Welcome to the midweek edition of The Long and the Short—where you get an honest take on trading, something you won’t hear elsewhere. I’m Sandeep Rao.

Earlier this July, a headline set off shockwaves in a very small corner of Indian markets. A US-based quant trading firm, Jane Street, was accused of manipulating the Bank Nifty index.

For most people, it was just another market story. But for derivatives traders in India, it felt like a rule shock—and a reminder that somewhere behind the regular broker apps, there are players operating at a completely different speed and scale—and may be impacting the trades taken by retail traders.

Jane Street has denied the allegations, though. It regained access to the Indian market after depositing the penalty amount and has also filed an appeal with the Securities Appellate Tribunal (SAT) in September, seeking additional data and documents.

But this newsletter is not about who’s right or wrong or Jane Street specifically. This episode is about firms like Jane Street, and a handful of others, who operate in the world of high-frequency trading—HFT firms, as they are called.

Firms that fire off millions of buy and sell orders in seconds, capture tiny profits from the order book, and add them up over thousands of trades. They co-locate next to exchange servers, live in microseconds, and make their money in the gaps most of us never even see on the screen.

Who are these firms? What exactly do they do? And what does their presence mean for everyone else—from intraday traders to long-term investors?

The Origin Story: From Black Monday to SOES Bandits

Like I always do, let’s start with the origin story. Where did HFT—high-frequency trading—actually come from?

To answer that, we have to start with a really bad day on Wall Street. The day was October 19th, 1987—now known as Black Monday—when the Dow Jones fell about 23% in a single day. Prices were collapsing so fast that the human market makers on the floor just stopped picking up the phone. If you were a regular investor trying to get out, you were basically stuck watching your portfolio melt while nobody answered your call.

If you ask me what caused that crash, there’s no one singular reason. It was an ugly combination of overvalued markets, nervous sentiment, and computer-driven selling all kicking in together, turning a normal correction into a full-blown cascade.

In the aftermath, regulators and exchanges realised something: relying on humans to manually answer phones and trade, especially during a panic, was a structurally bad idea. So NASDAQ tweaked an existing system called the Small Order Execution System—SOES. They made it mandatory for market makers to instantly execute small electronic orders, typically 1,000 shares or less. Retail-sized orders got automatic, priority execution; the big institutional blocks would have to wait their turn.

The Birth of SOES Bandits

This is when a tiny group of very sharp traders saw an opportunity. If small electronic orders get priority and instant fills, then whoever can react fastest to changing quotes can hit those prices before everyone else.

These traders started zipping in and out of stocks all day using the SOES system, scalping tiny profits over and over all through the day. They became known as the “SOES bandits”—and they’re basically the grandparents of modern-day HFT: speed, tiny edge, repeated thousands of times, but all done manually.

One of the most famous bandits was Harvey Houtkin, who ran a firm called All-Tech. He started teaching this style of trading, opening rooms full of screens where people did nothing but hammer trades all day on SOES.

The Rise of ECNs

Around the same time, another interesting story was unfolding. Gerald Putnam, who ran a small brokerage called Terra Nova, opened SOES trading rooms around the US. To save money on expensive NASDAQ terminals, he routed all those branch orders over the internet into a central hub in Chicago. That setup gave him an idea: “If I’m already routing and netting all these orders centrally, why can’t I just match some of them internally with a computer?”

That was in a way the first ECN—an electronic communications network—where a matching engine pairs buyers and sellers automatically.

Meanwhile, at a firm called Datek Securities in New York, two young techies, Jeff Citron and Josh Levine, were pushing this innovation even further. They built a trading system called Watcher that supercharged SOES trading. It lets day traders fire orders at insane speed compared to everyone else. As their flow grew, they realised they could often match trades against each other electronically—and out of that came The Island, one of the earliest and fastest ECNs on Wall Street.

The island became known for its blazing-fast matching engine. It started quietly eating into NASDAQ’s business because traders loved how quickly and cleanly it executed orders.

Gerald Putnam saw this, took the ECN idea, and went one step further. He launched Archipelago, another ECN, and wired it to not just match trades internally but also intelligently route orders out to other exchange venues if there was no internal match. That was the birth of the “smart order router”—a piece of software that looks across multiple markets or exchanges in real-time and decides where to send your order for the best execution.

