Given that demat for MFs is of little value to investors vis-a-vis loss of control (please see this, this & this), could you please explain why Coin chose to go the demat route when even a regular online distributor like FundsIndia does not do demat?

- If you are investing in multiple asset classes like stocks, bonds, ETFs then it provides a single portfolio. This is a big draw for me.

- The most underlooked reason in my view is that in case of death, it easy for your nominee to claim. In case of a folio, he will have to individually run around to the AMCs and then complete the formalities.

- They are broker and they are a DP becomes way easier to do this with Star MF.

Honestly, I don’t see any big disadvantage of holding MFs in demat. I’ve converted my folios to demat. The guy who wrote the Business Today article seems like an ass. To throw shade on holding MF in demat mode he has explained the settlement process and given a lot of useless info. The reality is redeeming an MF is just a couple of clicks no matter the mode. The freefincal makes a lot of assumptions which aren’t true for all investors.

4 Likes

The big folly of this oft repeated reasoning ( repeated even by Nitin) is that this assumes that the nominee will also have a demat account. Which wont be the case in 90% of the cases as nominee is mostly wife or parents.

Also the heirs of the dead person will also need to claims all the portfolio if they have the demat account or not.

And believe it or not MFUIndia has made all these things wayyy easier to handle.

FREE OF COST.

1 Like

Getting a demat account isn’ that big of a deal in this day and age thanks to Aadhaar. Not a deal breaker at all.

That’s good to hear. Never used them though.

1 Like

MFU India is way advanced than Coin.

Free of Cost.

SoA mode.

Has mobile app too

Will check it out.

What is SoA mode please?

Hello @Sanket, @nithin, @Bhuvan,

All fine. Hance proved holding MF units are advantages compared to non-demat form.

Though it’s upto once choice whether he wants to hold it in demat or not. I am quite sure that I’m not going to die in next couple of years.

Now, I don’t want to hold all the MF units bought in Zerodha coin in my Demat account. And also I don’t want to redeem(as ELSS funds can’t be redeemed) them. Folio switching is a options which is possible and should be available for customers. Can you put some light, how one can achieve this?

This just a simple query. Please consider it in same way.

this assumes that the nominee will also have a demat account.

Even if the nominee has a demat account, things aren’t straightforward. My father had demat MFs and stocks with Geojit which got transmitted to my ICICIDirect acc after he passed away. However ICICIDirect-the-great does not support demat MFs. My options are:

- Visit branch to Remat each folio (Rs.25 per folio) and transfer-in

- Visit branch to redeem the units (which may run into the fractional units problem)

1 Like

Statement of Account.

It is almost same as demat mode.

You don’t need to keep physical shares.

They are also held in electronic format just like demat.

Demat is a type of electronic format used by Depositories.

There can be multiple ways to maintain your books.

So MF industry uses this SoA format.

1 Like

Yup…

Thats y I prefer MFU.

Anyways its always better to separate your Investements, Trading, MFs & FDs.

Like a portfolio diversification.

Service Provider diversification.

1 Like

I am not an expert in MF investing, so I don’t have an opinion on demat vs. SoA etc. However, I found the below comment interesting:

Correct me if I am wrong, but aren’t demat accounts registered with CDSL, which is controlled by BSE along with several banks? Doesn’t this mean that there is no risk with investments held in one’s demat account from any possible illegal/unethical actions by the intermediary (like Zerodha), since CDSL’s systems are presumably well designed to protect investors from such possibilities?

Is there any risk with high service provider concentration - having only one service provider? If I rely on Zerodha’s services (demat, Kite, Coin, etc.) for 100% of my investments, is there any risk in case of extreme unlikely events like Zerodha going bankrupt, or the promoters (I am sure they are wonderful people in reality!) suddenly going bonkers and committing fraud, etc.?

I know such cases are very very unlikely, but I am interested in having an idea of what are the possible, theoretical risks, however unlikely they may be.

Thanks in advance!

I am also not 100% sure here.

But let me take an educated guess.

-

Yes Demat with CDSL/NSDL are extremely safe. There are indeed minuscule chances of any fraud on account of Zerodha or other brokers. But I assume that you have given PoA to Broker and hence he have all powers to remove your MFs etc from your demat - ethical, unethical, illegal - that will be matter of investigation.

Why I said diversification. -

Just to make use of various facilities by various services.

-

To save bucks on services

-

Easy visualizing the investments.

The MFU have more advanced and more efficient platform, services, facilities than Coin.

You need not pay 50 per month.

