Taxes can eat into your annual earnings. To counter this, tax planning is a legitimate way of reducing your tax liabilities in any given financial year. The definition of tax planning is quite simple. It is the analysis of one’s financial situation from the tax efficiency point of view.

Tax planning is a focal part of financial planning. It ensures savings on taxes while simultaneously conforming to the legal obligations and requirements of the Income Tax Act, 1961. The primary concept of tax planning is to save money and mitigate one’s tax burden.

Couple of years back, I had written a post on how to convert FNO profit to STCG. Few of the members here actually used it and also sent me a DM. Here is the link in case you have missed it.

The response that I got motivated me to share another such idea which I personally use.

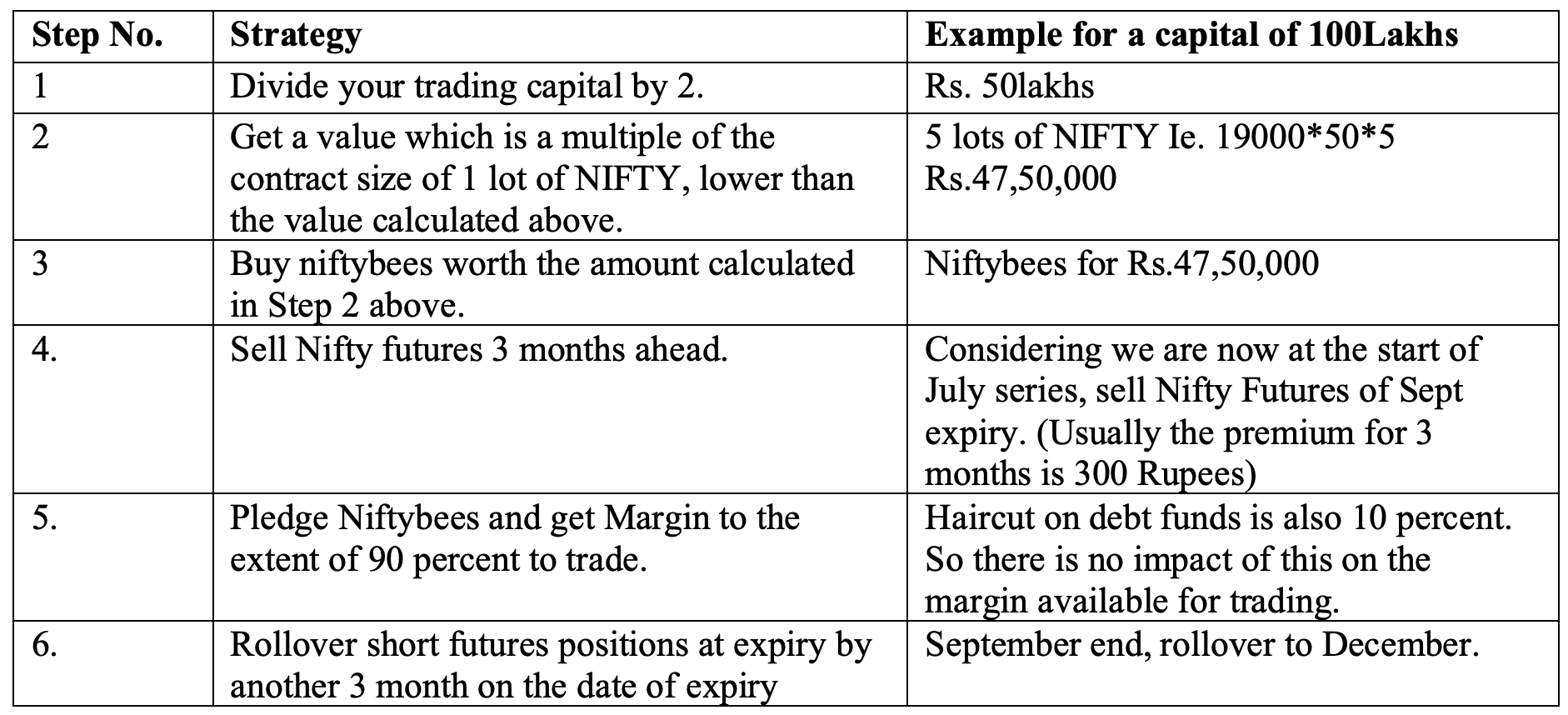

I am primarily an option seller in equity derivative segment. Before the recent changes on the taxation of debt funds where the indexation benefit was revoked, I used to buy debt funds and then pledge them to meet the margin requirements. My cash component included funds like money market, liquid, gilt, SGB and liquidbees. Also non cash component was mainly covered by the pledge of PSU banking, corporate bonds and credit risk funds. Debt funds under non cash category usually gives a return of 7 percent per annum. After the recent amendment, I had to reconsider buying debt funds at least in non cash category, since at the time of redemption the gains would be taxed as STCG. I have now developed a strategy which beats the mark of 7% return for non cash category.

The strategy shall hold good only if you meet the below mentioned assumption.

- Trade in derivatives which requires margin. I.e. Futures or short on options.

- Currently buying debt funds and then pledging them to meet margin requirements.

- Generating profits on annual basis and is subject to a minimum of 30 percent tax rate.