The Perfect Storm: Rules and Decimalization

So now you have: SOES bandits making money with speed, ECNs like Island and Archipelago matching orders electronically, and smart order routers stitching together multiple markets and exchanges.

In the late ‘90s and early 2000s, a couple of things poured rocket fuel on this setup. First, new rules forced exchanges to display ECN quotes right next to traditional market makers. Suddenly, these electronic venues were first-class citizens.

Second, decimalization in 2000 shrank tick sizes to one cent. Spreads got tighter, traditional market-making became less profitable for humans, and suddenly it made a lot more sense to let ultra-fast computers fight over those tiny, fractional edges instead.

By the mid-2000s, the big exchanges basically conceded that the future was electronic. NASDAQ bought the technology behind Island, the NYSE bought Archipelago, and those matching engines became the core of what these exchanges run on today. Alongside them grew a new class of firms whose whole business model was: see the market a little faster, react a little faster, and capture a tiny bit of edge thousands of times a day.

Those were the high-frequency trading firms, Tower and Getco being the early ones.

HFT Comes to India

India’s HFT story begins a bit later. SEBI opened the door to algorithmic trading around 2008; NSE rolled out co-location around 2010, letting firms park their servers right next to the exchange’s machines. From there, the same pattern plays out: more automation, more ECN-style matching, more emphasis on latency and order-flow intelligence, and a gradual rise of HFT-style strategies in our own markets.

So HFT started with a market crash in the US that broke the old manual system, then a small group of traders using SOES a bit more cleverly than everyone else, then ECNs like Island and Archipelago wiring those trades into ultra-fast matching engines, and finally, an arms race of speed, smart routing, and automation.

That’s the origin story of high-frequency trading—from SOES bandits on clunky terminals to co-located servers fighting over microseconds.

What Exactly is High-Frequency Trading?

Well, there are two ways to look at it. There’s the generic, conceptual definition, and then there’s the regulatory definition. Let me walk you through both.

The Conceptual Definition

First, conceptually, high-frequency trading is just algorithmic trading done at extreme speed and scale. There is code that reads market data in real time, makes decisions in microseconds or milliseconds, and sends loads of orders and cancellations throughout the day.

The edges are tiny—maybe a few paise, a tick, or a fraction of a tick—but the game is to do this thousands or millions of times. HFT firms invest heavily in speed: co-location next to the exchange, super-optimised code, fast networks, sometimes even specialised hardware. Their business model depends on being faster than others by tiny but consistent margins.

The Regulatory View

In India, SEBI treats HFT as a latency-sensitive, high-intensity subset of algorithmic trading—the kind that runs through DMA and co-location, fires a large number of orders per second, and shows very high order-to-trade ratios. It sits inside the broader “algo trading” bucket, but behaves differently enough that SEBI can place extra controls around it.

That’s why SEBI keeps an eye on both speed and order intensity: it allows exchanges to cap orders-per-second (OPS) for algos (for example, around 100–120 OPS in some segments), and it actively monitors order-to-trade ratios (OTR).

