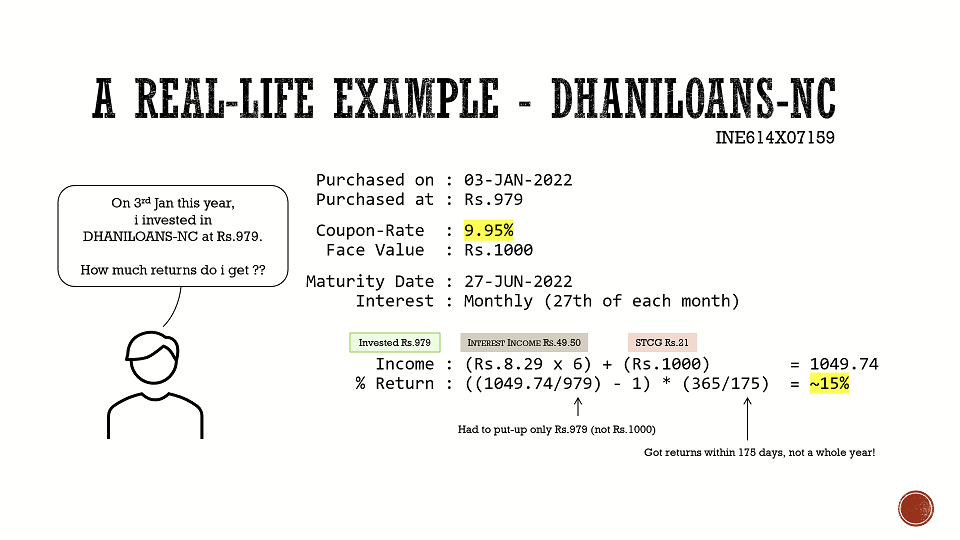

Recently, i purchased DHANILOANS (series NC) bond at a discount.

According to my calculations i am getting 15% p.a. returns over the next 6 months.

Is this correct?

Recently, i purchased DHANILOANS (series NC) bond at a discount.

According to my calculations i am getting 15% p.a. returns over the next 6 months.

Is this correct?

Your calculation is correct on a annualised basis. Your actual return will be 7.22% for a period of six months.

The bigger question being who is Dhaniloans NC. I am sure you know who this group is. The very reason you got the NCD at a discount is someone wanted the money back and hence offered the discount. The secondary market for bonds are very illiquid hence, anyone who wish to redeem need to offer a discount.

Agreed.

Another reason for bonds being available at a discount could be as follows…

I believe many folks have been selling a significant chunk of their bonds at a 2%-10% discount during the recent slump in DEC-2020, to invest their returns in stocks which they expect to bounce back more than 10% in the next few months.

The bigger question being who is Dhaniloans NC.

I did some online searches and looks like a NBFC that is doing somewhat OK.

They even have a newer IPO that folks are subscribing to.

As the bond i invested into, matures in 6 months, i think it is a smaller/short-term risk for me.

Assuming the math is fine, i will try to repeat this on AAA bonds during the next market slump. ![]()

I don’t think this is the case. They can raise funds by the help of bonds they own so no point in selling the bonds in discount. Anyway the folks who own bonds generally don’t speculate in markets this way and also to this magnitude that they would liquidate ther debt to this significate discount.

Though there might be various reason for this which we might not be able to know.

Let me at the outset put in a disclaimer that I am nobody to advise anyone. With this disclaimer in mind, do take into account credit risk of these companies.

Most of these companies, need to get fresh issue out to redeem the earlier ones. The problem will occur when the fresh issue is not subscribed. I am sure closure to maturity, you will be getting calls to put in the money into new NCDS.

This is the main problem with NBFC, their lending will be for longer tenor, however NCDs or bonds will be shorter tenor and this mismatch will remain.

Take a very calculative call.

That’s a good point.

My assumption that “During a market slump, folks are selling off their bonds to invest in Stocks” is based on the fact that the LTP of many of the liquid AAA Bonds (with significant daily traded volume) have fallen whenever NIFTY fell in the past several years.

But, maybe i’m seeing patterns where there are none.

Maybe, there are other factors at play that can explain this correlation… ![]()

Thank you for this insight. ![]()

By calls, if you mean this is a callable bond, this bond is not.

So as long as the issuer doesn’t go bankrupt, i believe the original principal will be refunded upon maturity - netting me a tiny profit capital-gain. ![]()

By the end of this month (when the current IPO completes),

if i start getting contacted by the issuer to invest in the current IPO,

then i better sell-off the bonds from the older series that i am holding soon,

as the issuer will be unlikely to pay back the principal of these bonds maturing 6-months down the line.

BTW, given an ongoing (or recently concluded) bond IPO (eg. DHANILOANS 2022),

anyone here knows how to find out how well it is subscribed ?

I meant telephone contact from rep of Dhani. Since you have already bought the bonds, hold still until maturity and I am sure you will get back your money with interest. It will be upto you then to look at other options.

Dont worry too much on this.

The proceeds of this bond will be used to repay your tranche. This is the normal cycle these NBFC follow.