- Account size is more than the value of 2 lots of nifty. I.e. for the current level of nifty of 19000, the value of the account should be at least 19 lakhs.

- Nifty gives an annual return of 10percent.

Strategy: For a capital of 100 lakhs considering nifty level of 19000.

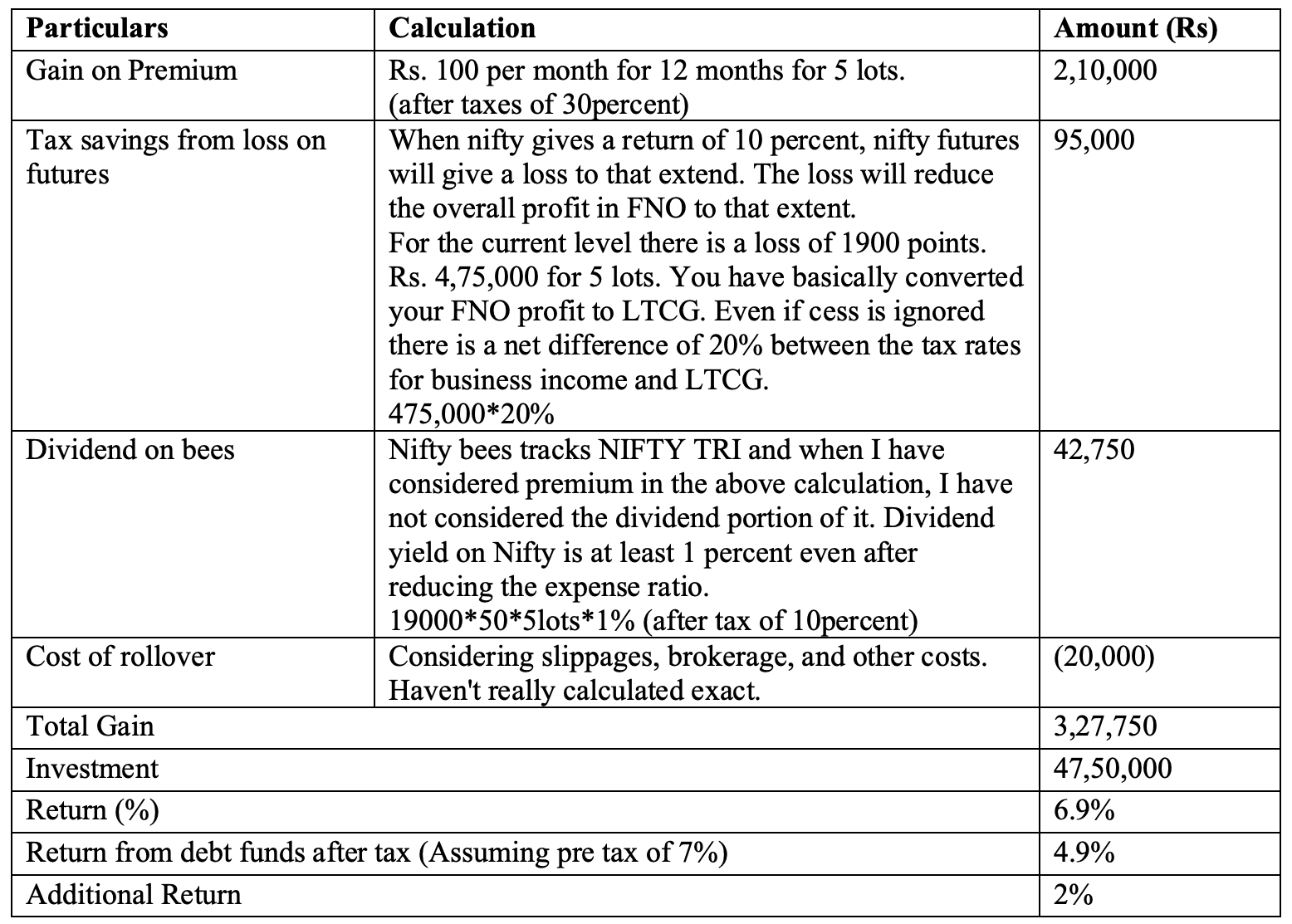

Impact of the strategy: Even though Nifty and nifty futures are supposed to move with a correlation of 1, there is a small difference in the form of premium because of the time value. Assuming after a year this arrangement is closed, this is how the returns look like. Difference between these two is our return.

Limitations:

- I have tried to be as conservative as possible. But then assumption of 10 percent return may not hold good for certain years. But over a period of time it should work.

- Nifty futures may trade at discount sometimes.

- If the timing of implementing this strategy is not right and nifty takes a temporary dip, the collateral margin reduces. This wouldn’t have been the case if debt funds were bought as usually capital value doesn’t come down. This will eventually nullify over the years once nifty outperforms debt funds.

Conclusion:

I have tried to cover everything as much as possible and keep it simple. But there is every chance that I have missed out something. Please feel free to give out our observations, so that I can optimise my strategy. I have been personally using this for over a year even before the tax amendments. But after such amendments, the gap in returns have widened.

Edit: Added limitation number 3 as noted by @Chetan_Nahata