Thank you @livepositionaltrader for sharing the detailed thought-process behind the NBFC-FD approach.

The previous post was underselling the amount of careful thought

that has gone into the investment approach into NBFC-FDs. ![]()

Subsequently with all the details involved, being discussed in this topic-thread,

hopefully now anyone else reading this topic-thread in future,

will not go for any abstract approach to calculating risk based on their “gut-feel” of a brand. ![]()

Also, here are a couple of potentially overlooked aspects in the “NBFC-FD” approach described so far.

( Sharing just in case these were not considered yet.

In case these aspects were already considered,

please do elaborate if you arrived at a different conclusion than the following. )

1. Comparing returns from NBFC FDs to LIQUIDCASE ignores their differences in liquidity.

What was the lock-in period of the NBFC-FDs offering the 7-8% annual rate of return?

For example, if we are considering NBFC-FDs that mature over 18-60months,

then the appropriate benchmarks to compare them against would be

T-BILLs, GSECs, SDLs, maturing over a similar time-horizon.

These assets offer higher returns than LIQUIDCASE,

- due to the lower liquidity

and higher expected value than NBFC FDs

- due to the further drop in probability of default (Sovereign vs. CRISIL-AAA).

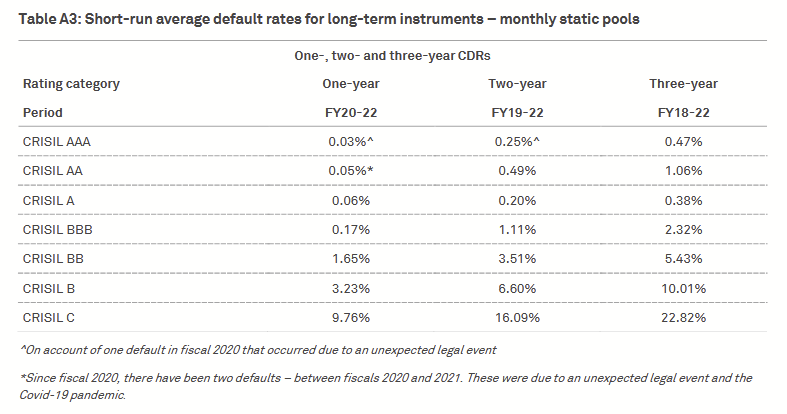

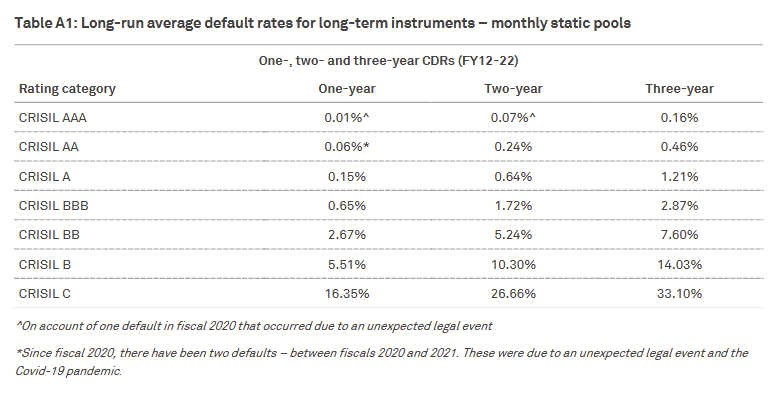

2. The methodology behind the default-rate implied by a CRISIL-AAA rating is unclear.

Could you please share any references that led to the following assertions?

i would like to understand the methodology behind the same.

As an additional data-point, looking at CRISIL’s own report from 2022-23

(that popped-up in an online-search for CRISIL ratings and their associated default-rates)

which mentions that over a 10-year analysis period,

the cumulative default rates are significantly higher than 0.1% over a 2-3 year horizon

(the periods over which NBFC-FDs are offering the high 7-8% returns being discussed)

[ Source ]

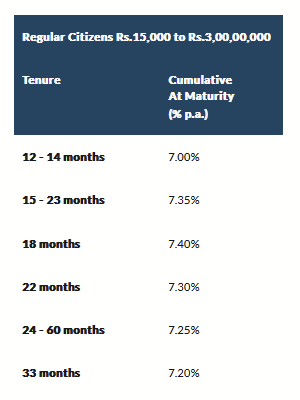

Rate of returns of an NBFC-FD over various tenures

[ Source ]

If we consider the range of default-rates from the above CRISIL report,

i.e. 0.07%, 0.16%, …, as high as 0.47% in recent times,

EVFD = (1 - 0.0007) × (1 + 0.0595) = 1.05876 (~5.88% risk-adjusted return)

...

...

EVFD = (1 - 0.0047) × (1 + 0.0595) = 1.05452 (~5.45% risk-adjusted return)

Note: The above math is overt nitpicking. The margin-of-error around these numbers is higher than what the above precision implies. The point being that, at extremes, even tiny numbers make a outsized difference.

PS: A previous draft of this post contained an error in calculations, despite my best efforts to triple-check it before posting. This has only further solidified my belief that the human brain cannot intuit accurately at extremes. ![]() Please do highlight if any other errors, either logical or mathematical, have still slipped through.

Please do highlight if any other errors, either logical or mathematical, have still slipped through.

A 3rd overlooked aspect. (potentially off-topic if each investment is evaluated in isolation)

3. The entire capital invested in an NBFC-FD is at the designated risk

(…however minuscule the risk may be.)

If investing in such instruments to maximize returns, while…

- …lowering overall risk

- …ensuring predictable-income / future-assets

…then the barbell approach can be of relevance in this context/scenario.

Attempting to extract a few additional points of return

by investing in a “middle-of-the-road” somewhat riskier proposition

is usually worse than explicitly splitting one’s investments into 2, and,

- ,continue investing the fraction that one cannot afford to lose.

- at zero risk (as near zero in reality as possible).

- ,investing the fraction that one can afford to lose.

- at a significantly higher-risk (as high as one wishes/expects overall returns to be)

PPS: This barbell approach is also applicable outside of purely financial scenarios.