The idea was to offer simple and cost-efficient index funds and ETFs and stay direct only. Despite not being loud about the AMC, 7 lakh investors have saved ₹6,400 crores in our funds.

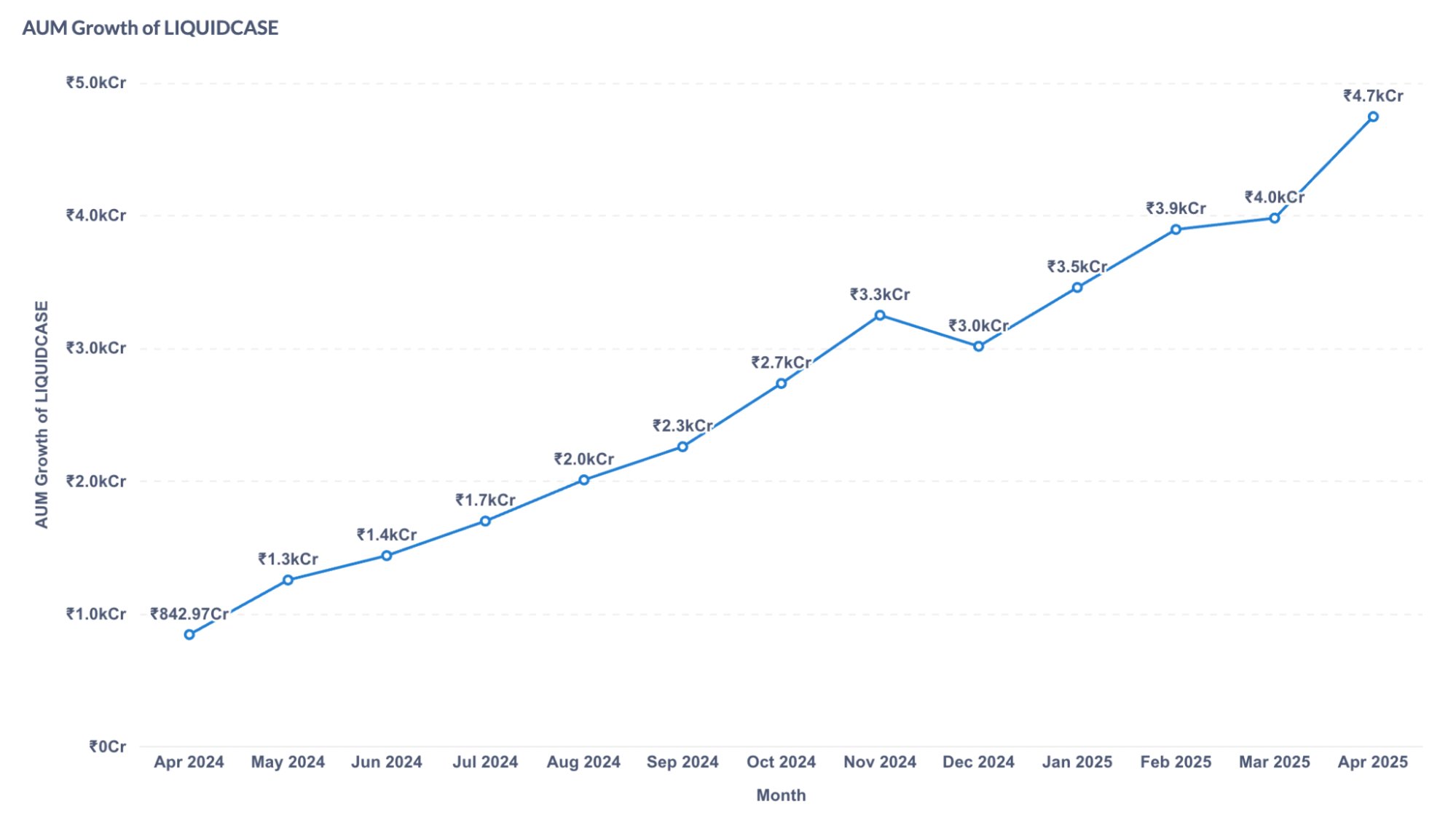

The hero fund is LIQUIDCASE ETF at ₹4,700 crores, and this is all in 15 months. LIQUIDCASE has to be one of the most successful Indian retail ETF launches ever.

When clicking on the link for Liquidcase, I find under Benchmark, SB rate as 2.85%. It says rates sourced from RBI and when I click on that link, it just shows RBI website. Can you please let me know in which section under RBI website, do we get this data.

I thought Banks were allowed to fix the interest rate and RBI do not control the same. It is for this reason, you will find IDFC giving 7% whilst SBI as of today is giving 2.70% and tiered.

The Benchmark rate remain fixed for 1yr, 2yr and 3yr.

