Unemployment vs Inflation: Who’s the bigger loser?

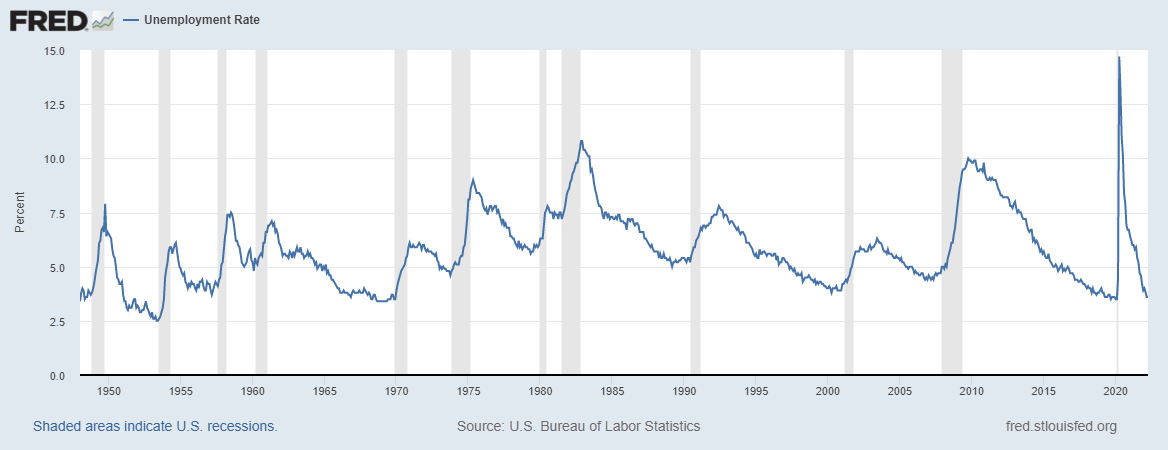

The current unemployment rate in the US is at 3.6%, which is at its fifty-year low. This paper discusses which is worse, is it unemployment, or inflation?

Ben Bernanke, the former chairman of the Federal Reserve, tried to justify why inflation is a broader concern than unemployment.

“The difference between inflation and unemployment is that inflation affects just everybody. Unemployment affects some people a lot, but most people don’t respond too much to unemployment because they’re not personally unemployed. Inflation has a social-wide kind of impact.”

Claudia Sahm, the author of this piece, discusses why she disagrees with Ben, and why both the concerns have social-wide effects.

A few pointers on the current unemployment in the US:

- Unemployment is currently 3.6% which is very close to its fifty-year low.

- Compensation from work is the key source of income, especially among middle-class families.

- A strong labor market gives workers bargaining power.

- Low unemployment is good for workers in the future.

- High inflation does not affect everybody the same.

What caught my attention in this piece was the last part, where she discusses why high inflation isn’t exactly the same for all sections of society. She references a hard-hitting paper by Matthias Doepke and Martin Schneider.

“The main losers from inflation are rich, old households, the major bondholders in the economy. The main winners are young, middle-class households with fixed-rate mortgage debt.”

What really hits you in this paper is for a person like me, it has time and again felt like inflation is the higher concern, whereas unemployment, although scary, was never on par. Both of these aspects are incredibly important concerns on the road to recovery. Although this paper is based in the US, I’d say this is the common quest the entire world is up against.

Social media is full of trading tips—but should you listen?

Social media is a source of limitless trading ideas, everyone from amateurs to professionals find ways to share information and with all this information being circulated, it’s often difficult to differentiate between credible and misleading data. Social media-driven stocks tend to only perform because of all the attention they receive, which pushes the price beyond what’s reasonable and makes it harder to identify realistic profit and loss targets.

One such example is the popular ‘pump & dump’ trend that’s been happening. Unaware influencers and popular youtube channels create a buying frenzy by advising their followers to purchase something that will “pump” up the price of a stock and then eventually have the shares of the stock “dumped” by selling it at an inflated price.

Try to keep an open mind when it comes to trying out new trading approaches, but also ensure to carry out a thorough fundamental and technical analysis whenever possible before you invest all your hard-earned money into it.

One of the latest pump & dump instances is of Lesha Industries and Vaxtex Cotfab Latest "Potential Pump and dump stocks" which are being circulated using ads in Youtube

This short but concise article explains how you can use social media to your advantage and use the information available as a catalyst for further research and not be taken as advice.

The complex economics of growing old

Life cycle hypothesis states that people make financial decisions to smooth out their consumption over a lifetime. To put it in simple terms it means that we gradually spend down our lifetime of savings in old age, smoothing our consumption until the end. But are we living out our golden years the way they are supposed to? Research says otherwise.

“People are living longer. Health issues are affecting economic outcomes, affecting medical expenses, affecting longevity”. “People are ending up in nursing homes for long periods of time and having to pay those large costs. All of this is becoming more prevalent for society and more of a risk from the standpoint of the individual.”

The following points highlight the contrasting behavior to the life cycle hypothesis:

-

Saving after retirement

-

Financial paths diverging for a couple

-

Bequest motive - Leaving it all behind for heirs or others

-

The decreasing “ability to enjoy life”

A major factor affecting the behavior is the medical expense incurred during the final stages of our lives. A survey in the USA shows that longer lives, fewer births, and falling immigration will mean that by 2035, 1 in 5 Americans will be over 65. In other words, American seniors will outnumber children. This is a common observation around the world and attracts a lot of economists for research in understanding these complex and dynamic risks we face later in life.

The following article by Jeff Horwich digs deeper into different aspects affecting the economics of our seniors and opens up a whole lot of questions for our financial planning.

—-----

Another dot-com burst?

