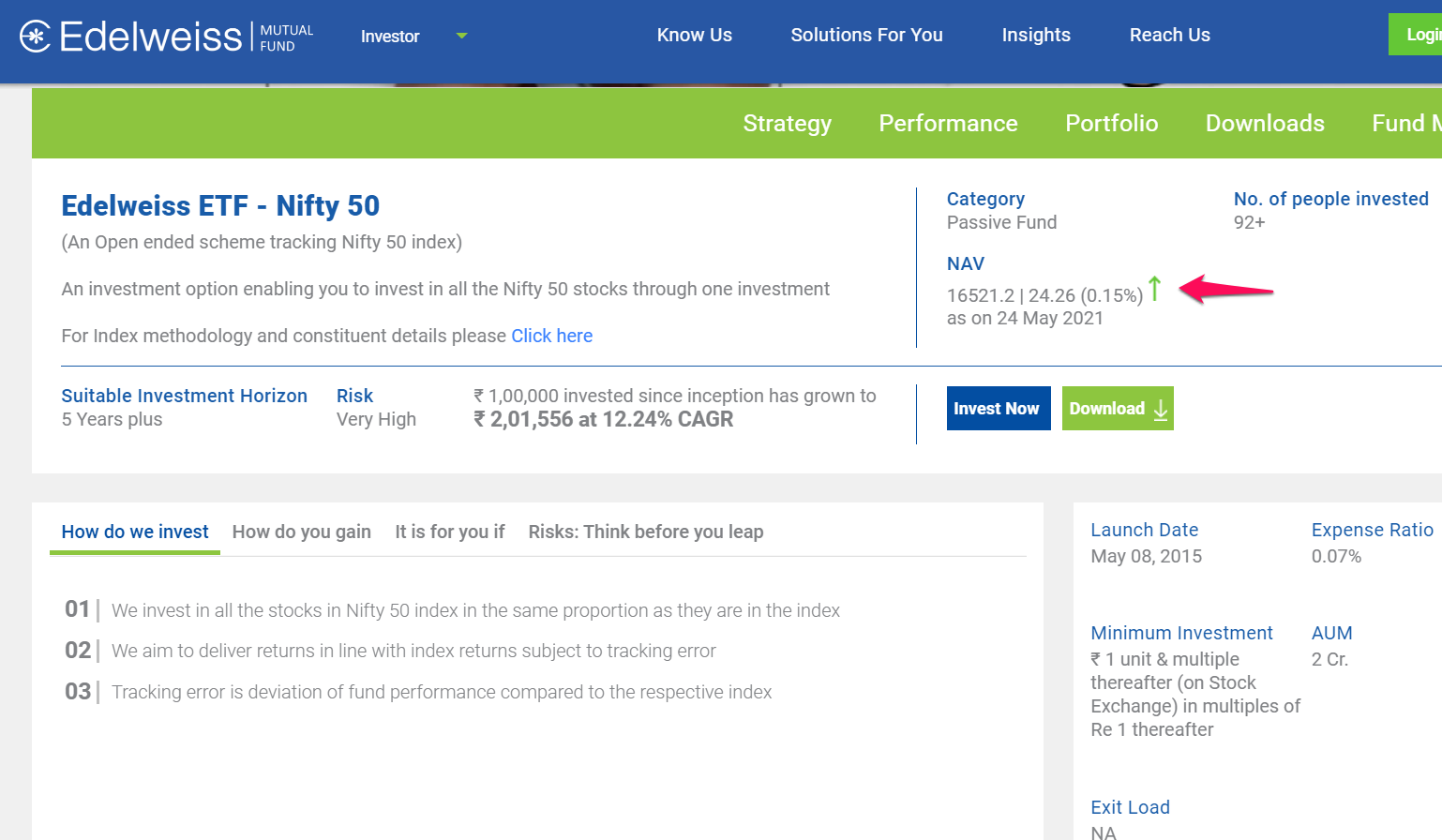

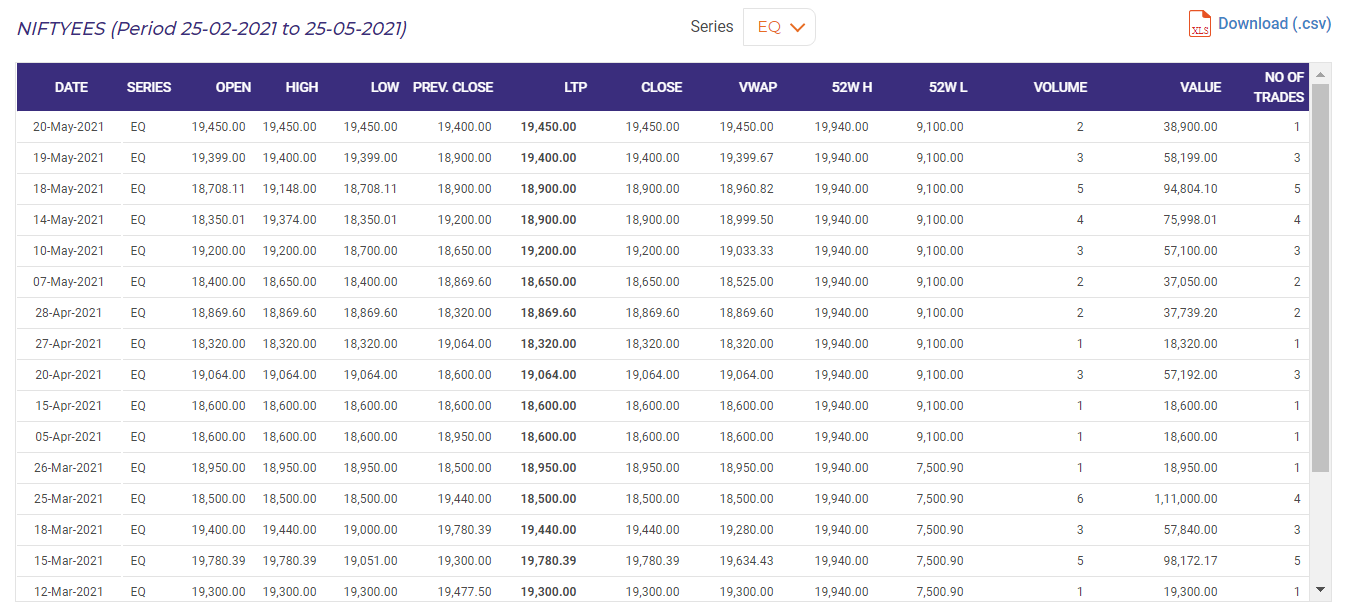

I understand that illiquidity might be responsible for this situation but given that it has been happening for an extended period of time, why are there no Authorized participants (AP) or the AMC maintaining this ETF stepping-in to resolve this disconnect between the actual NAV and the trading price of the ETF?

If a Large Investor approaches the AMC and directly purchases this ETF from them in Creation Unit size (which according to the latest Scheme Information Document is 400 units) and then goes ahead & exploits this arbitrage opportunity in the open market by selling those units slowly over the course of time, would this even be legal? Also, if a Large Investor approaches the AMC and tries to purchase 400 units of the ETF at NAV, wouldn’t the AMC be able to guess their motive behind doing so and appoint an AP beforehand to fix the liquidity problem making the arbitrage opportunity vanish altogether?

You need demand for the AP to step in and moreover, for most AMCs, ETFs are just shelf-filler products.

This is how ETF arbitrage wors Several people used to do this when N100 was trading at abnormal premiums. It was quite a profitable trade. Off-late, people do this in G-Sec ETFs.