To most people diversification means having multiple stocks or funds across some different sectors. If an investor is half-informed, then he’ll have an additional asset class such as debt or gold. For 99% of the investors’ diversification ends there and most often than not, there is no real thought behind why the diversification.

Well, diversification is anything but this and there is a lot more to it. I recently came across this study titled “SKIS & BIKES THE UNTOLD STORY OF DIVERSIFICATION” by Resolve Asset Management. It gives a sweeping view of diversification with some amazing data to back up each point. I highly recommend you give it a read. Here are some highlights:

The most fundamental principle of investing is diversification. But in our experience, few investors understand what diversification means. Sure, investors typically understand that diversification means “don’t put all your eggs in one basket”. Some also understand that diversification is about owning a combination of investments that zig and zag at different times. But when we probe a little deeper, it seems many investors are still confused about how diversification works in practice.

To explain the meaning of diversification, the authors use the example of Ski and Bike sales.

In most parts of Canada, we have very distinct seasons. Some months of the year are temperate and relatively dry, while other months are cold and snowy. As a result, most Canadian towns of any size have stores that sell skis and bikes. Of course, they don’t inventory both skis and bikes at the same time. Rather, in the spring they sell off all their ski related inventory and set out their bike gear, and in the fall they clear out the bike gear to make room for skis. Pretty creative, right? Let’s observe a simplified example of bike sales and ski sales over several years.

As winter approaches, ski sales accelerate while bike sales drop off. As summer approaches people stop buying skis, but ramp up their purchases of bikes. One line of business is thriving while the other is flat. In some years, winter might come late and produce very little snow, stifling ski sales.

But the subsequent spring might be warm and dry and encourage bumper bike sales. This is the

nature of diversification.

This same effect plays out in markets. Economic news that is good for one type of investment is often bad news for another. In fact, the hallmark of a diversified portfolio is the observation that one or more investments is disappointing you most of the time. A portfolio that consists of assets

that all produce gains at similar times for similar reasons will probably produce their worst losses

at the same time too.

Well executed diversification is indistinguishable from magic

In investing, it is a simple thing to build a low-risk portfolio by holding lower risk assets, like short-

term government bonds. Unfortunately, this portfolio would not be expected to generate much in he way of returns. Remember, the reason investors own higher risk assets like stocks instead of

clinging to the safety of short-term bonds or cash is that higher risk assets are expected to produce

higher returns.

In order to generate returns above cash, investors need to take on risk.

The central advantage of diversification is that it allows investors to hold many risky assets while maintaining a tolerable level of portfolio risk. But many investors express confusion about how two investments can both be expected to rise in value, even while they are uncorrelated. After all, if they are uncorrelated, shouldn’t we expect them to move in different directions?