I am sure there must be some changes in rates over a period of three years, find it difficult to assume that the rate remained same for each of the three buckets.

Also how is the benchmark arrived, is it the lowest rate offered by banking sector in India or an average taken or is it from RBi website. I want to see this section in RBI, tried searching but could not find the same.

Would like to know how this benchmark is arrived. it is important that this rate should be correct as this is the rate based on which the liquid case is compared.

Axix, icici and Kotak is on tiered basis from 2.75% to 3.25%

IDFC - 3 to 7%

Yes 3 to 5%

DCB - 1.5 to 7%

Canara - 2.70 to 4%

Is the benchmark computed based on PSU bank, then it has some resemblence of average of 2.85. If so this should be mentioned as a note so that investors are aware of the data being presented.

Same thing with inflation data, under sources, it opens up IMF website and I could not find the rate.

Related query - The return from this liquid case over the last one year was 6.52%. This is after the expense ratio of 0.27%. The purpose is to park free float funds into this fund instead of Bank SB account. So this also means that when I sell I will be subject to STCG of 20%. So is my real return approx 5.12%. Is this a correct assumption.

IIUC, the benchmark for a fund is whatever the fund wants to benchmark itself against. (subject to any restrictions specified in the securities regulations.)

The choice of the RBI “Savings Deposit Rate” as the benchmark appears to be a reasonable one, as this fund aims to be extremely liquid (almost like an SB account).

From what i gather, the Savings Deposit Rate was deregulated in India with effect from October 25, 2011, despite strong push-back from the retail banks. Retail banks are no longer restricted/guaranteed the RBI published Savings Deposit Rate in the savings accounts that the retail banks offer. As such, the RBI published rate is just a reference rate that can be used as a benchmark - which this fund appears to be doing.

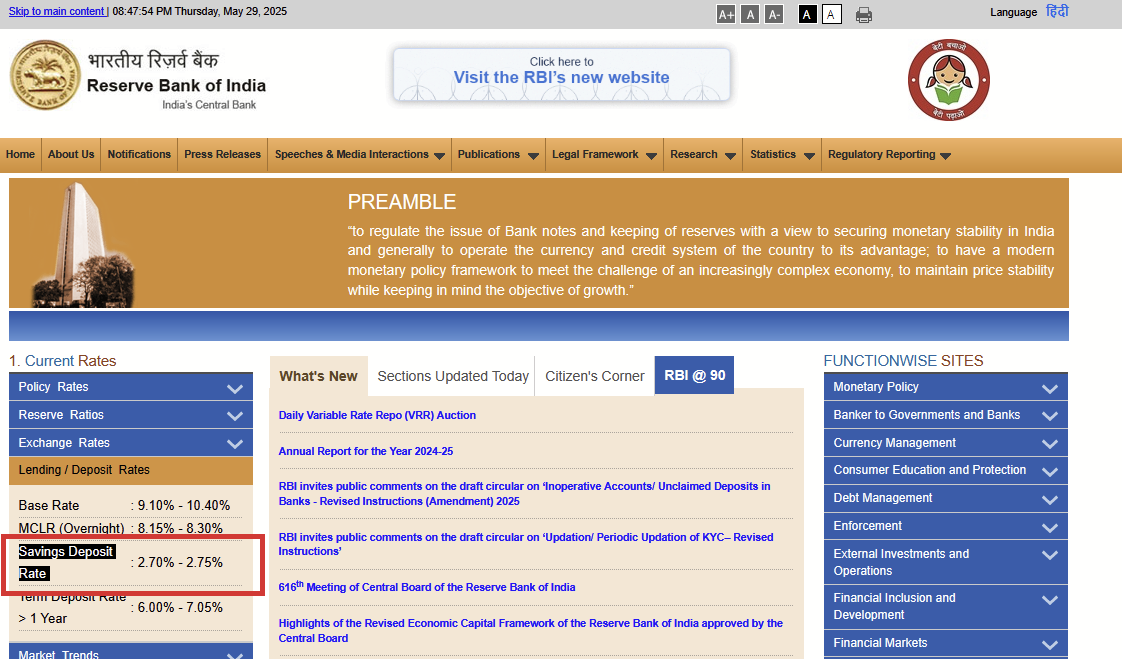

The current/latest Savings Deposit Rate on the RBI website

appears to be listed under Lending / Deposit Rates section.

