Another forum member tried asking RBI about this and they got a reply stating that the matter was referred to the Government of India

Other people have also gotten similar replies -

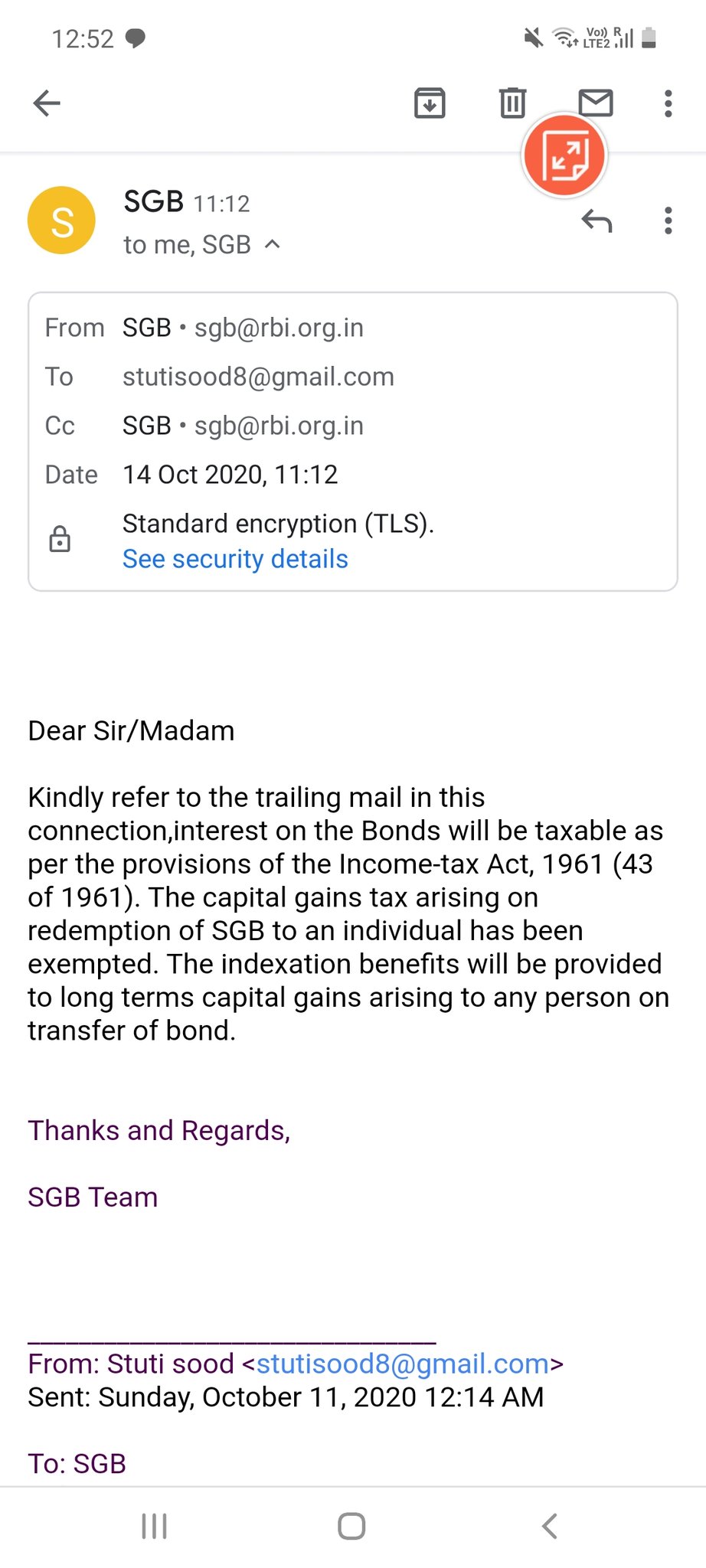

https://twitter.com/soodstuti/status/1315618609746518016

In a follow-up tweet, it has been claimed that capital gain is exempt for individuals even for secondary market purchases of SGB