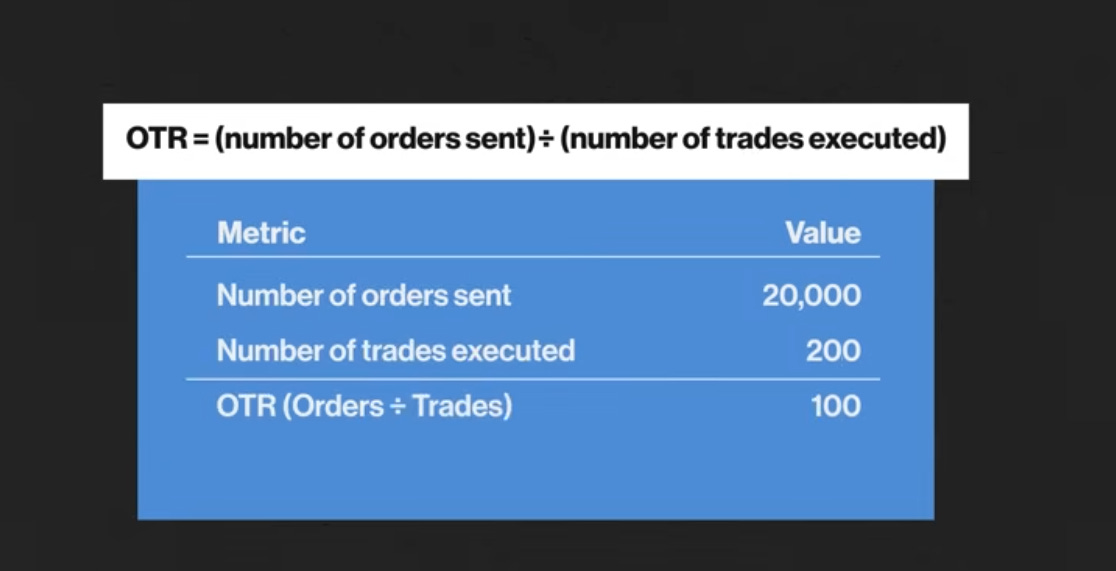

Understanding OTR

Now you may ask what OTR is. Order-to-Trade Ratio, or OTR, is simply the ratio of how many orders you send to the exchange versus how many of those orders actually turn into trades.

In formula form, it’s: OTR = (number of orders sent) ÷ (number of trades executed)

For example, if in one day you send 20,000 orders and only 200 of them get filled, then your OTR is 20,000 ÷ 200 = 100.

So, OPS and OTR are the two factors that SEBI monitors. And this is how HFTs are defined by the regulator.

What Do HFT Firms Actually Trade?

So far, we’ve understood how HFTs started and what actually defines them. The next obvious question is: what do these firms actually trade, and how is that changing in India right now?

At a high level, most HFT desks—in India and globally—run some mix of market making, different kinds of arbitrage, and very short-term, order-book-driven strategies. The common thread is always the same: they’re not trying to predict the next trend; they’re trying to capture tiny, repeatable edges over and over again, with very short holding periods.

Market Making

A big chunk of HFT activity in India is classic market making—being the “plumbing” of the market while providing liquidity. These firms continuously post both buy and sell quotes on instruments like index futures, stock futures, options, and sometimes even less liquid names.

The goal is to buy a bit cheaper, sell a bit higher, keep positions small, and turn inventory very quickly. They earn the bid–ask spread and small pricing edges, but do it thousands of times a day. Global players like Citadel, and Indian shops like AlphaGrep or Graviton, all have some flavour of this: a core of market making, arbitrage, and cash–futures arbitrage running at high speed.

Statistical Arbitrage

Then there’s something called statistical arbitrage, which focuses on price relationships rather than single instrument prices. In cash–futures arb, traders watch the gap between a stock or index and its future; if the future is too overpriced or too discounted versus spot plus carry, the algo buys one leg and sells the other, waiting for them to converge.

In statistical arbitrage, models track how related instruments normally move together—stock vs sector, index vs ETF, different expiries, options vs futures, even cross-asset spreads—and step in when those relationships drift slightly out of line: buy the discounted side, sell the overpriced side. Some of these models can be extremely complex, with hundreds or even thousands of variables driving decisions.

On top of that, you have cross-venue arb across exchanges. In India, we have NSE and BSE, where the same product trades on multiple venues; if one exchange updates a price a few microseconds earlier than another, a fast HFT can hit the stale quote on the slower exchange and lock in a tiny, low-risk edge. That’s the pure speed game.

Order-Book and Microstructure Strategies

Another big bucket is order-book and microstructure strategies, which live deep inside the order matching engine. These strategies care a lot about where you sit in the orderbook queue: are you first in line at the best price, or fifth?

The algos continuously place, move, and cancel orders to stay near the front, and they watch the pattern of incoming orders to infer when a big player might be about to trade. Holding times here are extremely short—milliseconds to seconds. This isn’t “I’m bullish Bank Nifty for the next hour,” it’s “I want to be first in line for the next few ticks, and I’ll adjust as the order flow changes.”

Options Trading

Options are another area HFTs love, especially in India. For years, a huge chunk of high-frequency activity has been in index options, weekly expiries, and expiry-day trades—effectively our desi version of 0DTE options.

Options are attractive because they move fast, spreads are tight but active, and you can hedge risk dynamically with futures or cash. HFT desks run options market-making strategies, quoting calls and puts across multiple strikes and expiries; volatility-arbitrage strategies, trading mis-priced implied vol; and complex hedging engines that continuously rebalance risk in small, rapid adjustments rather than big directional bets.