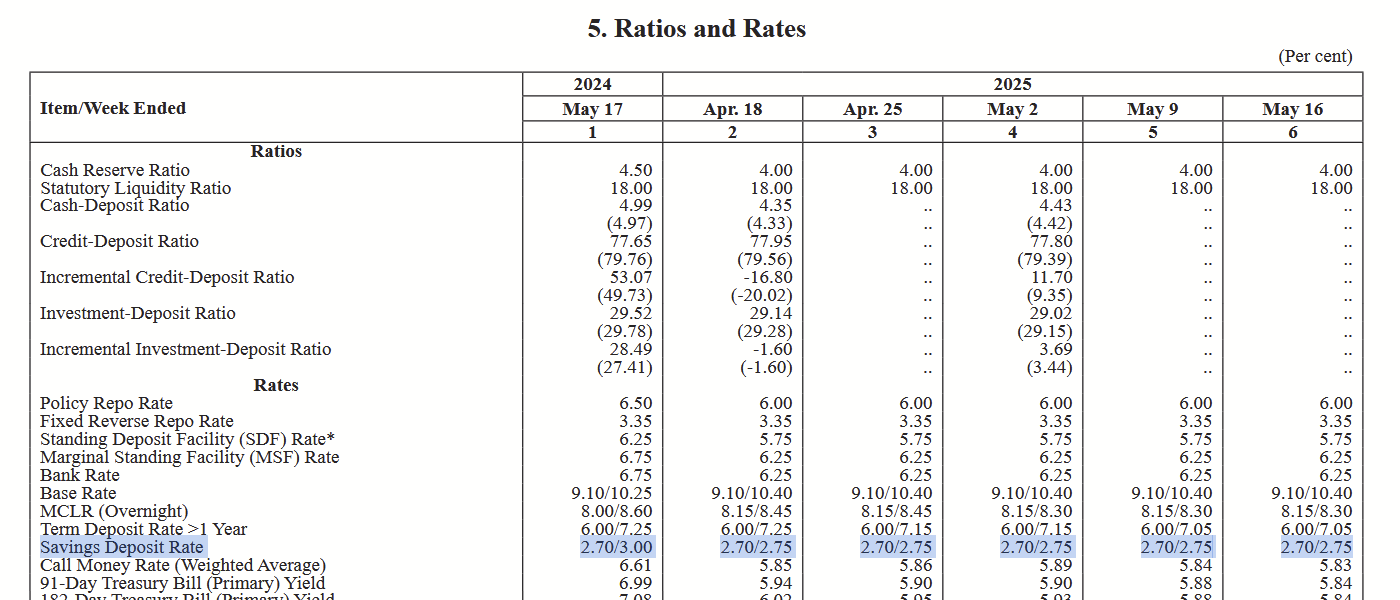

Also, searching on the RBI site for the specific phrase Ratios and Rates

lists a bunch of results that include weekly published “Ratios and Rates” circulars.

PDFs of the same appear to be currently available at the link https://website.rbi.org.in/documents/87730/39710791/T5_DDMMMYYYY.pdf

