Since both the Equity Linked Savings Scheme (ELSS) and Public Provident Fund (PPF) are saving schemes eligible for tax benefits investors may be confused in picking out one of the schemes.

While PPF has been a traditionally popular investment option, ELSS is steadily gaining traction due to better risk adjusted returns and lowest lock-in period.

What is ELSS?

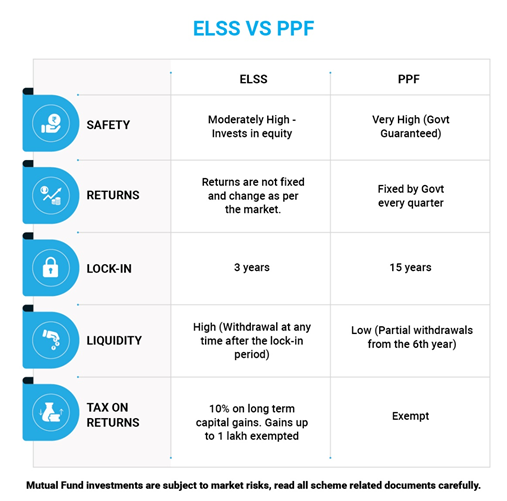

Equity Linked Saving Scheme (ELSS) is a type of mutual fund that is eligible for tax deduction benefits under the section of 80C of the Income Tax Act, 1961. Due to market linked returns and lowest lock-in period in the tax-saving category, ELSS has become more popular in recent times. You can invest in ELSS either in lump sum or through Systematic Investment Plans (SIP). Though ELSS funds are subject to market risks, historical data shows that equity has been best performing asset class over long investment horizon

What is PPF?

Public Provident Fund (PPF) is a government-backed saving scheme which provides guaranteed returns and added tax benefits u/s 80C. PPF pays interest on accumulated deposits and accrued interest. PPF interest rates are linked to Government bond yields and may be revised on quarterly basis. If you want to invest in the PPF account, you can open a PPF account in a post office or any bank.

The article aims to present a comparative analysis of the two schemes to help investors in selecting the right one for them.

Tax Benefits u/s 80C:

Investments upto Rs.1.5 lakh a year in ELSS and PPF are eligible for tax deduction benefits under section 80C of the Income Tax Act, 1961.

PPF investments come under exempt-exempt-exempt (EEE) category.

ELSS returns are taxable at 10% if the gain exceeds Rs. 1 lakh in the year.

Earlier ELSS was also tax-exempt after 1 yr, but with budget 2017-2018, now any gains in equity mutual funds or stocks are taxable @10% when you sell them, but you get an exemption of Rs 1 lac per yr. This means that if your profit after selling ELSS is Rs. 4 lacs, then you have to pay a 10% tax on 3 lacs.

Lowest Lock-in:

ELSS investment comes with a lock-in of only 3 years in the tax-saving category, making ELSS investments a relatively more liquid option. You can actually redeem your ELSS fund investment in just 3 years.

PPF investments are locked in for 15 yrs, but some partial money can be withdrawn after 7 yrs.

Liquidity:

PPF has a minimum investment of Rs 500 and a maximum investment of Rs 1.5 lakh. You can make deposits in the PPF account up to 12 times in a year. Premature closure is only allowed on limited grounds such as serious ailments. You can take a loan on the PPF deposits from 3rd to 6th financial year from the year of account opening. Further, you can make a partial withdrawal from 6th year onwards but only on some pre-specified grounds. Withdrawals not exceeding 50% of 4th year balance are permitted after a lock-in period of 7 years.

ELSS mutual funds, on the other hand, are the most liquid investments u/s 80C. You can redeem your ELSS units partially or fully after the lock in period of three years is complete. However, it needs to be mentioned here that, you do not necessarily have to redeem your ELSS units after the expiry of the lock-in period. You should redeem according to your financial needs and invest in ELSS as per your financial goals.

While both the schemes are tax saving, it is important to pick a scheme based on return expectations, risk appetite and investment time horizon. PPF is suited for individuals who are absolutely risk-averse and can afford a 15-year lock-in period.

Whereas those investors who are willing to take a moderate risk to earn higher returns can opt for ELSS. The best way to reduce risk in ELSS to its minimum is by staying invested for the long term.

Disclaimer: The views expressed here in this Article / Video are for general information and reading purpose only and do not constitute any guidelines and recommendations on any course of action to be followed by the reader. Quantum AMC / Quantum Mutual Fund is not guaranteeing / offering / communicating any indicative yield on investments made in the scheme(s). The views are not meant to serve as a professional guide / investment advice / intended to be an offer or solicitation for the purchase or sale of any financial product or instrument or mutual fund units for the reader. The Article / Video has been prepared on the basis of publicly available information, internally developed data and other sources believed to be reliable. Whilst no action has been solicited based upon the information provided herein, due care has been taken to ensure that the facts are accurate and views given are fair and reasonable as on date. Readers of the Article / Video should rely on information/data arising out of their own investigations and advised to seek independent professional advice and arrive at an informed decision before making any investments. None of the Quantum Advisors, Quantum AMC, Quantum Trustee or Quantum Mutual Fund, their Affiliates or Representative shall be liable for any direct, indirect, special, incidental, consequential, punitive or exemplary losses or damages including lost profits arising in any way on account of any action taken basis the data / information / views provided in the Article / video.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.