stated is dated back to 2007. A new circular was issued on 29th Feb 2016 on the same matter which I have attached here from the official web page of The Income Tax Lasted updated on 26th October 2021.

I would like to highlight 3(a) mentioned in the circular.

The assessee has the right to opt shares as either stock in trade or as a capital Asset. We need to.understand that by default shares are always treated as a capital Asset and that’s why this option is given.

All the professionals in this field also go by what’s mentioned in the Act. We have all come to consensus that if there is delivery of shares in your account, when its sold there is a clear transfer of capital Asset. We are ready to litigate in the court of Law too if required.

I do have few more technical points to stand my view, but I feel this should be enough to rest my case. There is a possibility that I am still missing something. Please feel feel to quote the relevant section. And yeah, my above scheme will hold good. @ZeroIndian

That is definitely not what 3(a) of the circular that you included says. It only says that the assessee has the right to report shares as stock-in-trade, and income from selling shares as business income. It does not say that the converse (reporting shares as capital assets at the discretion of the assessee) is allowed.

In fact

Part 3(b) explicitly lists the one specific case where the assessee has the right to report shares as capital assets (namely: listed shares which have been held for more than 12 months), and

Part 3(c) explicitly says that in the remaining cases (namely: unlisted shares, or shares held for less than 12 months) the determination of the nature of sale will be as per the previous circulars.

As far as I can see, this circular merely re-affirms what the earlier circular (that I linked in my previous reply) says, and makes the same criteria clearer. It does not contradict that earlier circular.

However, given that I am not a tax expert, nor an expert on constitutional law, I could very well be completely wrong in how I read these things.

Since you have specifically disagreed on only one point I believe you agree with the rest of the points.

When an option is given to the assessee to choose a particular option, if its not chosen then by default the existing provisions stand.

Lets understand why it became a debatable issue in first place. Assessees wanted to treat losses from shares as business losses for the main reason they wanted to carry forward the losses for 8 years. Also all expenses related to share trading could also be claimed as business expense. This was questioned by few assessing officers and then it became a matter of litigation. To remove such confusion, CBDT issued circulars to AOs. Now these are binding only to AOs and not to the assesees. The circular you stated, the one which was issued back in 2007 asked them to decide on case to case basis. This didn’t end the number of litigation in the same matter. So the option was given to the assesee to chose shares as stock in trade.

Some of the other places where option is given to the assesee.

Presumptive taxation: Now this is just an option for an assessee to show profits on Presumptive basis if they are not able to maintain the books of accounts. If they don’t opt for this the regular provisions of the Act shall be applicable.

New Tax regime: As you must be aware budget 2019 gave an option to the asseseee to choose new regime. Now if this is not chosen, then the old scheme is applicable.

Why I am stating this, even though its not really relevant in this case is because whenever an option is given, if its not chosen by default the existing provisions shall apply. And what do the provisions of the Act say? Clearly shares is included in the definition of capital Asset.

And to restate, for me as an assesee only provisions of the Act apply. Not the circulars.

Anyways, you want a second opinion from @Quicko. Lets wait for the response.