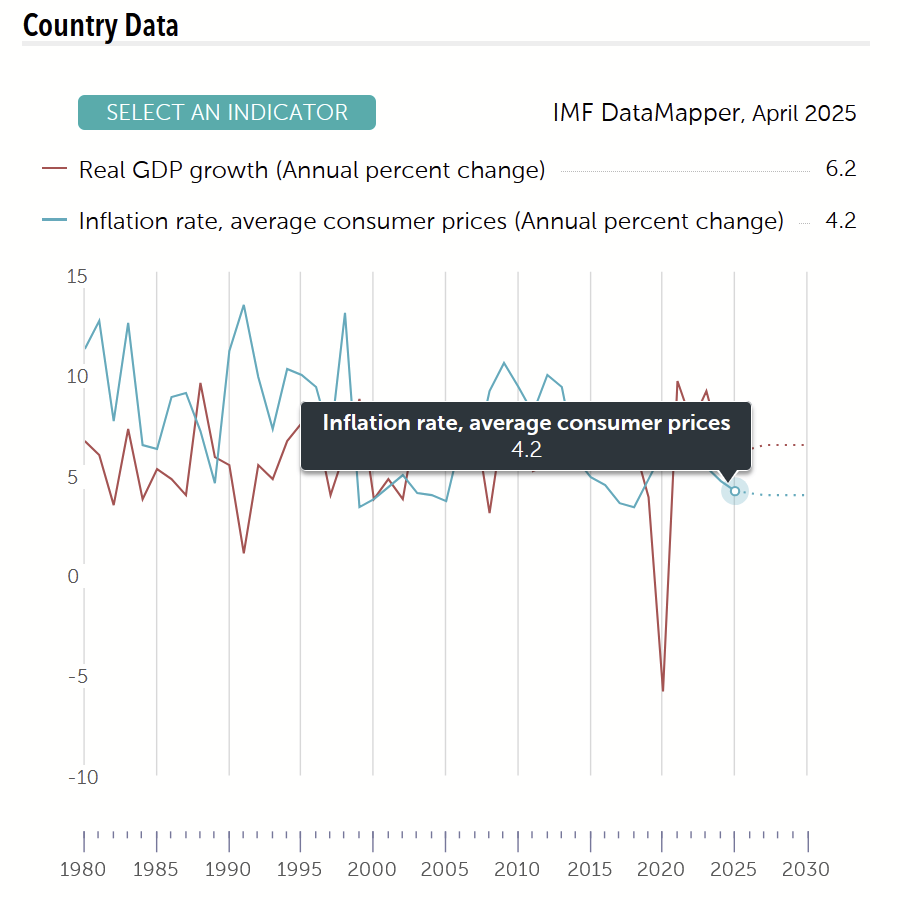

A chart with annual GDP and Inflation (CPI?) is available for India at this page on the IMF website

(and further details in various reports available on the page).

Bank FD gave more returns than LIQUIDCASE. Only advantage is that you can pledge it and use as a “Cash component” with 6.00% haircut. IMO this fund is good only if you pledge it and use it for trading.

I think LIQUIDCASE gave best returns as compared to the other cash component options. Next best in terms of return is LIQUIDADD.

Tax Implication

All gains/profits from the units of the Liquid ETFs, irrespective of the holding period, will be considered as Short Term Capital Gains (STCG) and will be taxed as per the tax slab of the investor (plus 4% cess and surcharge, if any).

Bank SB ac interest is also on slab rate, Liquidcase is also on slab rate - net effect same.

Few private banks apart from SFB, offer higher rates than Liquidcase and no need to pay Expense ratio of 0.27% and non zerodha customers have to pay brokerage as well like icici direct.

I think the advantage is for traders like @Jack_R pointed out, who can pledge this for their trades as against funds in SB account.

From return perspective for a retail investor, sb interest gives a better return dropping the idea of parking funds in this ETF.

If your income is taxable, growth MF only gets taxed when we sell. That can make a big difference for static capital by compounding over the years.

Pledging on top of that makes it decent for trading. As all (tiny…) growth can be used as capital too.

But yeah, liquidcase is like overnight fund ( so low rates) and with higher expenses. Best use case is pledged capital that you may need to withdraw to fix negative balance. Otherwise go for lower expense funds or alternative ones with higher rates ( and risk )

Small difference. Since liquidcase is a growth fund, tax implications are only at the time of sale. That’s not the case for FD. There is time value of money even for the tax portion.

Did not understand. The money that i keep in my SB account (Not FD) which everyone keeps for their regular expenses, I thought of moving it to this ETF as I thought this will give better returns than SB rate. Money will eventually be used up and hence I have to sell these units and incurr capital gain. I thought this ETF was an alternate to SB account and I get higher return than SB interest rate i.e on my float balance.

But when compared, it does not appeal as I get higher return on SB account - The choice of liquid case was not for long term investment.

I repeat is this ETF an alternate to maintaining funds in SB account which gives return on float balance and return is higher than SB interest rate…

Savings bank typically give around 3% ? Overnight finds such as liquid case can give more.

liquidcase current yield after expense will probably be around 5.5-6%. Both on slab.

If your bank pays more than 6%, then yes no point in using liquidcase/overnight funds for your usage.

Anyway the diff wont be much and may not be worth the hassle for everyday expenses. I don’t use it for that.

As soon as possible - Please launch a passively managed aggressive hybrid index fund with a 75:25 equity:debt asset allocation ASAP [ must be re-balanced monthly to maintain the asset allocation]

Okay. I think I wrongly interpreted your post. I thought you were considering it instead of FD.

For SB balance I do not think any bank gives more than 6 percent interest right away irrespective of balance. I know IDFC gives but I think that is only if avg balance is more than 5L. (I am not sure).

But if you are considering frequent buying and selling small amount from this etf, I do not think it will even beat sb rate. There are trade charges to be incured with the etf.

To make meaningful difference you might have to have at least 10L in this etf with not so frequent trades.

I go with a silly approach for my investments, but it has worked for me so far. Like I park my funds in Bajaj Finance and Federal Bank etc., mostly NBFC FDs etc. which offer 8%+ returns (including extra 0.5% for senior citizens and 0.5% for women/senior accounts - someone in family). Without those benefits they offer 7%+.

My silly analysis is I calculate some probability of collapse. I look at the market cap and brand name. For example Bajaj Finserv has a market cap of ₹3.22 lakh crore, and it’s the 7th largest in the financial space in India and part of a large group. So, I get in theory the chances of it collapsing are very low - close to none.

I don’t analyze yield or benchmark rates. I just look for a strong company, decent interest and easy to understand structure maybe becuase i dont understand financial fundamentals like many of you guys tbh… i am very poor at it.

Maybe not the smartest analysis but it has worked for me so far. Just sharing!