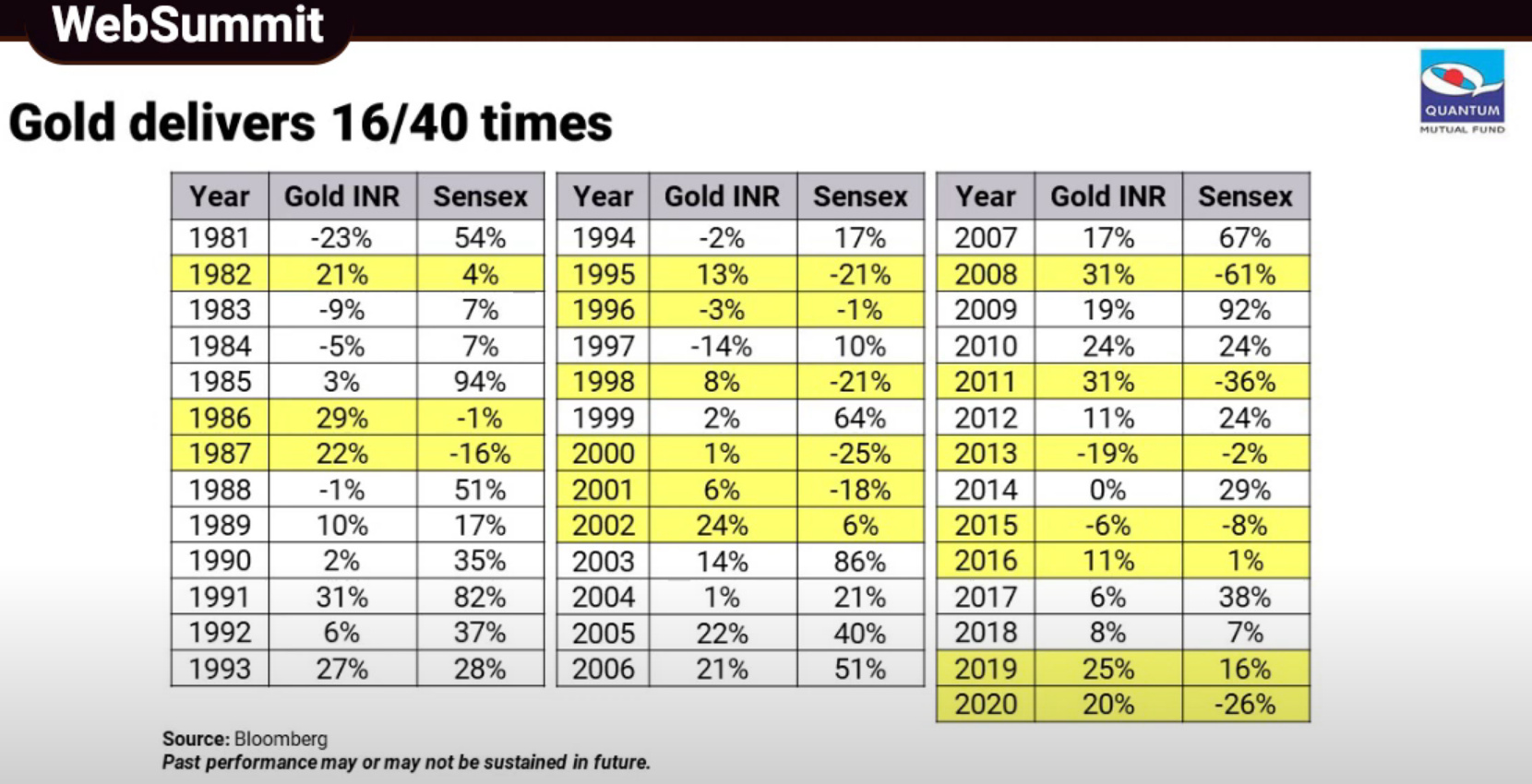

Indians love their gold. According to a World Gold Council estimate Indians held between 23,000 to 24,000 tons of gold, a majority of it with Indian households. Indians have an emotional attachment with the yellow metal, it’s a significant part of everything from weddings to festivals. For most Indians, gold along with real estate have been the most popular investment options with jewellery being the most common option.

Off late other options like Gold ETFs, Digital gold through various online platforms and Sovereign gold bonds are becoming popular. Courtesy of the recent spike in gold prices, ETF holdings of gold have reached an all-time high of over 24 tonnes. But most investors just think of access to gold as an investment option without fully realizing the advantages and disadvantages of each option.

So, in this post, I’ll briefly cover the various gold investment options, which will also let you know why SGB and followed by Gold ETFs/MF are the best instruments if you are looking at gold as an investment option.

1. Digital gold

This mode has become quite popular thanks to all the wallets and payment options. These apps advertise the fact that you can start investing in gold for as little as Rs 1. But are you getting a good deal? Let’s compare.

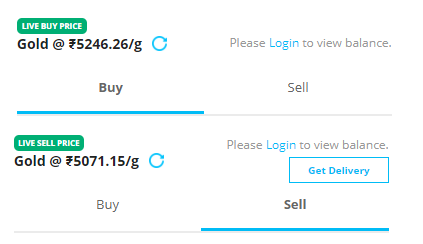

What most people don’t realize that when you buy digital gold a GST of 3% is levied, so straight away you are down by 3%. And then each provider will have his commissions and spreads. Here are the latest buy and sell prices on some of the popular platforms. For comparison, the spot price of gold as of Friday was Rs 5104 per gram.