A lot of the “Thursday madness” in Indian markets over the last few years has been driven by these expiry-day, microsecond options strategies.

Mid-Frequency Strategies

Not everything inside a quant or HFT firm is ultra-low latency, though. There’s also a large and growing bucket of systematic intraday or mid-frequency strategies. These trade on one-minute, five-minute, or even longer timeframes are fully systematic and data-driven, but are less obsessed with shaving off every microsecond.

Many smaller players in India live in this “mid-frequency” space: they still run systematic models, often on index futures or baskets of stocks, but without the heavy hardware and network spend that true high-frequency requires.

The Changing Landscape

Interestingly, what’s changing now is the mix. After SEBI’s crackdown on India’s once-frenzied weekly index options market, exposure caps, restrictions on expiries, real-time surveillance, and a sharp drop in index-options turnover have all put pressure on the old “pure expiry-day, microsecond options churn” model.

The investigation into Jane Street and the broader tightening around derivatives has pushed India’s HFTs to re-look at their businesses. Firms like AlphaGrep, Graviton, Quadeye, and iRage are still running ultra-low-latency systems, but they’re also building slower, more data-driven strategies that think in minutes to hours instead of microseconds.

They’re leaning more into cash equities, longer-dated index derivatives, stock derivatives, commodities, and cross-asset trades, and they’re expanding to markets like the US, Japan, Brazil, Southeast Asia, Singapore, and Europe as a hedge against tighter rules and shrinking margins at home. Many HFTs are doing Crypto as well.

Inside many of these firms, you now effectively have two worlds: one side still focused on pure HFT—co-located, ultra-low-latency, queue-position games—and another side focused on mid-frequency and quant asset-management style strategies powered by machine-learning and richer datasets.

If you zoom out, the story is that HFT in India is evolving from a narrow focus on speed and expiry-day leverage in weekly options to a broader, multi-asset, multi-horizon quant ecosystem. The DNA is still the same—systematic, heavily engineered, cost-obsessed, and built around small, repeatable edges—but those edges increasingly live across market making, arbitrage, options, cash equities, commodities, and global markets, spread across both high-frequency and mid-frequency styles rather than just 0DTE Bank Nifty at microsecond speeds.

Who Are These Firms and How Much Do They Make?

Now that we have a sense of what strategies HFTs trade, the next question is: who are these firms, how much money do they make, and what is this business really like from the inside?

The Players

In India, the HFT world is dominated by proprietary trading firms—outfits that trade their own capital and have their own broking licence—plus a few broker-prop desks and subsidiaries of big global players.

On the homegrown side, firms like Graviton Research Capital, Quadeye, AlphaGrep, iRage, Estee Advisors, Dolat Group, NK Securities, and a handful of others form the core of the ecosystem.

Alongside them, you have the global firms. Firms like Tower Research Capital, Jump Trading, Hudson River Trading, Citadel Securities, Jane Street, and others have Indian entities or FPIs that plug into NSE and BSE using the same co-location and low-latency infra as local players. Tower was one of the earliest international HFTs in India.

Then there’s another layer: global quant asset managers and hedge funds—names like WorldQuant, Millennium, and others—who may not be doing pure microsecond HFT here, but run medium-frequency stat-arb and quant strategies into India from offshore structures.

The Infrastructure

Structurally, almost all of these have a broker membership at the exchange. The broker has two key buckets: client accounts and a proprietary (prop) account. The big HFT shops mostly use the prop account, trading their own capital; that’s partly for control, and partly for saving costs like stamp duty, etc.

They take exchange connectivity through co-location—literally renting physical space and rack units in the exchange’s data centre—and then cram those racks with custom-tuned servers, network cards, and software optimised to shave off microseconds.

The Money

So how much money do they actually make?

Let’s start with Graviton , based in Gurgaon and founded in 2014 by IIT Delhi alumni, which is often cited as the current “top dog”—Moneycontrol reports that in FY23 it did a whopping ₹3,525 crore in revenue and around ₹605 crore in net profit, purely from quant and algorithmic trading.