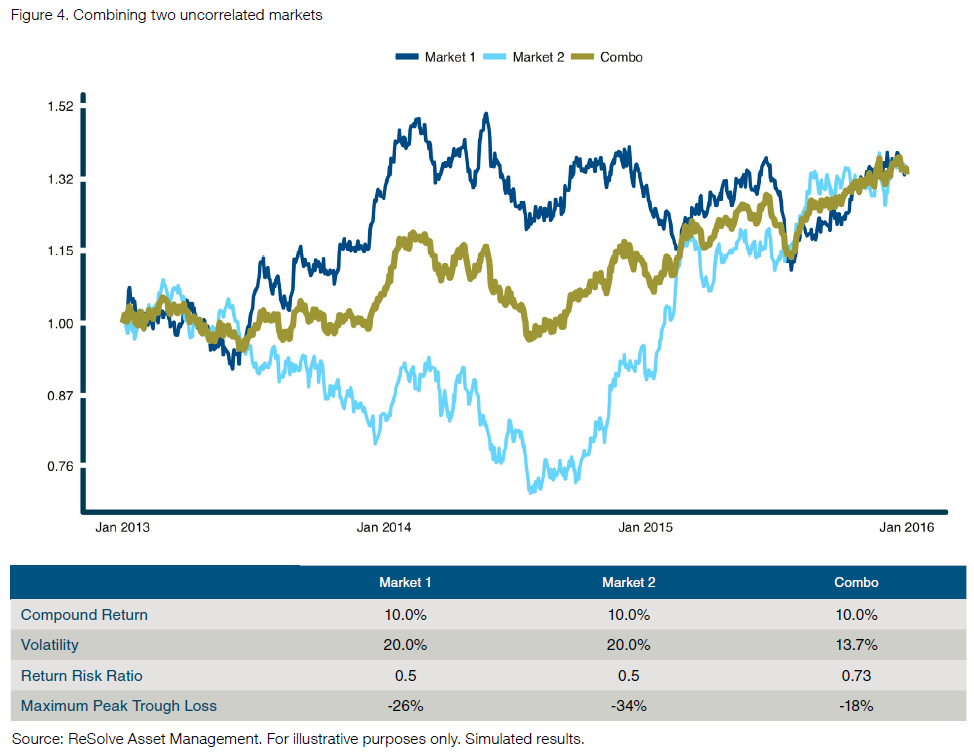

As a thought experiment, it’s interesting to see how introducing more uncorrelated investments can make the experience even smoother. For example, in the event an investor could construct five uncorrelated investments with the same 10% expected compound return and 20% volatility,

an equally weighted portfolio would have the same return, but less than half the volatility, of any of the individual investments. Even better, while the average peak-to-trough loss of each individual investment is close to 30%, the peak-to-trough loss of the portfolio is well under 10%.

Diversification in practice

Finding truly uncorrelated investments. It turns out this is harder than people think, and most investors get it wrong.

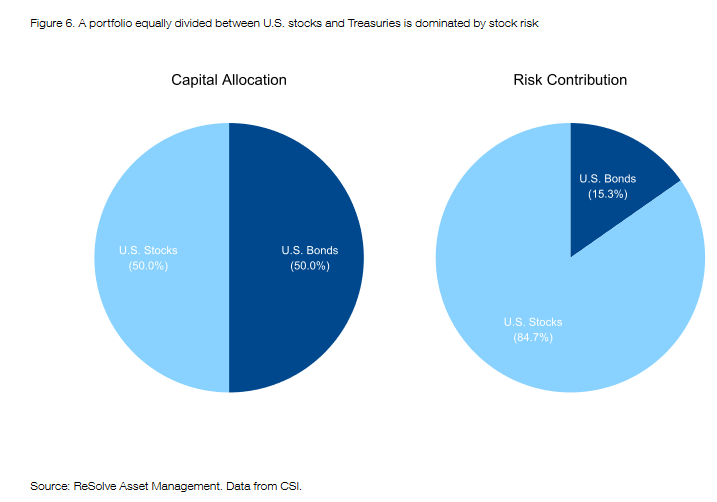

**Diversification is about balance. Unfortunately, while many investors own products that are **

**labeled “balanced”, the portfolios underlying those products are anything but. The imbalance **

**occurs because the assets in the portfolio have wildly different risk profiles. As Figure 5 shows, **

**when you hold an equal portion of stocks and bonds in a portfolio, the portfolio is completely **

dominated by stock risk, because stocks are so much more volatile than bonds.

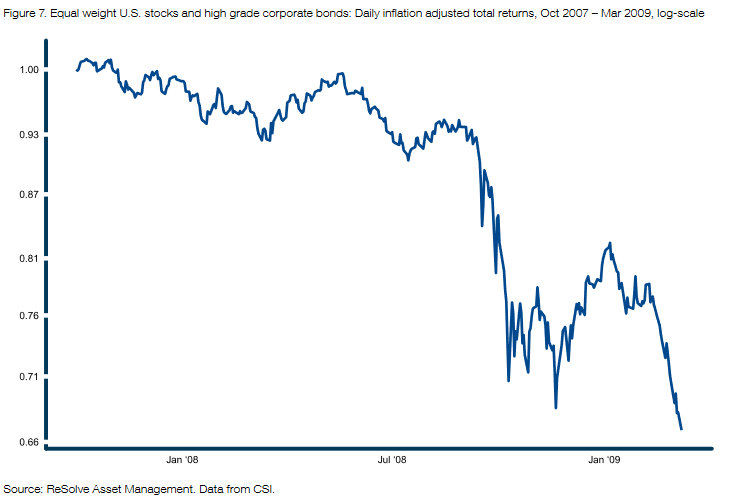

Consider the performance of this 50/50 portfolio of U.S. stocks and high-grade bonds during the global growth shock in 2008-2009 (Figure 7.).

