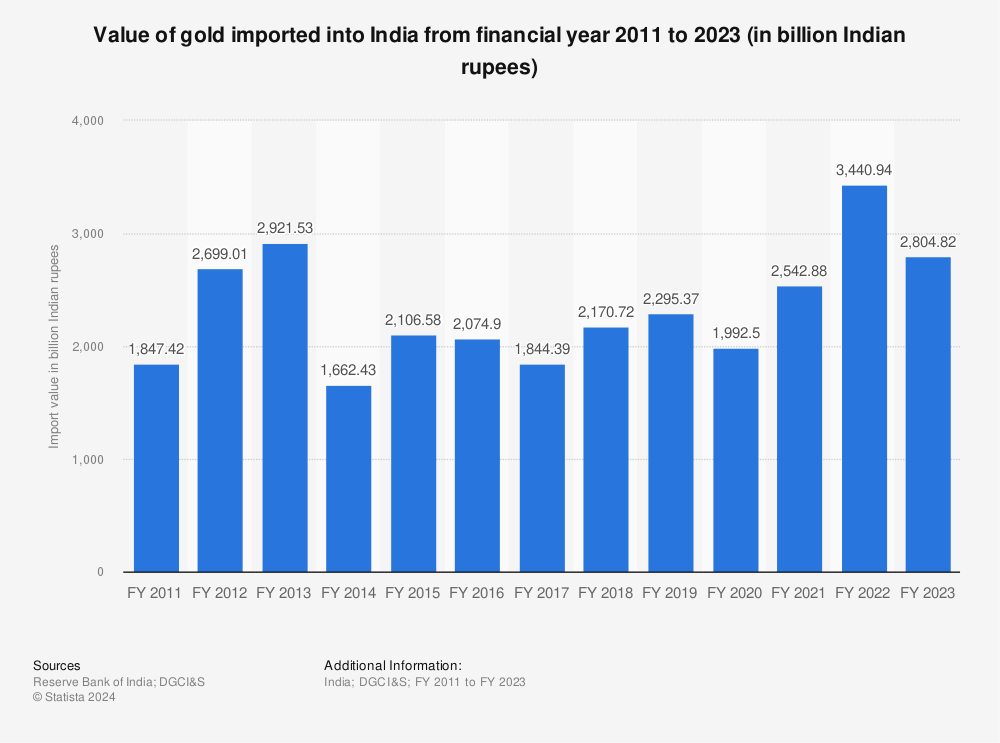

That comparision doesn’t really explain much

as the demand for gold during 2015-2022 in the absence of SGB is not known.

Sure, it can be estimated/forecasted based on historical demand for gold before 2015,

IMHO, such a forecast is unlikely to be accurate due to the unforeseen circumstances (geo-political unrest, pandemic, lockdowns, AI-boom, …) over the past few years.