The total spread between buy and sell works out to anywhere between 3.5% to 7% depending on the platform you use. This is a terrible deal no matter how you look at it. And then there’s the question of safety. These digital gold platforms aren’t really regulated by anyone and assuming that something goes wrong, it is not clear what the recourse for investors is.

2. Sovereign gold bonds (SGBs)

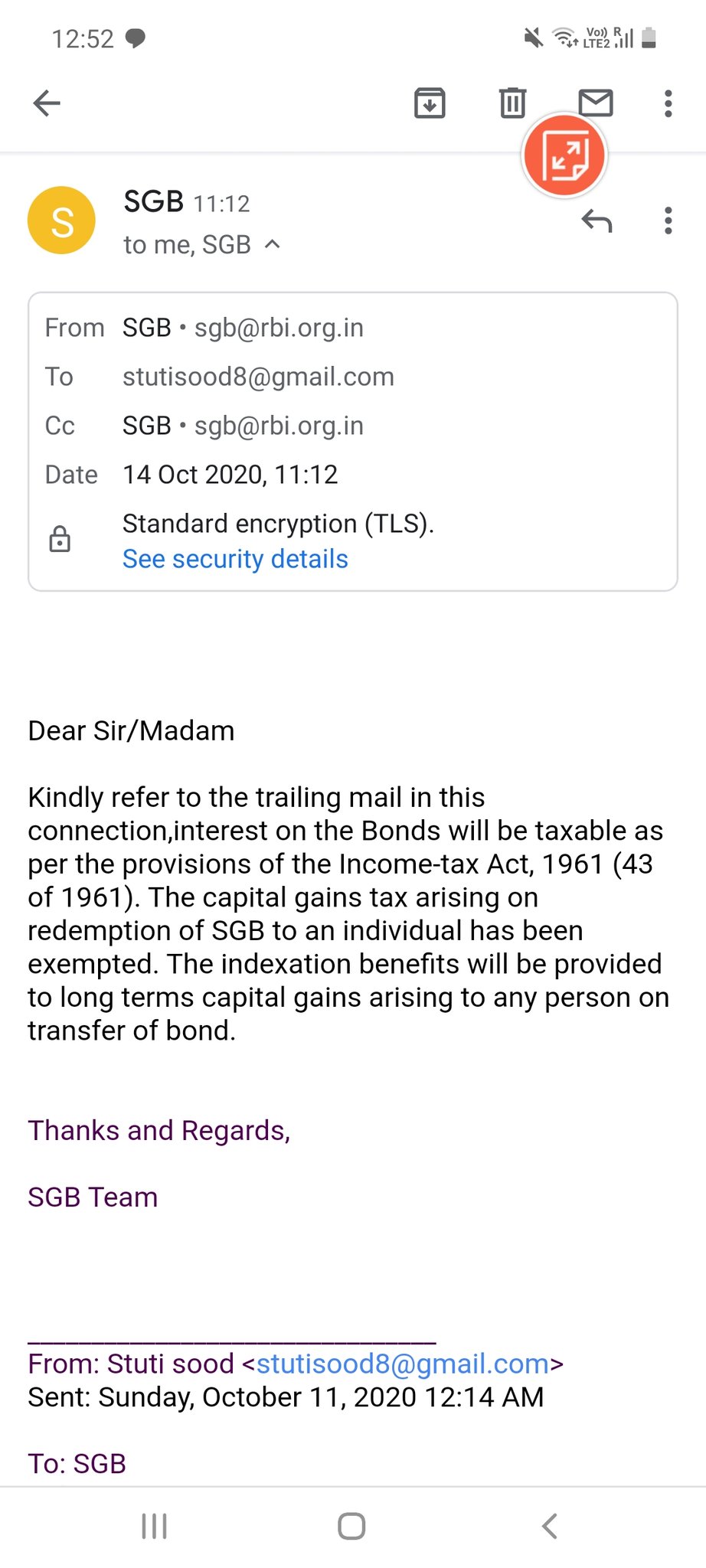

Undoubtedly, the best way to invest in gold bonds and here’s why. When you invest in gold bonds, you get a 2,5% interest every year. You are getting paid for holding gold. And then you don’t pay any GST, commissions, expense ratios etc. Not just that, if you buy gold bonds during the issuance and hold till maturity of 8 years, you don’t have to pay any capital gains. And when you buy gold bonds online, you also get a Rs 50 discount, doesn’t get any better than this.

As for safety SGBs carry a sovereign guarantee - meaning they are guaranteed by the Govt of India. Doesn’t get any safer than that. And these bonds are listed, even though volumes are still picking up, you can still exit anytime you want.

3. Gold exchange traded funds (ETFs) and mutual funds

the only small disadvantage of SGBs is that the minimum investment is in multiples of 1 gram. So, if you want to invest smaller amounts, you can consider investing in Gold ETFs or gold mutual funds. These ETFs and mutual funds have share prices as low a Rs 45. But remember, you pay an expense ratio when you invest in gold ETFs, this ranges between 0.50% to 1%. But you can sleep well knowing that these products are regulated by SEBI.

4. Physical gold

This is the most popular option but also the most inefficient option. When you buy jewellery/bars as an investment option, you have to incur making charges, GST, and then you are bearing a risk when it comes to storing it. The other thing is liquidity, selling physical gold is not an easy task unlike gold bonds or ETFs.