Also with zerodha there is always chances of some mishap or the other. consider a situation in which you are not able to exit a position, sell MF because N is busy accepting some award? ![]()

![]()

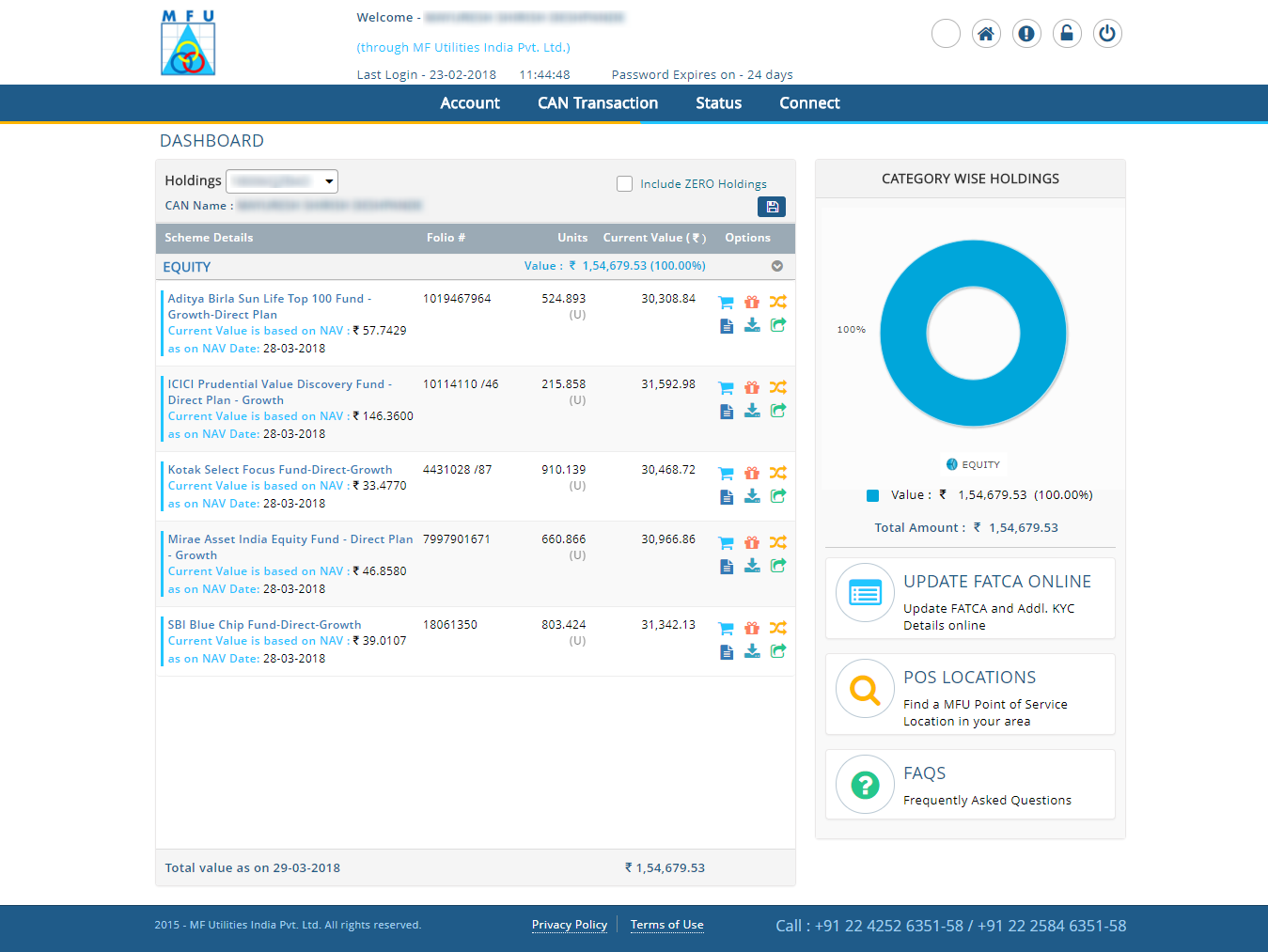

I have Direct MFs with MFU. Let me tell you the Apps from which I can access all those MFs

- goMF -by MFU

- myCAMS - by CAMS

- KTrack - by Karvy

- Individual Apps of various AMC

- Website of MFU, CAMS, Karvy & individual AMCs

Now i can access, transact in any MF from any of these platforms.

For eg SBI MF can be accessed from goMF, myCAMS, SBIMF Invest APP.

But this is possible only if you have SoA MF. If your MF is in Demat format, you can see your folio from the app but cant transact. So in case you have coin based MF only gateway to your folio is Coin - which may crash any time just like kite.

So yes its way safer to have SoA MF.

PS - once N himself put forward this line of argument while defending coin vs MFU

And guess what, same things happening with zerodha. Can’t keep pace.

2 Likes

@maddy_Des Thank you. I had a quick look at MFU website. First impression is that the website needs improvement  , doesn’t look as polished as Zerodha.