Found it! ![]()

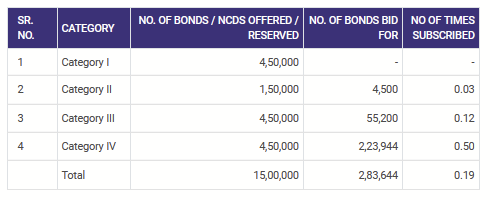

As of today,

1 week into the ongoing DHANILOANS IPO (and 3 weeks left till the deadline),

the IPO appears to be only 19% subscribed so far.

[ Source: NSE ]

Hopefully, the above ongoing IPO gets better subscribed over the next few weeks,

so that they will have enough funds to pay back the principal

on the previous series of their bonds maturing later this year.

I wonder why investors run behind such bonds or NBFCs/banks…i don’t know anything about this group but our hard-earned money should be dealt with deep study/caution.

@CoolBird i completely agree with the above sentiment.

In my case, i recently started learning about bonds.

I have invested a small amount in this bond as a learning exercise.

Even if i lose this due to my miscalculations, spending a thousand bucks to learn seemed a reasonable “fee”. ![]()

At the time i was exploring the NSE bond market, this was the only bond that fulfilled a bunch of criteria.

Hence i chose this bond series for my learning experiment.

(Not a recommendation/endorsement. Sorry, if my initial post came across as such.)

Following-up on @neha1101’s insight earlier in this topic-thread, about how NBFCs repeatedly raise money from the market to pay-off previous debts, i also came across this article on how NBFCs are currently bearing the majority of the risk of long-term loans to the real-estate development bubble.

Time will only tell if/when exactly this real-estate bubble will burst and NBFCs backing them will default.

Based on my layman/armchair analysis, DHANILOANS appears to be relatively less exposed to real-estate risks. If i understood their latest prospectus right, it appears to have < 10% of its loans backed by residential/commercial real-estate (specifically pages 50, 122, 323, and 398 of the PDF).

Indeed! ![]()

Any comments on potential risks in this scenario (or with NBFCs, or even on Bonds in general) are welcome…

Well your math is correct but unfortunately it works well only at very small quantity. In fact it is monthly interest paying bond, so if you do XIRR calculation, your return would be higher than 15%

Only problem, this bonds are illiquid with very thin traded quantity.

For bond under question max traded quantity in recent past looks like 1.3K (that’s just 13 lakh rupees) on most day traded qty is just 100.

So if you are just buying for few thousand, everything works. If you want to buy for 1 lakh, your order itself will distort the price and the yield.

Coming to the risks, while most of your point are valid, just wanted to point one

As I said, this is not really a liquid bond. Since probably you just bought single bond, it looks liquid. But it is not.

Well everything looks rosy till it isn’t. issues surface only when somebody starts digging.

From recent past, both DHFL and Srei met this criteria. There were no issues and suddenly scams started coming up.

Also, when issues comp up, price won’t reduce linearly, it wall be a vertical fall. So constant monitoring of quality and cutting your losses at right time if something pops up is required.

Yes because this NBFC is not in real estate sector. This was originally Indiabulls consumer loans, which got renamed as Dhani. Indiabulls had separate NBFC for housing and real estate loans. This NBFC predominantly lends unsecure loans to retail investor.

With repeated lockdowns this sector is also coming under stress.

But yeah just for learning perspective, seems like a good trade.

Update : Received the first of the 6 monthly dividend payments left on the bond.

It was credited directly to the bank account associated with the Trading account used to purchase the bond.

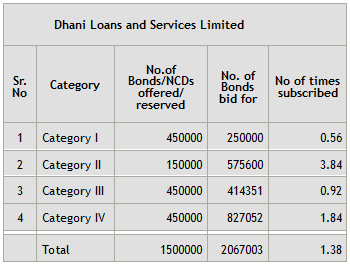

Also, i see that the recently concluded bond IPO of DHANILOANS has been over-subscribed.

[Source]

The inherent maturity-mismatch (a common type of asset-liability mismatch NBFCs usually face),

doesn’t appear to be an issue for DHANILOANS over the next few months.

That’s one less reason for them to face any liquidity issues in the short-term,

i.e. one less reason for me to worry about! ![]()

Now to sit-tight for the next 5 months, receiving my remaining 5 monthly dividends,

and then i can count my minor capital-gains… ![]()

![]()

![]()

This is no longer true.

Based on the recent developments related to Dhani Loans…

…i felt unethical and unsafe,

investing in their bonds (even for a few months).

Hence, i sold off my handful of bonds i had purchased as an experiment.

Thankfully, i had NOT invested in the stocks of the same company.

Folks holding the same company’s stock,

have seen the value of their investment halved in a month! ![]()

Note that even when the stocks of the company dived, hitting the exchange’s lower-circuit-breaker on 3 consecutive days, the company’s bonds stood strong. However, i lost my nerve that even the bonds would fall and that was a major reason that triggered me to sell them off sooner rather than later.

The fundamental issues do not appear to be specific to Dhani Loans alone. It appears to be the “Standard Operating Procedure” of NBFCs operating in India right now. Thus, this concludes my foray into the NBFC “cesspool”. Learnt few lessons. No obvious losses. ![]()