What are the changes from Nov 26th in non F&O stocks ?

In March, SEBI bought about 4 major regulatory measure. These are explained in this post by @nithin

- Minimum margins for stocks without F&O contracts- If a stock has an intraday price range of more than 10% for 3 days in the last 1 month, the minimum margin will again be 40%. This again means a maximum intraday leverage of 2.5 times for these stocks.

This has been withdrawn. So minimum margin requirements for non-FO stocks will just be Var+ELM margins.

- Revision of MWPL for stock F&O-Stocks with high OI utilisation and/or price movement more than 15%(over the past 5 days, during March), the MWPL is cut to 50%

This has been withdrawn and pre-COVID MWPL limits will apply. The likelihood of stocks entering the ban period will reduce.

- Revised position limits for index F&O- Big traders, prop desks, FII’s, etc., bring a systemic risk to the markets in these uncertain and volatile times. SEBI has set certain position limits on index F&O contracts, to trade beyond which they would need to bring in 100% of the notional contract value in cash for being long or have stocks worth the notional value to short.

This position limit is set at Rs 500 crores of notional or contract value for futures and another Rs 500 crores for options positions (Rs 500 crores is approximately 7500 lots of Nifty at the current price). Further, this position limit is calculated on a net basis (based on risk), which means if you are long calls and long puts, your net overall position is 0 to calculate the position limit.

This measure will continue. However, this doesn’t affect retail traders.

- 15 minutes cooling-off period for F&O stocks at circuit breakers interval of 10%

This measure will continue. Probably a good thing for the markets as buying and selling activity increases at the circuit limits. Will continue to help reduce irrational moves during increased volatility.

4 Likes

@MohammedFaisal do you mind throwing more light on this

Is this based on net position? So it will be same in your example of short call and short put option, (changing long to short) ? Will that mean if you are a large entity, you will be required to give more margins (maybe full contract value) once your size grows big in case you are a seller?

@ShubhS9, can you please look this up … why does one side hedging not reduce the margin requirements?

Hey @MayankMaheshwari,

That’s correct. If the notional value of an entity’s net position in index derivatives is more than 500 Cr, they will have an additional margin requirement which will remain blocked for 1 month(this was 3 months when it was introduced in March).

This has been the reason for the lower OI at the exchanges.

1 Like

I see faisal, so this net is netting for buy/sell and put/call?

