I came across a an article in barrons.com. Its interesting because it says:

The U.S. Is Scaring Off Foreign Investors. Is It Becoming Un-investible?

That seems like a strange thing to say because of the fact that U.S. stocks have outperformed the rest of the world, by a huge margin, over the past decade

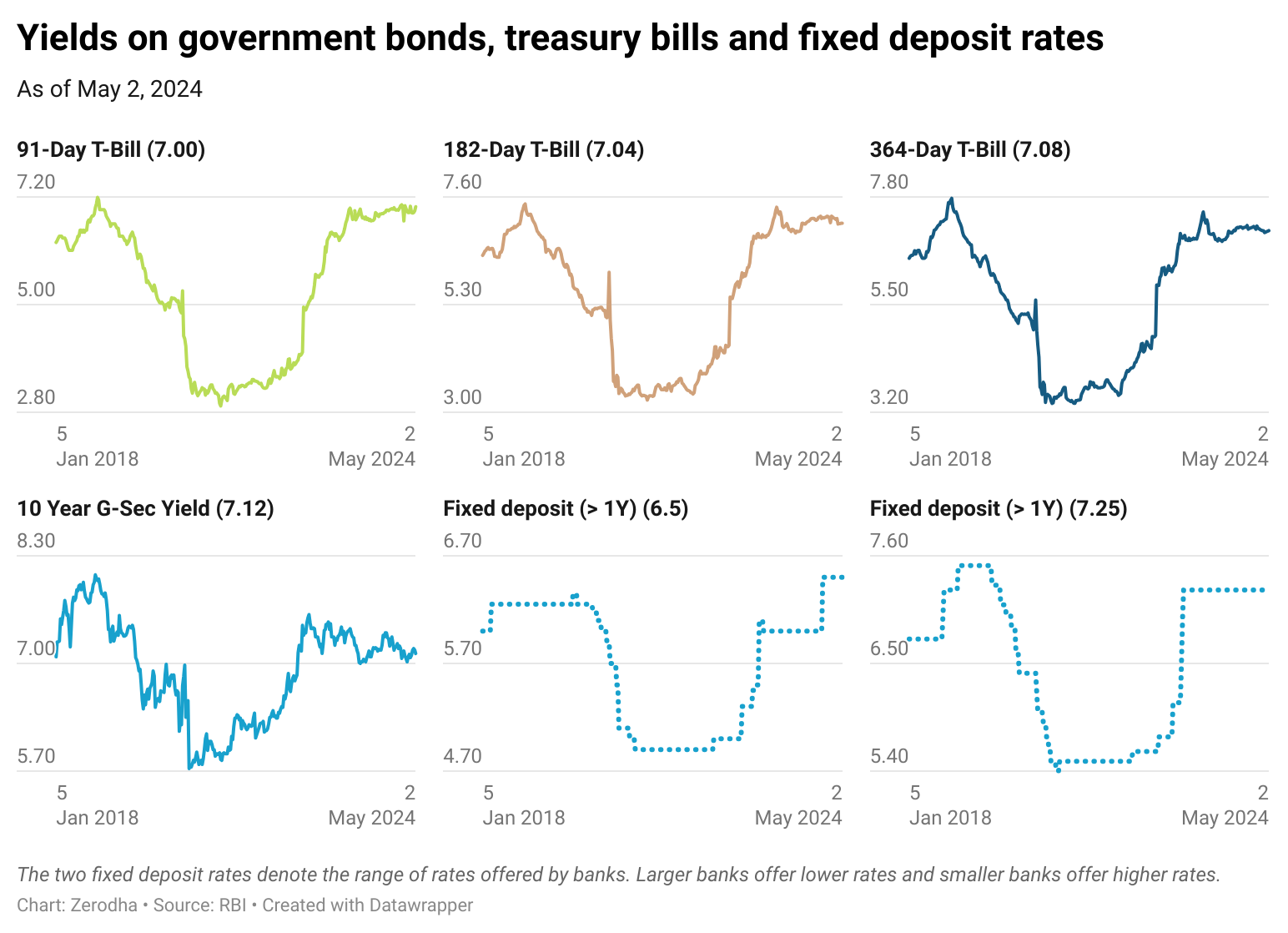

Risk of default is Zero as these bonds are issued by Government.

The above is the interest rate that is paid by the Bank. Example Ujjivan pays 7.75% for 990 days deposit. The 7.75% is the interest rate paid, the yield of the deposit on maturity will be a annualised yield of 8.54% as a sum of 1,000 for 990 days gives a total return of 1,235. The 235 is the interest and when you compute annualised yield it will effectively work out to 8.54%.

Bank deposits are not guaranteed if the bank goes bust or faces a liquidity crisis.

Some bank deposits are insured, but only to a limit.

IIRC, it is currenlty 5lac INR per bank account (for more details, read about DICGC insurance in india)

Bank FD interest rates vary based on the investment amount.

Banks often do not offer the highest rates for the largest amount of investment (lacs/crores). (this point might not be relevant when investing in thousands)

Also, the high interest rates are not guranteed for 10 years.

i.e. when if one books a 2yr FD at 8% today, one cann book 8% returns for the next 10 years.

There is no guarantee after 2 years the bank will offer to renew FD at the same rate for subsequent years.

Also, GSECs often provide higher returns than bank FDs (eg. currently some GSECs yield more than 8%).