AlphaGrep , another Mumbai-based Quant firm, saw its net profit explode to roughly ₹207 crore in FY22, up from under ₹3 crore just a few years earlier, as revenues climbed close to ₹800 crore.

Dolat is one of the few listed names where you can actually see HFT-style profits show up in public filings. NK Securities, iRage, and Estee sit in that same cluster of highly specialised, mostly quiet, very profitable quant shops.

Jump’s India arm has scaled fast—recent regulatory data suggests revenue of well over ₹2,500 crore for FY24.

Citadel Securities has been building out in Mumbai as a global market-maker, and Jane Street , before SEBI’s interim order, is estimated to have earned billions of dollars from Indian index options over just a couple of years, with SEBI alleging roughly $567 million (around ₹4,800+ crore) in unlawful gains now locked in escrow.

The Economics

Graviton’s revenue, Jane Street’s Indian options haul, Tower’s long-running volumes—all point to a business where a handful of firms collectively turn over tens of thousands of crores and pull out serious profits if they get the tech and risk right.

But at the same time, margins have been crushed over the last decade. People inside the business will tell you: where you might have earned, say, 1 paisa on every ₹100 of turnover in 2010, you’re probably closer to a third of that today—something like 0.3 paisa—because spreads are tighter, competition is fiercer, and transaction costs plus stamp duty eat a big chunk of your edge. The game is no longer about fat spreads; it’s about huge scale and relentless cost optimisation.

The Risks

The risk side is real, too. This is a world where a bad deployment or a broken risk-check can burn crores in seconds—think of Knight Capital in the US, which famously lost hundreds of millions of dollars in under an hour due to a software glitch.

Engineering in HFTs isn’t just good infra, it’s survival. Therefore, a lot of the salary pool goes to systems, network, and hardware engineers who can keep latency low, clocks in sync, and kill-switches working. You’ll often hear numbers like upwards of a crore per annum salaries for engineering roles, and far more for top traders and partners, plus big, deferred bonus pools.

Going Global

Because margins are thinner and regulation is getting tighter, these firms have become globally focused now. Indian HFTs and quant shops now routinely run strategies across 30+ exchanges worldwide: US equities and commodities, Brazilian futures, European and Japanese markets, even crypto.

India remains attractive because of its massive derivatives volumes, but firms hedge their business risk by also making money in US commodities, Brazilian equity index futures, global FX and crypto venues, and so on. Some markets, like China, are seen as “painful” on the regulatory/operational side, while others—like US futures or certain crypto venues—can be more lucrative for the same tech stack.

The overall picture is this: India’s HFT landscape is a tight group of specialised prop firms plus a handful of global giants and bank desks, all fighting in a brutally competitive, low-margin, high-fixed-cost business.

When it works, the numbers can look absurd—thousands of crores in revenue and hundreds of crores in profit. When it doesn’t, a single bug, a single rule change from the regulator, or a sudden shift in market structure can wipe out an entire strategy line overnight.

It’s less like a gentle asset management business and more like running a high-tech, high-stakes trading factory: huge fixed costs, razor-thin unit margins, constant pressure to innovate, and a global race to find the next micro-edge before someone else does.

Are HFTs Good or Bad for India?

A question that often gets asked is: Are HFTs “good” or “bad” for India? The honest answer is: they’re a net positive in function, but sadly, they are portrayed as villains.

On the plus side, HFTs make our markets deeper and tighter—they narrow bid–ask spreads, keep quotes available almost all the time, and absorb a lot of short-term noise. If you abruptly shut them off tomorrow, volumes would drop, spreads would widen, fills would get worse, and the market would feel slower and “boring” for everyone, from intraday traders to large institutions.

Most serious HFT shops actually don’t want to “move” prices; their ideal world is lots of small, uninformed flow where they can trade in size without leaving footprints, capturing tiny, low-risk edges over and over.

So in totality, HFTs are critical market infrastructure run by profit-seeking firms, and the real question for the ecosystem is whether regulation can keep the benefits of liquidity and tight pricing while curtailing the tail risks and bad behaviour. Am I asking for too much? I don’t know. But I think it’s possible.

So that brings us to the end of this deep dive on HFTs in India. I hope you found this episode valuable.

Do share your questions, thoughts, and feedback in the comments—I’ll do my best to respond.

Thank you for watching, and see you in the next one.