, doesn’t look as polished as Zerodha.

But will check it out in detail later when I have the time.

Cheers!

1 Like

More the facilities, more the complex GUI will be!

Coin has no STP/SWP, SIP from Bank, mobile app, CAGR or XIRR

It can’t get clean & simpler than this.

Also if you have some problem in understanding you can ask.

Also read this

2 Likes

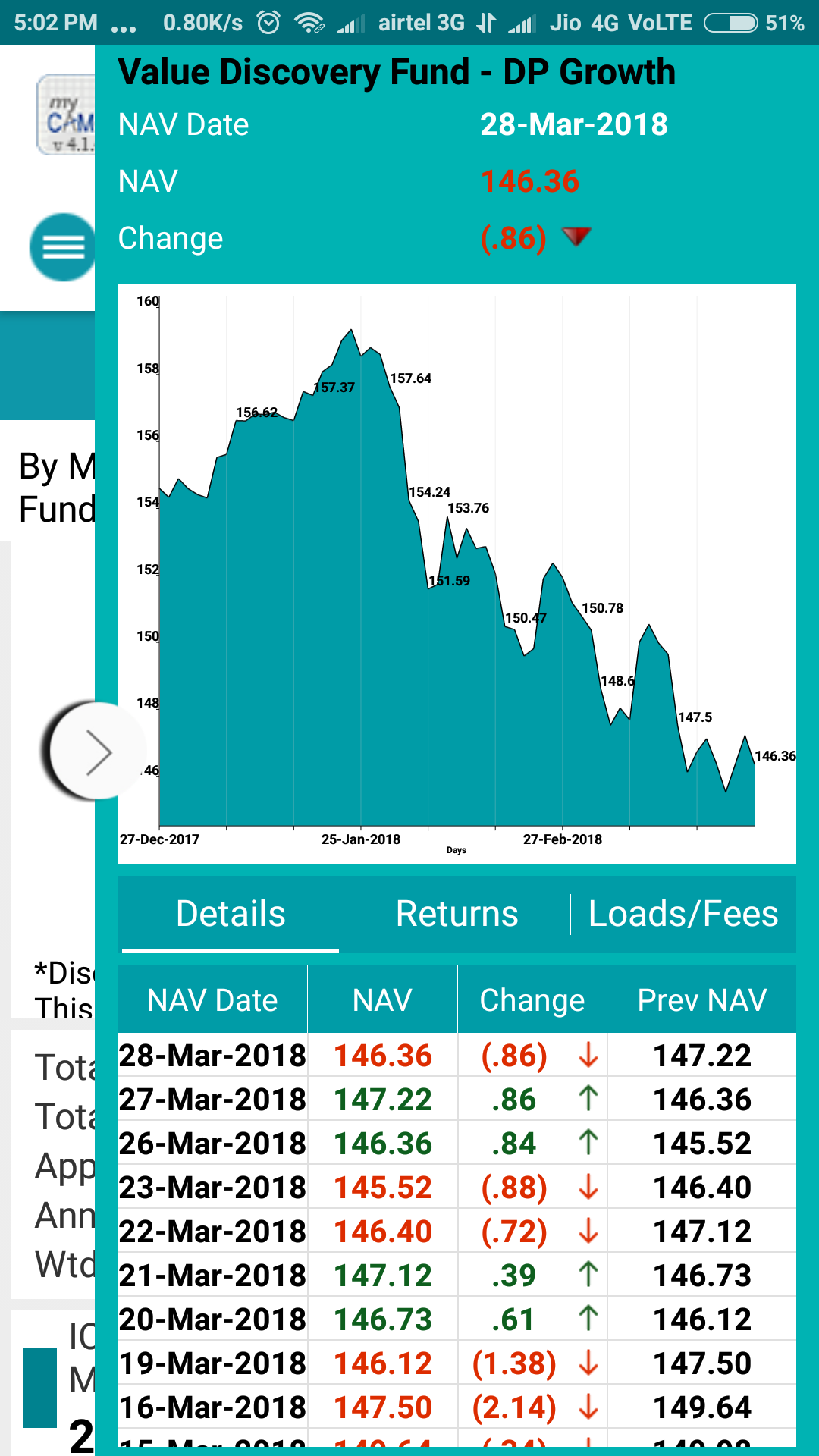

And this is how myCAMS app looks like.

If you have non demat MFs of CAMS catered AMCs.

Can you expect this from Zerodha even in 2020?

You can click on this link to understand the remat process. If its still not clear then kindly raise a ticket on our support portal.

Cool

Hi Mady, where can I find CAGR or XIRR etc in the MFU app? I have never seen anything like that. It does not show the price you bought or the returns. All I have seen is the current value.

Not sure if I am not looking at the right places. Thanks slight_smile:

1 Like