The Global Financial Crisis of 2008 inflicted a 33% peak-to-trough loss on U.S. investors holding equal weight portfolios of high-grade bonds and stocks.

From Figure 7 it’s obvious that despite having 50% in bonds, the portfolio is almost perfectly correlated with stocks most of the time. The average correlation is .91, and the portfolio’s correlation with stocks has never dropped below 0.8 since 1993.

Diversifying

Unfortunately, most investors seek diversification in the wrong places. For example, many

investors perceive that holding many different stocks or stock mutual funds in a portfolio will

produce strong diversification benefits.

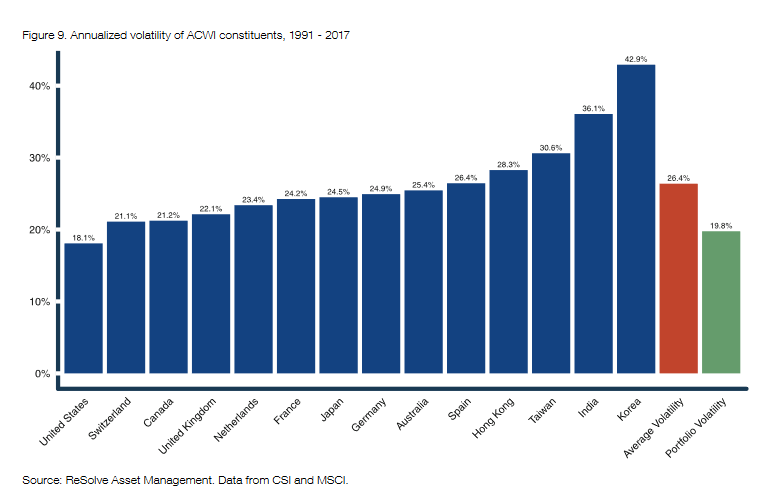

To illustrate this point, let’s examine whether we can achieve meaningful diversification by combining the 14 largest global stock markets in the MSCI All-Cap World Index (ACWI). The ACWI

is constructed to represent over 99% of total global equity market capitalization, and the 14 markets that we’ve chosen represent over 75%. (Note: we excluded China due to lack of long-term index

data).

> Remember that diversification benefits are a function of the low correlation between the assets in the portfolio. Worse, since the proliferation of index products has made it easy to invest in international markets, correlations have steadily increased.