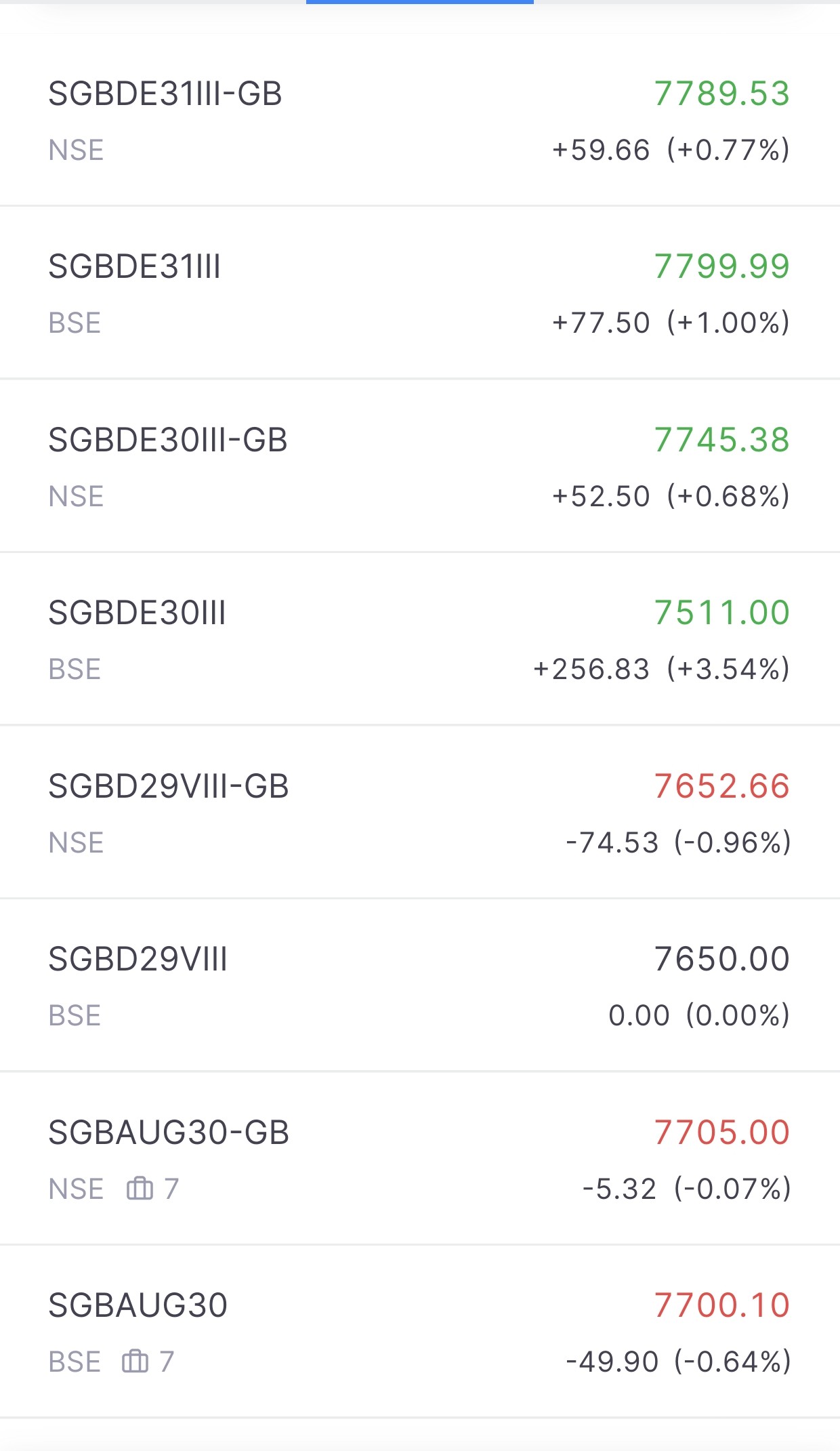

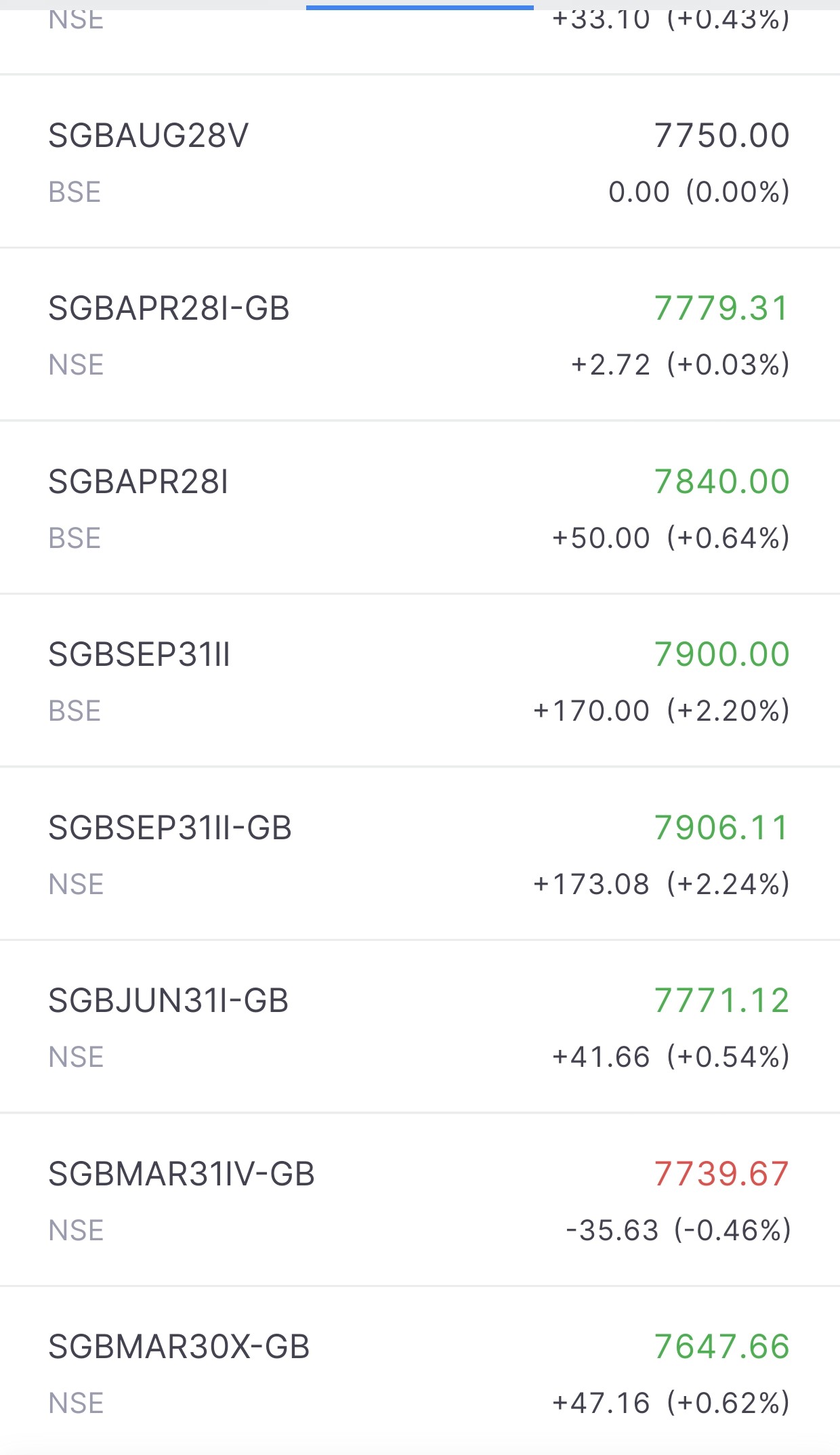

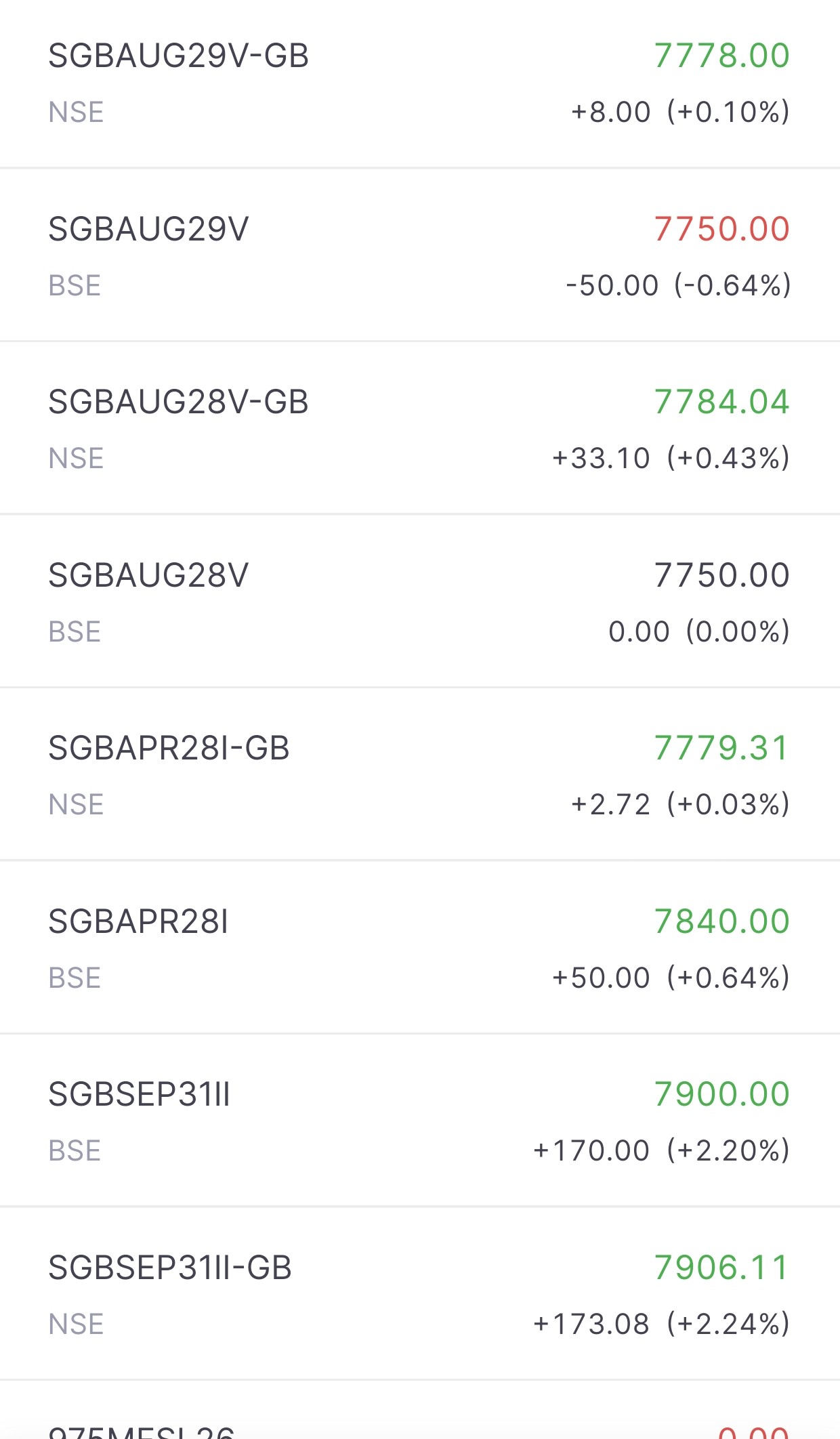

You can find quite a few details in the RBI circulars on SGB.

(eg. the data release on SGB.)

The Bonds bear interest at the rate of 2.50 per cent (fixed rate) per annum on the amount of initial investment.

Interest will be credited semi-annually

The bonds offer 2.5% / annum now (not the 2.75% / annum of the initial tranche).

So, that needs to be factored into the calculations to evaluate the current SGBs.

Interest @2.75% every 6 months = 36.91 x 16 = 590.56

More importantly, this calculation looks incorrect.

Note that even though the interest payment is semi-annual (every 6 months),

the interest quoted in for the whole year (not every 6months).

i.e. half of the annual interest is paid out every 6 months.

Headline Return 128.46%

This is simply based on the capital-gains due to appreciation of Gold over the past 8 years.

This excludes the returns from interest.

This gain due to appreciation of the price of gold

wasn’t something that was known upfront,

nor was/is it guaranteed.

This return of 128.46% over 8 years amounts to 10.88% compounded annually.

(…and the additional semi-annual interest payments

are the additional fixed-returns available on SGBs

apart from the variable gain/loss due to price of gold)

Regarding SGBs, here’s another question that comes to mind -

How is it decided when to issue a new tranche/series of SGB ?