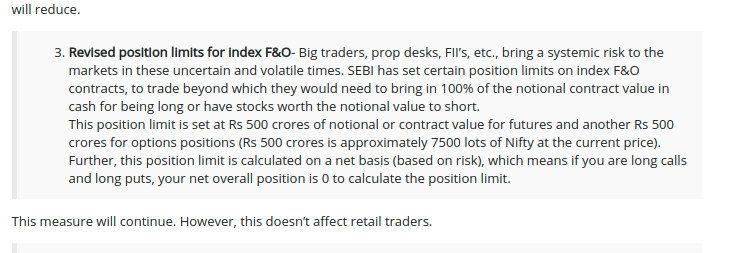

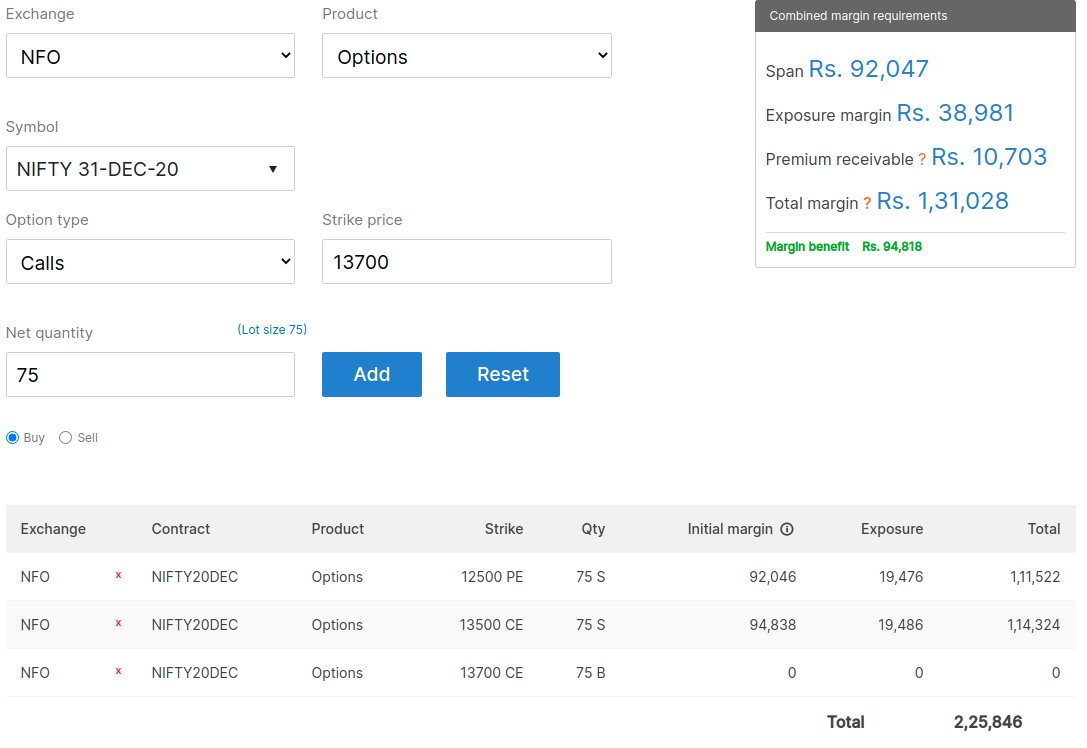

SPAN is calculated taking the max risk for the account. While one side of your position is protected, your max loss is uncapped on the other side.

Say the short Calls have a risk of 11K(as the leg is protected), the short Puts carry unlimited risk and 1 day risk will be 92K. So higher of the 2, 92K is considered.

3 Likes

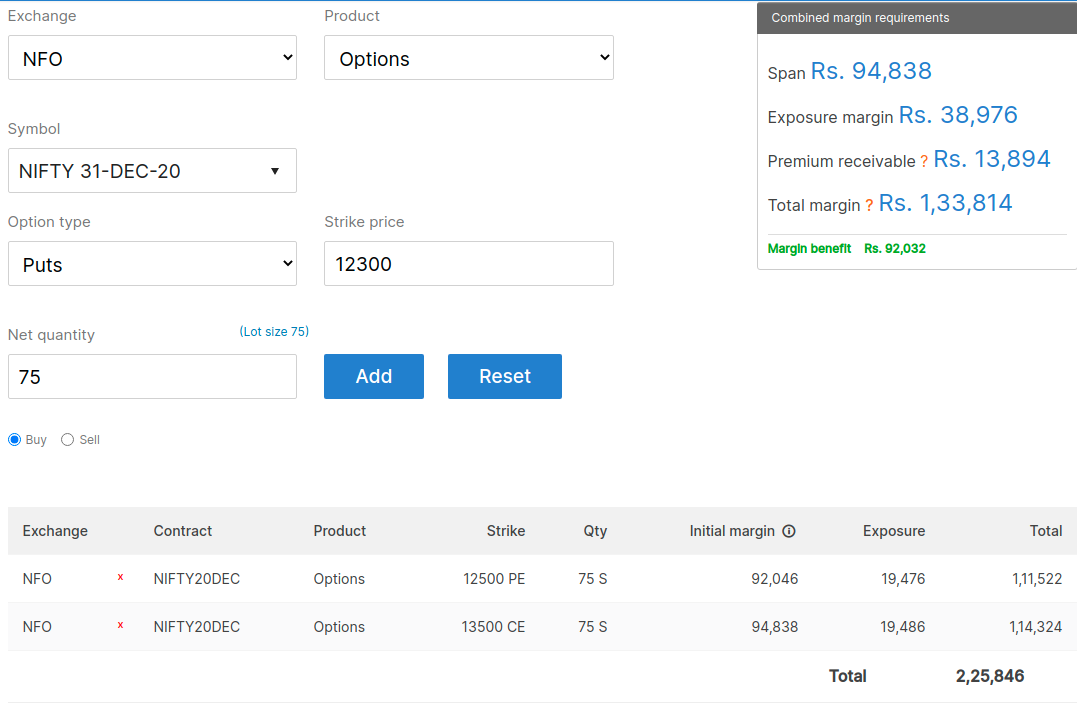

ah… on mis orders, if we create an iron condor, will be get even more margin?

So here an iron condor gave me 3 times leverage to one naked short postion,

1 short naked option margin required was about 1.3L.

Hedged naked option margin is about 40k, both nrml (long and short).

Now 1 short naked option margin as MIS is 33k.

If i hedge it with a buy option will my margin requirement go further down from 33k?

If we hedge it using NRML or MIS buy order does that make a difference?

It can go down, you can add these positions to Basket under MIS and check the margin requirments., though there might not be much difference.

cool will try and check, will basket order include my existing postions?

There is an option provided to include existing positions.