Global tech shares have been falling since the beginning of the year. As you can see, every single one of the FAANG stocks has had a negative return. Inflation, the current Russia-Ukraine situation, or any other market chaos to be blamed.

Today, many people talk about their crypto views and say that crypto is the way of the future, even if they have no idea what it is. A similar thing happened in 1995 when people began to believe anything with a dot.com at the end of it. This is almost surely going to be the next big thing. There were exorbitant values in IPOs back then, and we’re seeing the same situation again.

Is it another dot com bubble, and are we witnessing history repeating itself? Here’s an interesting read that explores all of them.

Euphoria to Dispair

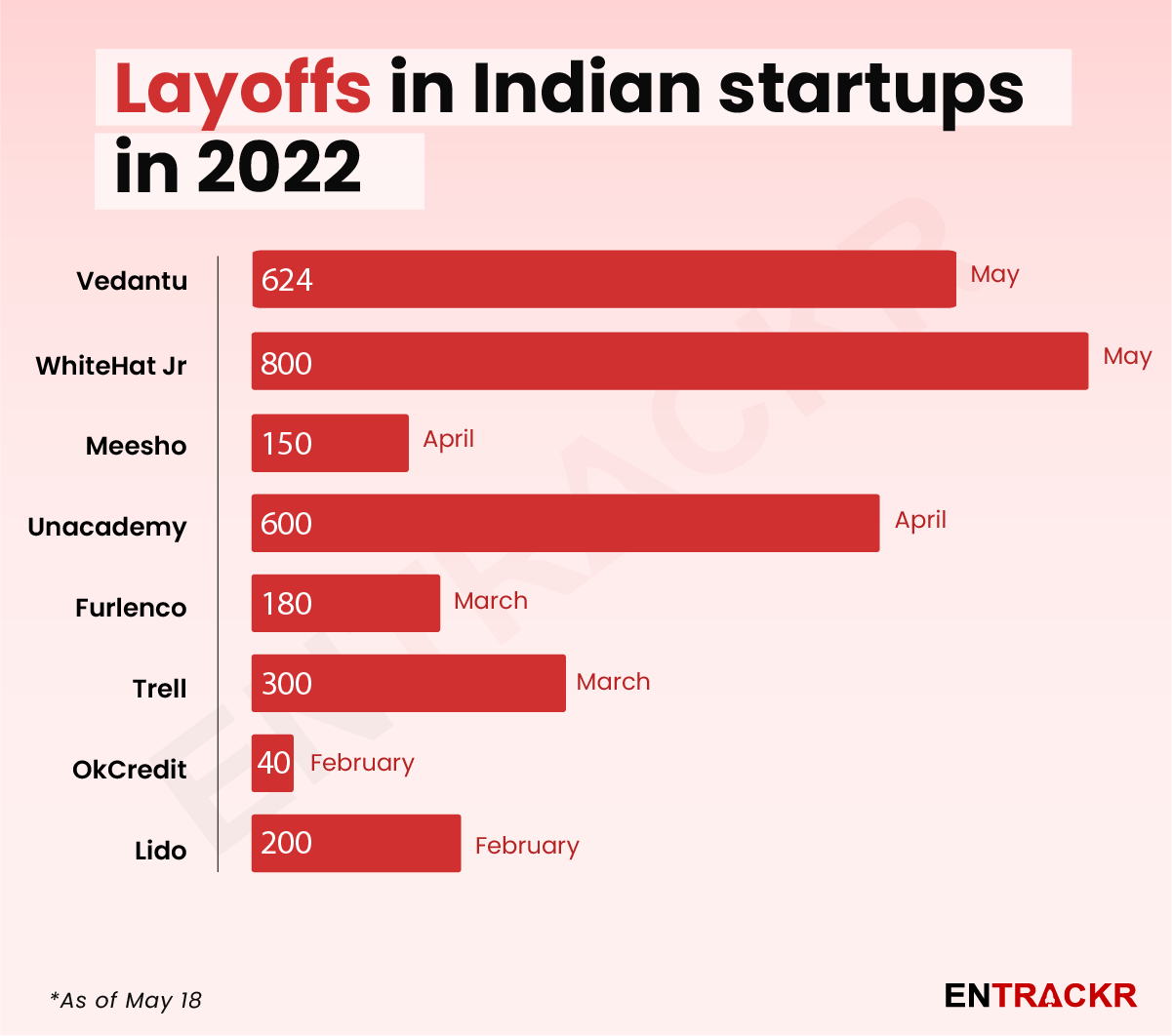

2021 was a euphoric year for start-ups around the world and in India, thanks to the central banks that pumped money into the economy to ease the impact of the pandemic, which founds its way into the financial ecosystem.

Turn to 2022 and it’s been anything but euphoric. “A spike in inflation and hike in interest rates after the abundant liquidity last year has had a knock-on effect on startup funding, as investors cut down on investments to public and private markets, allocating their money to bonds instead. Lockdowns across the world have also impacted supply chains. Add to this the Russia-Ukraine war, which has pushed up fuel prices and consequently transport costs. All around, the sentiment has turned bleak, a stark contrast to the euphoria in 2021, where Indian minted a new unicorn almost every week.”

With easy money disappearing and companies finding it hard to raise capital to fuel their growth, start-ups are now getting in cash preservation mode to sustain them in these tough times. And this has been brutal for many employees at these start-ups. We have seen some of the big start-ups such as Vedantu, Meesho, etc. cutting jobs at a rapid pace.

Finshots and MoneyControl have great write-ups on these developments ![]()

What to watch:

Deepak Parekh, chairman of HDFC Ltd. on institution building, leadership, inflation, RBI’s rate hike and the HDFC - HDFC Bank merger.