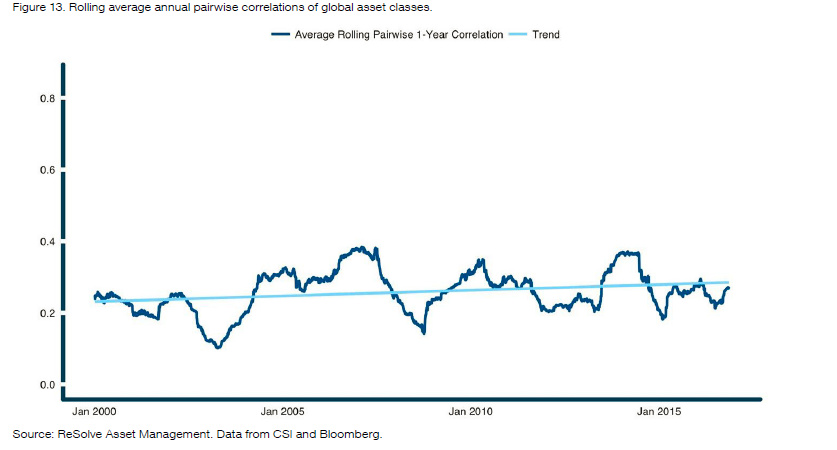

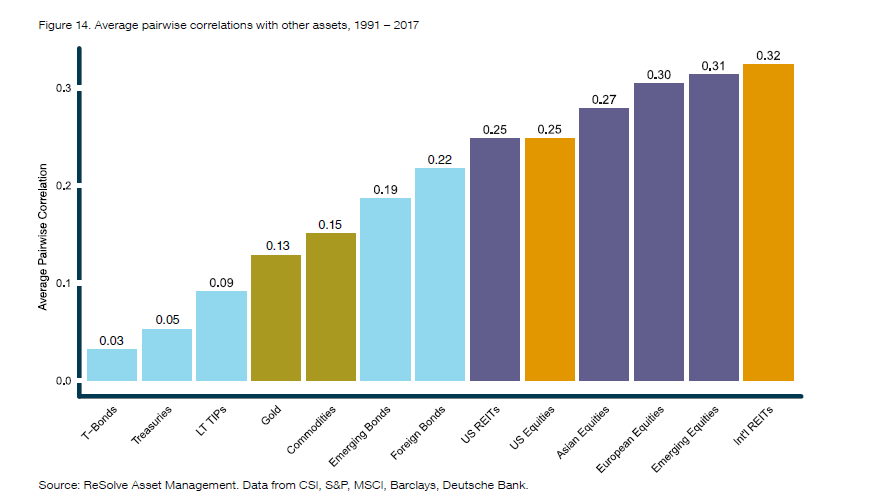

Even better, there is no reason to believe that this diversification benefit from investing in diverse

global asset classes will go away anytime soon. Figure 13 clearly shows that the average annual

pairwise correlations between these diverse asset classes have been persistently low, averaging

0.25 compared to the average 0.6 correlations across global equity markets. And, in contrast

to what we observe across global equity markets, the trend does not appear to be increasing

materially over time.

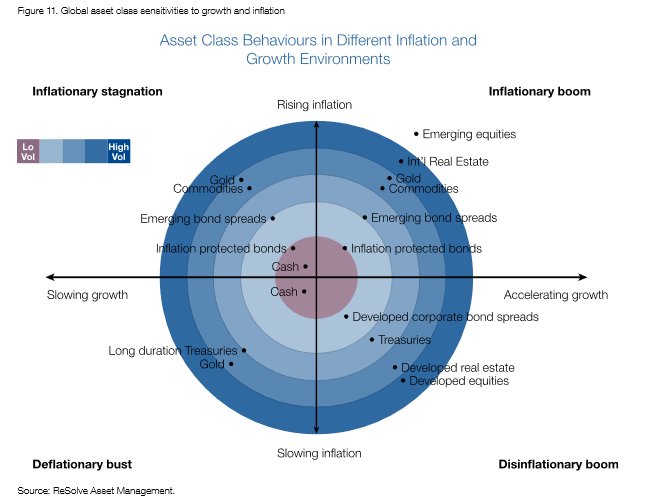

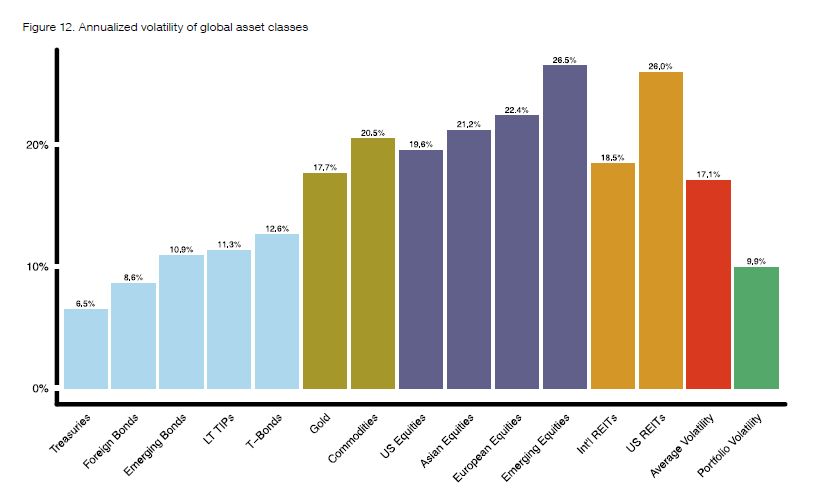

The lesson from this section is that diversification has very practical benefits, but only for

investors who can think more broadly about the world’s many sources of returns.

The research paper is quite detailed and data rich. Do check it out for a fuller picture.